Indian Government Savings Schemes Explained: PPF, EPF, NPS, SSY and the Full Small-Savings Map

By Tapabrata Biswas · Updated July 17, 2026 · 12 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is the pillar page for The Money Decoded's Indian Government Savings Schemes cluster — a research-led catalog of the small-savings, pension, insurance and gold schemes backed by the Government of India. Nothing here is investment advice. Scheme rates are reset every quarter, eligibility rules are specific, and the right scheme for any person depends on their goals, age, tax regime, and liquidity needs — which only a SEBI-registered investment adviser or a qualified Chartered Accountant who knows your situation can assess. For any decision that turns on your numbers, consult the appropriate professional.

Government savings schemes occupy a distinct place in Indian personal finance: they trade the higher potential returns of markets for sovereign backing and, in several cases, fully tax-free growth. A bank can fail; the Government of India standing behind a PPF or SGB does not in the same way. That guarantee, plus the Section 80C tax deduction that many of these schemes carry, is why they remain the backbone of conservative Indian portfolios even when equity returns look more exciting.

This page synthesizes the 10 cluster posts, lays out the current Q1 2026 rates side by side, surfaces the principles that tie the schemes together, and gives goal-based starting sequences for new readers. Each scheme has its own deep-dive post linked below.

The 10 schemes in this pillar

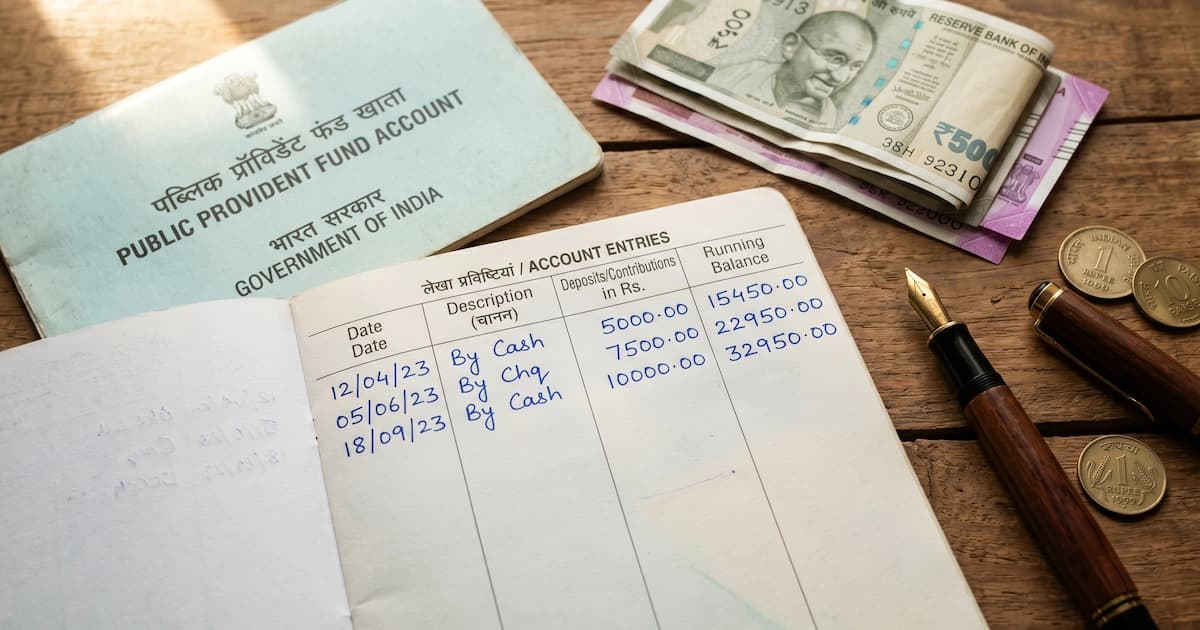

1. Public Provident Fund (PPF)

The default long-horizon government savings account, open to any resident individual. A 15-year lock-in, a government-fixed rate announced quarterly (7.1% for Q1 2026), and the cleanest possible tax treatment — fully exempt-exempt-exempt (EEE), with the contribution also eligible for Section 80C. The post covers the deposit limits (₹500 to ₹1.5 lakh a year), the interest-calculation quirk that rewards depositing before the 5th of the month, partial-withdrawal rules from year 7, and the 5-year extension blocks after maturity.

