Income Tax Guide for Salaried Employees FY 2025-26

By Tapabrata Biswas · Updated July 19, 2026 · 28 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

A new Income-tax Act took effect in India on 1 April 2026. The return you file this July has nothing to do with it.

That sentence is the most useful thing in this guide, because the filing season is currently full of the opposite. Of twenty pages we read ranking for salaried filing queries, eleven say nothing about which Act governs the return, and three actively frame the current filing under the 2025 Act. One, written by a named chartered accountant, structures its entire guide around the new statute and never states which law actually applies.

The Income Tax Department settles it in one line. Its transition FAQ says taxpayers filing returns for AY 2026-27 in July 2026 will do so using the forms prescribed under the old Act.

This guide covers the FY 2025-26 return under the Income-tax Act 1961: which Act applies and why the distinction matters, the slabs and the rebate arithmetic, which deductions survive the new regime, how the regime choice is actually exercised, reading Form 16 and reconciling it, choosing between ITR-1 and ITR-2, the due date, and the 30-day verification rule that quietly turns punctual returns into late ones.

It's educational, and it isn't tax-planning advice. The regime that fits any individual depends on a salary structure and deduction profile no article can see, and a chartered accountant who has looked at your actual numbers is the right person for a borderline call, a capital-gains question, or any notice from the department.

Which Income Tax Act governs the return you file this July?

The Income-tax Act 1961 governs the return filed in July 2026 for FY 2025-26 income, even though the Income-tax Act 2025 came into force on 1 April 2026. The department's transition FAQ is explicit that returns for AY 2026-27 are filed using the forms prescribed under the old Act.

The mechanics are worth understanding, because the two Acts genuinely run in parallel right now. The 1961 Act stands repealed from 1 April 2026, yet its provisions continue to govern every tax year beginning before that date. Assessments, appeals and other proceedings for earlier years also continue under it until they conclude. Section 536(2)(c) of the new Act preserves the old one for exactly this purpose, with Section 6 of the General Clauses Act 1897 as a backstop.

So the e-filing portal is currently doing two things at once. Returns for AY 2026-27 use old-Act forms. Advance tax for Tax Year 2026-27, which started in June 2026, follows the new Act.

The Tax Year concept itself begins later than most coverage implies. It applies from 1 April 2026, meaning income earned during FY 2026-27, which will be called Tax Year 2026-27. Nothing about the return you file this month uses that vocabulary.

Two reassurances follow from the department's own FAQ. The new regime survives the transition, appearing as Section 202 of the 2025 Act and remaining the default. And an option already exercised under the old Act is treated as if it had been made under the equivalent provision of the new Act, so nobody needs to re-elect anything.

Where this bites in practice is section numbers. The renumbering is real: Section 139(1) becomes Section 263(1), and the rebate now sits at a different number. At least one insurer's page ranking this season describes the rebate as "Section 156" without ever mentioning Section 87A, which means a reader searching the section they actually need won't match it. For this year's return, the 1961 numbering is the one that applies.

What are the FY 2025-26 slabs under each regime?

Under the new regime for FY 2025-26, income up to ₹4,00,000 is nil and the top 30% rate begins above ₹24,00,000. The department publishes the table with cumulative amounts, which is how the tax is actually computed.

| Taxable income | Tax |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 to ₹8,00,000 | 5% above ₹4,00,000 |

| ₹8,00,001 to ₹12,00,000 | ₹20,000 plus 10% above ₹8,00,000 |

| ₹12,00,001 to ₹16,00,000 | ₹60,000 plus 15% above ₹12,00,000 |

| ₹16,00,001 to ₹20,00,000 | ₹1,20,000 plus 20% above ₹16,00,000 |

| ₹20,00,001 to ₹24,00,000 | ₹2,00,000 plus 25% above ₹20,00,000 |

| Above ₹24,00,000 | ₹3,00,000 plus 30% above ₹24,00,000 |

One detail the department states that almost no summary carries: the new-regime slab table is identical across all three age brackets. Under 60, 60 to 80, and 80 plus all face the same thresholds. The higher exemption for senior citizens exists only in the old regime.