→ What Is Public Provident Fund (PPF)

2. Employees' Provident Fund (EPF)

The mandatory retirement scheme for salaried employees, established under the 1952 Act and administered by the EPFO. A 12% employee contribution is matched by the employer, earning the EPFO-declared rate (8.25% for FY 2023-24) — among the highest guaranteed returns in the system. The post covers the split of the employer's share into EPF and the Employees' Pension Scheme, the employee contribution's 80C eligibility, the EEE treatment on completion, and the withdrawal and transfer rules on changing jobs.

→ What Is Employee Provident Fund (EPF)

3. Sukanya Samriddhi Yojana (SSY)

The girl-child savings scheme, open only for a girl below 10 at account opening — one account per child. It carries the joint-highest small-savings rate (8.2% for Q1 2026), full EEE tax treatment, and 80C eligibility. The post covers the ₹250 to ₹1.5 lakh annual deposit band, the 15-year contribution window inside a 21-year maturity, the partial-withdrawal allowance for higher education at 18, and why it tends to out-yield a PPF opened for the same purpose.

→ What Is Sukanya Samriddhi Yojana (SSY)

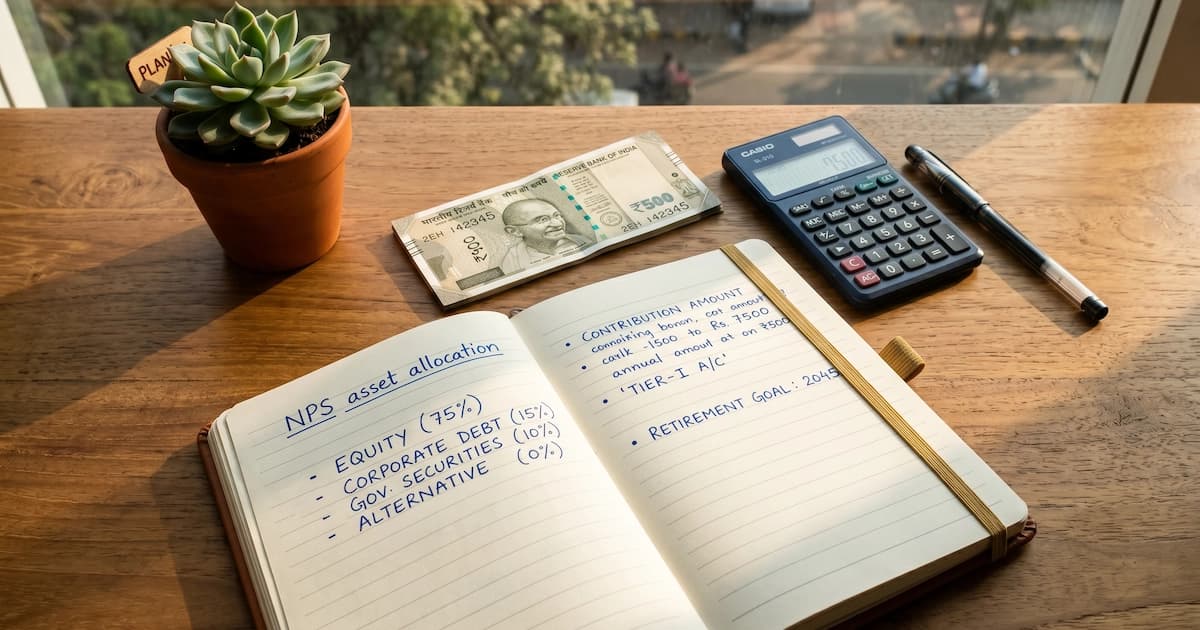

4. National Pension System (NPS)

The voluntary, market-linked pension account regulated by the PFRDA — the one scheme in this pillar without a fixed rate. Returns depend on your chosen mix of equity, corporate debt, government securities, and alternatives. The post covers the Tier I vs Tier II distinction, Active vs Auto allocation choices, the additional ₹50,000 deduction under Section 80CCD(1B) above the 80C cap, the 80CCD(2) employer contribution that even the new regime allows, and the annuity requirement on part of the corpus at 60.

→ What Is National Pension System (NPS)

5. Atal Pension Yojana (APY)

The guaranteed defined-benefit pension aimed at unorganized-sector workers. Unlike NPS, APY promises a fixed monthly pension at 60 — ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 — chosen at registration, with contributions scaled to your entry age. The post covers eligibility, the contribution tables by age and pension slab, the spousal and nominee continuation on death, and how APY sits between EPF and NPS for those outside formal employment.