| Taxable income | Old regime, under 60 | Old regime, 60 to 80 |

|---|---|---|

| Exemption threshold | ₹2,50,000 | ₹3,00,000 |

| Next band at 5% | to ₹5,00,000 | to ₹5,00,000 |

| ₹5,00,001 to ₹10,00,000 | ₹12,500 plus 20% | ₹10,000 plus 20% |

| Above ₹10,00,000 | ₹1,12,500 plus 30% | ₹1,10,000 plus 30% |

Health and education cess of 4% applies on the tax plus any surcharge, in both regimes. Surcharge starts above ₹50 lakh at 10%, rises to 15% between ₹1 crore and ₹2 crore, and 25% between ₹2 crore and ₹5 crore. Above ₹5 crore the two regimes diverge sharply: the new regime caps surcharge at 25% while the old regime goes to 37%. For the full slab structure across both regimes, our income tax slab explainer sets it out in more detail.

Is salary up to ₹12.75 lakh really tax-free?

A salaried person earning ₹12,75,000 gross pays no tax under the new regime for FY 2025-26, and the arithmetic works out exactly rather than approximately.

| Step | Amount |

|---|---|

| Gross salary | ₹12,75,000 |

| Less standard deduction under Section 16(ia) | (₹75,000) |

| Taxable income | ₹12,00,000 |

| Slab tax before rebate | ₹60,000 |

| Less Section 87A rebate | (₹60,000) |

| Tax after rebate | ₹0 |

| Cess at 4% | ₹0 |

| Total liability | ₹0 |

The ₹60,000 of slab tax is ₹20,000 on the ₹4 lakh to ₹8 lakh band at 5%, plus ₹40,000 on the ₹8 lakh to ₹12 lakh band at 10%. The rebate cap is also ₹60,000. They cancel precisely, which is why this particular figure became the headline.

Three numbers get conflated constantly, and keeping them apart is most of the battle. Only three of the fifteen pages we read on this topic do it cleanly.

| Figure | What it is |

|---|---|

| ₹60,000 | The maximum Section 87A rebate under the new regime |

| ₹12,00,000 | The taxable income ceiling for the rebate |

| ₹12,75,000 | The gross salary at which tax reaches nil, after the standard deduction |

Two qualifications matter. The department words the rebate condition as taxable income, and the Budget speech announcing it excluded special-rate income such as capital gains from the claim. So a person with ₹11 lakh salary and ₹3 lakh of equity gains isn't inside this outcome, and only two of fifteen pages mention that carve-out at all.

The old-regime rebate still exists but is far narrower: capped at ₹12,500 and available only where taxable income does not exceed ₹5,00,000.

What happens just above the threshold

Marginal relief prevents a cliff at ₹12 lakh. Without it, a rupee of extra income would trigger the full slab tax. The rule caps the tax so it cannot exceed the amount by which taxable income exceeds ₹12,00,000.

Take ₹13,00,000 gross, giving ₹12,25,000 taxable after the standard deduction. Slab tax computes to ₹63,750. Marginal relief caps it at ₹12,25,000 minus ₹12,00,000, which is ₹25,000, so tax payable is ₹25,000 plus 4% cess, or ₹26,000. The relief tapers as income rises and runs out around ₹12,70,000 taxable, where normal slab tax finally falls below the cap. Two of fifteen pages show this arithmetic.

Above the rebate

| Item | ₹18,00,000 gross | ₹25,00,000 gross |

|---|---|---|

| Standard deduction | (₹75,000) | (₹75,000) |

| Taxable income | ₹17,25,000 | ₹24,25,000 |

| Slab tax | ₹1,45,000 | ₹3,07,500 |

| Cess at 4% | ₹5,800 | ₹12,300 |

| Total tax | ₹1,50,800 | ₹3,19,800 |

| Effective rate on gross | 8.4% | 12.8% |

The effective rate stays far below the marginal slab rate even at ₹25 lakh, because the lower bands are taxed at lower rates throughout. Our marginal versus effective rate explainer works through why that gap persists.

Which deductions survive under the new regime?

The Income Tax Department lists only two Chapter VIA deductions available to a salaried taxpayer under the new regime: Section 80CCD(2) and Section 80CCH.