→ What Is Atal Pension Yojana (APY)

6. Senior Citizen Savings Scheme (SCSS)

The income scheme for those aged 60 and above (with earlier eligibility for certain retirees). It carries 8.2% for Q1 2026, paid out quarterly rather than compounded — functioning as a pension supplement, not a wealth-accumulation vehicle. The post covers the ₹30 lakh maximum investment, the 5-year tenure with a 3-year extension, the 80C eligibility of the deposit, the taxable nature of the interest, and the TDS thresholds that apply to the payouts.

→ What Is Senior Citizen Savings Scheme (SCSS)

7. Post Office Monthly Income Scheme (POMIS)

The scheme built for steady monthly cash flow, crediting interest (7.4% for Q1 2026) to a linked account every month rather than compounding it. The post covers the single and joint account limits (₹9 lakh single / ₹15 lakh joint), the 5-year tenure, the taxable interest with no 80C benefit, and how POMIS compares to SCSS and an annuity for someone who needs predictable monthly income.

→ What Is Post Office Monthly Income Scheme (POMIS)

8. NSC vs KVP

The two post office fixed-term certificates, compared head to head. The National Savings Certificate (NSC) is a 5-year certificate at 7.7% (Q1 2026), compounded annually but paid at maturity, with 80C eligibility. Kisan Vikas Patra (KVP) is a doubling certificate at 7.5% that roughly doubles the investment over its stated tenure but carries no 80C benefit. The post covers where each fits, the taxability of the interest, and the liquidity and pledge rules.

9. Sovereign Gold Bond (SGB)

The government's gold-investment instrument — a direct sovereign obligation issued by the RBI, not an ETF or a paper claim on stored gold. It tracks the market price of gold and pays an additional 2.5% fixed interest a year. The post covers the 8-year tenure with an exit option from year 5, how it compares to physical gold and gold ETFs, and the two changes that reshaped it: fresh issuance stopped in February 2024, and from 1 April 2026 the capital-gains exemption on redemption was narrowed to original subscribers who hold to maturity. Since the secondary market is now the only way in, and secondary buyers are exactly who the narrowed exemption excludes, the tax-free version is closed to new buyers.

→ What Is Sovereign Gold Bond Scheme (SGB)

10. PMJJBY vs PMSBY

India's two low-cost government insurance schemes, both linked to a bank account. PMJJBY (Pradhan Mantri Jeevan Jyoti Bima Yojana) provides ₹2 lakh of life cover for any cause of death at ₹436 a year; PMSBY (Pradhan Mantri Suraksha Bima Yojana) provides ₹2 lakh of accident cover at ₹20 a year. The post covers the eligibility ages, the auto-debit enrolment, what each does and doesn't cover, and why these are protection products rather than savings or investment schemes.

Current rates and key terms at a glance (Q1 2026)

The single most useful reference across the cluster — every scheme's rate, tax treatment, and 80C status side by side. Small-savings rates are reset quarterly by the Ministry of Finance, so treat these as the Q1 2026 snapshot and verify the live rate before acting.

| Scheme | Rate (Q1 2026) | Payout | Tax on returns | 80C eligible | Who it's for |

|---|---|---|---|---|---|

| PPF | 7.1% | Compounded, at maturity | Tax-free (EEE) | Yes | Any resident, long-horizon |

| EPF | 8.25% (FY 2025-26) | At withdrawal | Tax-free (EEE) on completion | Yes (employee share) | Salaried employees |

| SSY | 8.2% | Compounded, at maturity | Tax-free (EEE) | Yes | Girl child under 10 |

| NPS | Market-linked | At 60 (part annuity) | Partly taxable | 80CCD(1B) +₹50K | Voluntary retirement savers |

| APY | Defined benefit | ₹1K–5K/month from 60 | Taxable pension | — | Unorganized-sector workers |

| SCSS | 8.2% | Quarterly | Taxable | Yes | Age 60+ |

| POMIS | 7.4% | Monthly | Taxable | No | Those needing monthly income |

| NSC | 7.7% | Compounded, at maturity | Taxable | Yes | 5-year fixed savers |

| KVP | 7.5% | At maturity (doubles) | Taxable | No | Capital-doubling savers |

| Post office RD | 6.7% | Compounded quarterly, at maturity | Taxable | No | Monthly savers without a lump sum |

| SGB | Gold price + 2.5% | Interest half-yearly | Tax-free at maturity for original subscribers only, from 1 Apr 2026 | No | Gold allocation |

| PMJJBY | ₹436/yr → ₹2L cover | On death | N/A (insurance) | — | Life cover |

| PMSBY | ₹20/yr → ₹2L cover | On accident | N/A (insurance) | — | Accident cover |

Several of these schemes feed directly into the old-regime Section 80C stack — the deduction that shapes the old-vs-new regime decision for salaried filers. That decision, with worked numbers, is laid out in our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26), and the cap mechanics in Section 80C deductions in detail.