Section 80CCD(2) covers the employer's contribution to a pension scheme, with a deduction limit of 14% of salary, and it applies for all categories of employers. Section 80CCH covers the Agniveer Corpus Fund. Section 80JJAA also survives, but it's a business deduction and doesn't reach a salaried filer.

That makes the employer's NPS contribution the one meaningful Chapter VIA route left in the default regime, which is a considerable change from how tax planning worked five years ago. The mechanics of that contribution sit in our National Pension System explainer.

The Section 24(b) trap

Housing loan interest under Section 24(b) is allowed in the new regime, and this is where the published record is worst. The department's own salaried page lists "Section 24(b)" with no qualifier, which reads as though home loan interest survives generally. It doesn't.

The department's detailed entry gives the real rule: the allowable value is the actual amount without any limit, but any resulting loss under the head income from house property cannot be set off against other heads and cannot be carried forward. And the ₹2,00,000 self-occupied cap appears only in the department's old-regime section.

In practice that means let-out property only. A salaried person paying interest on the flat they live in gets nothing for it under the new regime. Nine commercial pages we read state this correctly while the government's own summary page is ambiguous, which is an unusual inversion worth flagging plainly.

What the new regime removes

| Deduction or exemption | Old regime | New regime |

|---|---|---|

| Standard deduction | ₹50,000 | ₹75,000 |

| Section 80C, up to ₹1.5 lakh | Available | Not available |

| HRA under Section 10(13A) | Available | Not available |

| Section 80D health insurance | Available | Not available |

| Section 24(b), self-occupied | Up to ₹2,00,000 | Not available |

| Section 24(b), let-out | Available | Available, no limit |

| Section 80CCD(2), employer NPS | Available | Available, 14% of salary |

One caution on that first row. The ₹75,000 new-regime figure is confirmed by the Budget announcement of 1 February 2025, which stated the ₹12.75 lakh salaried threshold arises "due to standard deduction of ₹75,000." The ₹50,000 old-regime figure appears on a department FAQ page that is demonstrably stale elsewhere, so we cite it with that caveat attached and without calling it dated-confirmed.

Which brings up something readers deserve to know.

The department contradicts itself

The Income Tax Department currently publishes two live pages that disagree. Its salaried page for AY 2026-27, reviewed 9 July 2026, gives the ₹60,000 rebate and the ₹12 lakh ceiling. Its regime-comparison FAQ still publishes the older ₹25,000 rebate at ₹7 lakh, and states a ₹50,000 standard deduction "for both old and new tax regimes from AY 2024-25 onwards."

The second page carries no visible review date, and it ranks for regime-comparison queries. One competitor page we read reproduces those stale figures wholesale.

The dated, on-point authority for FY 2025-26 is the salaried page and the Budget announcement. Where a government page and a government page conflict, the one with a review date and the one matching the Finance Act should govern, and we've sourced accordingly throughout.

How do you actually choose the old regime?

A salaried employee with no business income switches regime directly in the return each year and doesn't need Form 10-IEA. The department states that non-business taxpayers can exercise the option every year directly in the ITR, provided the return is filed on or before the Section 139(1) due date.

Taxpayers with business or professional income face a materially stricter regime. They must furnish Form 10-IEA by the due date, need it again to switch back, and re-entry to the new regime is available only in a subsequent assessment year and only once in a lifetime.

Two of fifteen pages we read draw this distinction, which is odd given how much it matters. For a salaried filer, the practical consequence is compact: file by 31 July and the old regime is available by ticking a box; file late and it isn't available at all for that year.

The new regime became the default through the Finance Act 2023, which amended Section 115BAC with effect from AY 2024-25.

When does the old regime still win?

The old regime beats the new one when deductions and exemptions cut taxable income by more than the gap between the two rate structures. For a renting employee in a metro with a maxed Section 80C and home loan interest, that threshold is reachable.

The old regime's arithmetic is harsher at the top: its 30% rate starts at ₹10 lakh against ₹24 lakh in the new regime, and its rebate is capped at ₹12,500 against ₹60,000. So the deductions have to work hard to overcome both.