Meta-principles synthesized from the cluster

Four patterns emerge from reading the 10 posts together.

Principle 1 — Rates are administered, not market-set, and reset quarterly

Every fixed-rate scheme here (PPF, SSY, SCSS, POMIS, NSC, KVP) has its rate announced by the Ministry of Finance each quarter, independent of bank deposit rates or RBI policy. EPF's rate is declared annually by the EPFO. This is the defining feature of the small-savings system: the rate you earn is a policy decision, not a market outcome. It also means any rate quoted in an article — including this one — is a snapshot that must be re-checked against the current quarter's notification before you act.

Principle 2 — Tax treatment varies more than the rate does

The headline rate is the number savers fixate on, but the tax treatment often matters more. A 7.1% PPF return that's fully tax-free (EEE) can beat an 8% taxable return for someone in the 30% slab. The cluster splits cleanly into three tax buckets: EEE / fully tax-free (PPF, SSY, EPF on completion), taxable interest (SCSS, POMIS, NSC, KVP), and special-case (SGB appreciation tax-free at maturity only for original subscribers from 1 April 2026; NPS partly taxable). Comparing schemes on headline rate alone is the most common mistake the cluster guards against.

Principle 3 — Each scheme is built for a life stage or goal, not for everyone

These schemes are not interchangeable. SSY exists for a girl child's future; SCSS and POMIS for retirees needing income; EPF and NPS for retirement accumulation; PPF for any long-horizon goal; APY for workers outside formal employment; SGB for a gold allocation; PMJJBY/PMSBY for pure protection. Choosing well is mostly a matter of matching the scheme's design — its lock-in, payout style, and eligibility — to your specific goal and stage, not chasing the top rate.

Principle 4 — Safety and liquidity trade off against each other

The sovereign backing that makes these schemes safe usually comes with long lock-ins — 15 years for PPF, 21 for SSY, 5 for SCSS/POMIS/NSC, 8 for SGB. That illiquidity is the price of the guarantee and the tax benefit. This is why these schemes belong alongside, not instead of, an accessible emergency fund and more liquid holdings. Locking money you may need soon into a 15-year instrument defeats the purpose, however attractive the rate.

Where to start

The 10 posts read in any order, but five goal-based sequences make sense depending on your situation.

For retirement accumulation (salaried)

- What Is Employee Provident Fund (EPF) — the mandatory base you already have

- What Is Public Provident Fund (PPF) — the voluntary tax-free top-up

- What Is National Pension System (NPS) — for the extra ₹50,000 deduction and equity exposure

For a child's future

- What Is Sukanya Samriddhi Yojana (SSY) — if you have a girl child under 10

- What Is Public Provident Fund (PPF) — the universal alternative for any child

For retirees needing income

- What Is Senior Citizen Savings Scheme (SCSS) — quarterly payout, highest senior rate

- What Is Post Office Monthly Income Scheme (POMIS) — for monthly cash flow

- What Is Atal Pension Yojana (APY) — if you're approaching 60 outside formal employment

For tax-saving under Section 80C

- What Is Section 80C Deduction — the ₹1.5 lakh cap and how schemes compete for it

- What Is Public Provident Fund (PPF) — the cleanest 80C instrument

- NSC vs KVP — the fixed-term certificate options

For safety-first allocation and protection

- What Is Sovereign Gold Bond Scheme (SGB) — a sovereign gold allocation

- PMJJBY vs PMSBY — ₹2 lakh of life and accident cover for under ₹500 a year

In every case, the educational content gives you the vocabulary; matching a scheme to your actual goals and tax situation is where a professional adds value.

The standing recommendation across all 10 posts

Every post in this pillar ends the same way: verify the current quarter's rate and rules against the primary source, and consult a qualified professional before committing. This isn't boilerplate. Small-savings rates change four times a year, eligibility rules carry exceptions, and the tax treatment interacts with your regime choice and slab in ways a general article can't resolve for you. The primary sources are freely accessible — the Ministry of Finance's quarterly small-savings notifications, India Post for the post office schemes, the EPFO for EPF, the PFRDA for NPS, and the RBI for SGB. Combine this educational content with a current primary-source check and, where the sums are meaningful, a SEBI-registered investment adviser or Chartered Accountant who knows your situation.