The largest of them for a salaried renter is HRA. Under Section 10(13A) the exemption is the lowest of three figures: actual HRA received, rent paid minus 10% of basic salary, or 50% of basic in a metro (40% elsewhere).

| Component | Monthly |

|---|---|

| Basic salary | ₹50,000 |

| HRA received | ₹25,000 |

| Rent paid | ₹30,000 |

Running Rule 2A on those figures: actual HRA is ₹25,000; rent minus 10% of basic is ₹30,000 less ₹5,000, or ₹25,000; and 50% of basic in Mumbai is ₹25,000. All three land at ₹25,000 a month, so ₹3,00,000 a year is excluded from taxable income. Where annual rent exceeds ₹1,00,000, the landlord's PAN must be reported to the employer, per CBDT Circular 8/2013. Our HRA exemption explainer covers the metro and non-metro distinction in full.

Section 80C carries a ₹1,50,000 cap shared across every eligible instrument combined, covering PPF, ELSS, life insurance premiums, EPF, home loan principal and Sukanya Samriddhi Yojana among others. The detail sits in our Section 80C explainer.

Stack a ₹3 lakh HRA exemption, a ₹1.5 lakh Section 80C claim, ₹2 lakh of self-occupied housing interest and a ₹25,000 Section 80D premium and the old regime removes ₹6.75 lakh from taxable income before the slabs apply. Whether that beats the new regime depends entirely on the income level and on whether those deductions are real, in the sense of already being paid, which is precisely the calculation a chartered accountant should run against actual figures.

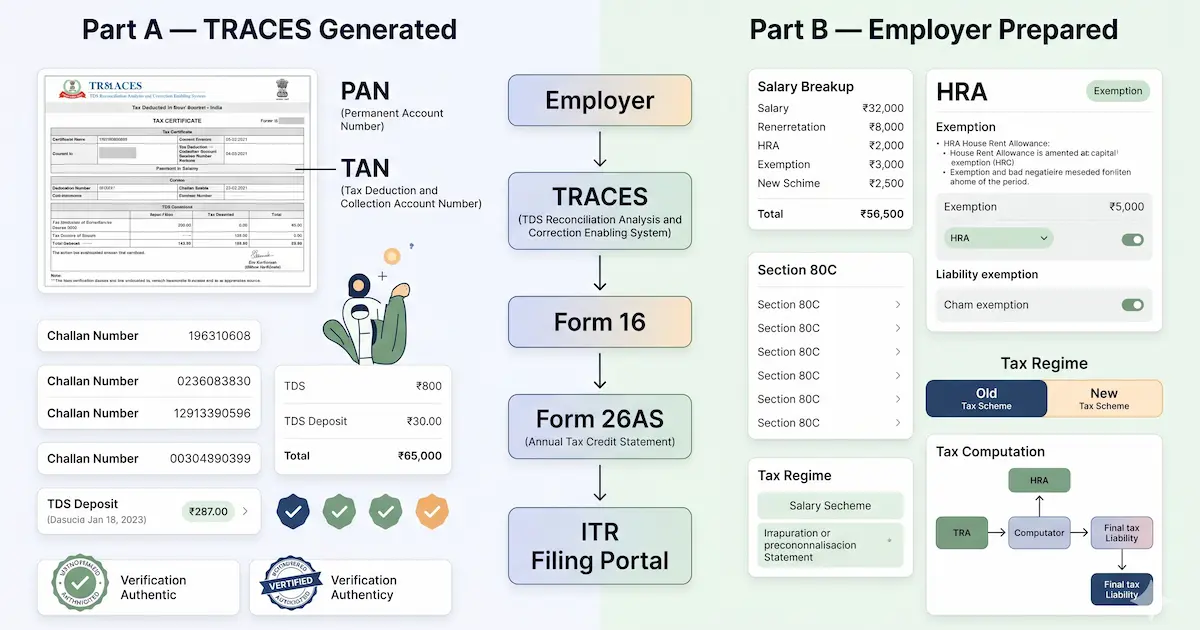

How do you read Form 16 and reconcile it?

Form 16 is the TDS certificate an employer issues under Section 192, certifying salary paid and tax deducted during the financial year. Part A carries the quarter-by-quarter record of tax deducted and deposited against your PAN. Part B carries the salary breakup.

TDS isn't the final tax. It's an advance against it, estimated by the employer from the information the employer has. Total your actual liability at filing and compare: more TDS than liability produces a refund, less produces a balance payable. Our TDS explainer covers how the deduction works across payment types, and Form 16 in detail walks the fields.

Reconciliation matters because the employer only sees what the employer pays. Form 16 should agree with Form 26AS, the consolidated tax-credit statement, and with the Annual Information Statement, which additionally reports interest, dividends and securities transactions.

A worked case where the two diverge:

| Item | Amount |

|---|---|

| Salary tax plus cess, covered by employer TDS | ₹97,500 |

| Long-term capital gains on equity | ₹2,00,000 |

| Less Section 112A exemption | (₹1,25,000) |

| Taxable LTCG ₹75,000 at 12.5% plus 4% cess | ₹9,750 |

| Total liability | ₹1,07,250 |

| TDS already deducted on salary | ₹97,500 |

| Balance payable at filing | ₹9,750 |

Anything outside salary, whether capital gains, fixed deposit interest or freelance income, has to be added by the filer and the balance paid as self-assessment tax before the return goes in.

ITR-1 or ITR-2: which form applies?

ITR-1 (Sahaj) applies to a resident individual, other than not ordinarily resident, with total income up to ₹50 lakh from salary or pension, one house property, other sources such as interest and dividend, agricultural income up to ₹5,000, and capital gains under Section 112A up to ₹1,25,000.

Eleven conditions push a filer out of ITR-1, and any single one is enough. The department lists them: being a company director; having short-term capital gain; having Section 112A long-term gain above ₹1,25,000; holding unlisted equity shares at any time in the year; holding any asset, including a financial interest in any entity, outside India; having signing authority in a foreign account; having income from any source outside India; having tax deducted under Section 194N; having payment or deduction of tax deferred on ESOPs; having any brought-forward loss or loss to be carried forward under any head; and total income above ₹50 lakh, excluding Section 112A gains up to ₹1,25,000.

ITR-2 covers individuals not eligible for ITR-1 with income under any head other than profits and gains of business or profession.

One caveat on this section. Media coverage of CBDT's notified AY 2026-27 forms reported that ITR-1 now accepts up to two house properties. The department's own AY 2026-27 help page, reviewed 9 July 2026, still states one house property, and we could not retrieve the notified form itself because the site hosting it blocks automated access. We've stated the department's current published position and flagged the discrepancy without choosing between them, and anyone with two properties should confirm with a CA or the utility itself before filing.

What is the due date, and has it been extended?

31 July 2026 for salaried individuals filing ITR-1 or ITR-2, with no extension notified as of 19 July 2026.

Neither government help page states a due date directly, which is a curious gap. The corroboration comes from the department's own helpdesk banner: from 25 July 2026, its support lines operate 24x7 until 23:59 hrs on 31 July 2026. A department staffing to the minute is reasonable evidence of the deadline it expects.

The portal's news feed, read on 19 July 2026, carried no extension item. Its most recent entries were a TDS notification dated 13 July and utility releases for ITR-7 and ITR-5.

Worth knowing, though: the previous year's deadline moved from 31 July to 15 September 2025. An extension this year is neither announced nor impossible, so the portal is the place to check close to the date.

| Milestone | Date |

|---|---|

| ITR-1 and ITR-2 due date | 31 July 2026 |

| Belated return | 31 December 2026 |

| E-verification window | 30 days from filing |

Filing late costs more than the fee under Section 234F and the interest under Section 234A. It also forfeits the old-regime option for that year, since the department conditions the regime choice on filing by the Section 139(1) due date. Two of twenty pages we read mention that consequence.

What happens if you do not e-verify within 30 days?

The verification date becomes the filing date, which is the consequence nearly every guide states incorrectly. The limit is 30 days from the date of filing, set by Notification No. 2/2024 dated 31 March 2024.

Verify inside 30 days and the upload date counts as the date of furnishing the return. Verify after 30 days and the department treats the date of e-verification or ITR-V submission as the date of furnishing instead, with all consequences of late filing following as applicable.