These schemes are deliberately conservative tools. Their value is certainty, sovereign backing, and tax efficiency — not maximum return. Used well, they form the stable base of a portfolio that can then take measured risk elsewhere. For the broader vocabulary of Indian taxation that surrounds the 80C-eligible schemes here, see our tax concepts overview.

Frequently asked questions

Which Indian government savings scheme has the highest interest rate in Q1 2026? Among the major government savings schemes, Sukanya Samriddhi Yojana (SSY) and the Senior Citizen Savings Scheme (SCSS) carry the highest rate at 8.2% for Q1 2026, followed by EPF at 8.25% (the FY 2023-24 EPFO-declared rate). PPF is 7.1%, NSC 7.7%, KVP 7.5%, and POMIS 7.4%. SSY is restricted to a girl child under 10, and SCSS to those aged 60 and above, so the highest-rate schemes are eligibility-limited. NPS has no fixed rate — it is market-linked. Small-savings rates are reset every quarter by the Ministry of Finance, so verify the current quarter's rate before acting.

Which government schemes qualify for the Section 80C tax deduction? PPF, EPF (employee contribution), SSY, NSC, SCSS, and the 5-year post office time deposit all qualify for the Section 80C deduction of up to ₹1,50,000 a year — but only under the old tax regime. The ₹1.5 lakh cap is shared across all of them combined. NPS adds a separate ₹50,000 deduction under Section 80CCD(1B), above the 80C cap. KVP and POMIS do not qualify for 80C, and SGB interest is taxable. Under the new tax regime, none of these 80C deductions apply, which is part of the old-vs-new regime trade-off.

What is the difference between PPF, EPF and NPS? PPF is a voluntary 15-year account open to any Indian resident, with a government-fixed rate (7.1% in Q1 2026) and fully tax-free (EEE) returns. EPF is a mandatory retirement scheme for salaried employees, funded by a 12% employee contribution matched by the employer, earning the EPFO-declared rate (8.25% for FY 2023-24). NPS is a voluntary, market-linked pension account regulated by PFRDA, where returns depend on your chosen mix of equity and debt and part of the corpus must buy an annuity at retirement. PPF and EPF offer certainty; NPS offers growth potential with market risk.

Are returns from government savings schemes tax-free? It depends on the scheme. PPF, SSY and EPF (on completion) enjoy EEE treatment — exempt at contribution, accrual, and withdrawal — so returns are fully tax-free. SCSS, POMIS, NSC and KVP pay taxable interest, added to your income and taxed at your slab rate. SGB capital appreciation is tax-free at maturity only for an original subscriber who held throughout, following the Finance Act 2026 change effective 1 April 2026, and taxable for anyone who bought on the exchange or redeems early, while its 2.5% interest is always taxable. NPS is partly tax-free at withdrawal with the rest taxed. Tax treatment is scheme-specific and changes with the Budget, so confirm the current rules for your situation with a CA.

Sources

- Ministry of Finance, Government of India — quarterly small-savings interest rate notifications — dea.gov.in

- Department of Posts (India Post) — PPF, SSY, SCSS, POMIS, NSC, KVP scheme rules — indiapost.gov.in

- Employees' Provident Fund Organisation (EPFO) — epfindia.gov.in

- Pension Fund Regulatory and Development Authority (PFRDA) — NPS and APY — pfrda.org.in

- Reserve Bank of India (RBI) — Sovereign Gold Bond scheme — rbi.org.in

- National Savings Institute, Ministry of Finance — nsiindia.gov.in

- Income Tax Department of India — tax treatment of scheme returns — incometax.gov.in

You might also like

PPF pays 7.1% for Jul-Sep 2026, unchanged since 2020. See the Rs 500 to Rs 1.5 lakh limits, EEE tax, 15-year lock-in, withdrawal rules and a maturity example.

13 min read

What is EPF? The 8.25% FY 2025-26 interest rate, the 12% + 12% contribution split, the new EPF Scheme 2026 withdrawal rules, and the tax treatment explained.

14 min read

NPS entry now runs to age 85, and non-government exits need only 20% annuity since December 2025. What the new tax regime allows, and what it takes away.

17 min read