Work that through. A return uploaded on 28 July 2026 and verified on 5 September becomes a September filing. The upload was punctual; the return is late. Late fees, interest, and the loss of the old-regime option all attach to a filing the taxpayer believes was submitted on time.

A return never verified at all is treated as invalid, though a condonation request can be submitted for genuine delays.

Thirteen of twenty pages we read omit the 30-day window entirely. Of those that mention it, most describe an unverified return as simply "invalid," which conflates the never-verified case with the late-verified one. They're different outcomes with different costs.

What this guide deliberately does not cover

This explains how salaried income tax works for one specific year under one specific Act. It doesn't recommend a regime, a deduction, an instrument or a filing strategy to anyone, and the worked examples exist to show the arithmetic, never to argue for a choice.

The regime decision turns on a salary structure, rent, loan position and investment profile that no article can see. A chartered accountant who has looked at your numbers is the right person for a borderline call, and for anything involving capital gains, foreign assets, ESOPs, multiple employers or a notice from the department.

Several things sit outside the scope on purpose. Business and professional income, presumptive taxation, and the audit deadlines that follow from them are a different filing entirely. Advance tax scheduling for taxpayers with substantial non-salary income is covered only where it touches self-assessment tax at filing. The Income-tax Act 2025 appears here solely to establish that it doesn't apply to this return; its provisions will matter for the FY 2026-27 filing.

Four sourcing limits are worth stating on a page people file real returns from. The old-regime ₹50,000 standard deduction comes from a department page that is stale on other figures, so it is not dated-confirmed. The ITR-1 house-property discrepancy above is unresolved. A portal page carries an internally incoherent fragment about a 31 August date for non-audit cases, which we have not reproduced because it contradicts the 31 July date stated everywhere else. And the due-date position was verified on 19 July 2026 and should be re-checked before filing.

Frequently asked questions

Which Income Tax Act applies to the return I file in July 2026? The Income-tax Act 1961. The Income-tax Act 2025 came into force on 1 April 2026, but it governs income earned from that date onward. The Income Tax Department's own transition FAQ states that taxpayers filing returns for AY 2026-27, pertaining to the period governed by the old Act, in July 2026 will do so using the forms prescribed under the old Act. The 1961 Act stands repealed from 1 April 2026, yet its provisions continue to govern all tax years beginning before that date, and assessments and appeals for earlier years also continue under it. The new Tax Year concept begins with income earned in FY 2026-27, which will be called Tax Year 2026-27.

What are the income tax slabs for FY 2025-26? Under the new regime, income up to ₹4,00,000 is nil, ₹4,00,001 to ₹8,00,000 is 5%, ₹8,00,001 to ₹12,00,000 is 10%, ₹12,00,001 to ₹16,00,000 is 15%, ₹16,00,001 to ₹20,00,000 is 20%, ₹20,00,001 to ₹24,00,000 is 25%, and above ₹24,00,000 is 30%. The new-regime slabs are identical for all three age brackets, so there is no higher exemption for senior citizens. Under the old regime, income up to ₹2,50,000 is nil, ₹2,50,001 to ₹5,00,000 is 5%, ₹5,00,001 to ₹10,00,000 is 20%, and above ₹10,00,000 is 30%, with the exemption threshold rising to ₹3,00,000 for those aged 60 to 80. Health and education cess of 4% applies on the tax plus any surcharge in both regimes.

Is salary up to ₹12.75 lakh really tax-free? Yes for a salaried person under the new regime, and the arithmetic is exact rather than approximate. The ₹75,000 standard deduction reduces ₹12,75,000 gross to ₹12,00,000 taxable. Slab tax on ₹12,00,000 is ₹60,000, being ₹20,000 on the ₹4 lakh to ₹8 lakh band at 5% plus ₹40,000 on the ₹8 lakh to ₹12 lakh band at 10%. The Section 87A rebate for the new regime is capped at ₹60,000 and applies where taxable income does not exceed ₹12,00,000, so it cancels that ₹60,000 precisely and the cess computes on zero. Note the department words the condition as taxable income, and the Budget speech excluded special-rate income such as capital gains from the claim.

Which deductions survive under the new tax regime? Very few, and the list is shorter than most summaries suggest. The Income Tax Department lists Section 80CCD(2), the employer's contribution to a pension scheme, at a deduction limit of 14% of salary, and Section 80CCH for the Agniveer Corpus Fund. Section 80JJAA also survives but is a business deduction irrelevant to a salaried reader. Section 24(b) for housing loan interest is allowed, and this is where most pages go wrong: under the new regime it applies to let-out property only, with actual value and no limit, though any resulting loss under house property cannot be set off against other heads or carried forward. The ₹2,00,000 self-occupied interest deduction exists only in the old regime. Section 80C, HRA under Section 10(13A), and Section 80D are all unavailable in the new regime.

Do salaried employees need Form 10-IEA to choose the old regime? No, provided they have no business or professional income. The Income Tax Department states that non-business taxpayers can exercise the option to change from the default regime every year directly in the ITR, and that the return must be filed on or before the due date specified under Section 139(1). Taxpayers with business or professional income are in a different position entirely: they must furnish Form 10-IEA by the Section 139(1) due date, they need it again to switch back, and re-entry to the new regime is available only in a subsequent assessment year and only once in a lifetime. The practical consequence for a salaried filer is that missing the due date costs the old-regime option for that year.

What is the ITR filing due date for FY 2025-26? 31 July 2026 for salaried individuals filing ITR-1 or ITR-2, and no extension had been notified as of 19 July 2026. The Income Tax Department's own helpdesk banner corroborates the date, stating that from 25 July 2026 its support lines operate 24x7 until 23:59 hrs on 31 July 2026. The portal's news feed carried no extension item. That said, the previous year's deadline was extended from 31 July to 15 September 2025, so the position is worth re-checking on the portal close to the date. A belated return remains possible until 31 December 2026, but filing late forfeits the option to choose the old regime for that year.

Should a salaried filer use ITR-1 or ITR-2? ITR-1 (Sahaj) applies to a resident individual, other than not ordinarily resident, with total income up to ₹50 lakh from salary or pension, one house property, other sources such as interest and dividend, agricultural income up to ₹5,000, and capital gains under Section 112A up to ₹1,25,000. Eleven conditions push a filer to ITR-2, and any single one is enough: being a company director, having short-term capital gain, having Section 112A long-term gain above ₹1,25,000, holding unlisted equity shares at any time in the year, holding any asset or financial interest outside India, having signing authority in a foreign account, having income from any source outside India, having tax deducted under Section 194N, having deferred ESOP tax, having any brought-forward or carried-forward loss, or total income above ₹50 lakh.

What happens if you do not e-verify within 30 days? The filing date changes, which is the consequence most guides state incorrectly. The Income Tax Department sets the limit at 30 days from the date of filing, under Notification No. 2/2024 dated 31 March 2024. Verify within 30 days and the upload date counts as the date of furnishing the return. Verify after 30 days and the date of e-verification or ITR-V submission is treated as the date of furnishing instead, with all consequences of late filing following as applicable. So a return uploaded on 28 July and verified in September becomes a September filing, carrying late-filing consequences even though it was uploaded on time. A return never verified is treated as invalid, though a condonation request can be submitted for genuine delays.

Sources

-

Income Tax Department, Salaried Individuals for AY 2026-27, page last reviewed or updated 9 July 2026 (the new and old regime slab tables, the Section 87A rebate limits, surcharge rates, the default-regime rule, the new-regime deduction list including 80CCD(2) at 14% and Section 24(b), and the full ITR-1 and ITR-2 conditions) incometax.gov.in

-

Income Tax Department, Objective and scope of the new Act, FAQ (that returns for AY 2026-27 are filed under the forms prescribed by the old Act, that the 1961 Act continues to govern tax years beginning before 1 April 2026, and that the Tax Year concept starts with FY 2026-27) incometax.gov.in

-

Income Tax Department, ITR-V FAQs, 30-day timeline for e-verification (the 30-day limit under Notification No. 2/2024 dated 31 March 2024, and the rule that late verification makes the verification date the date of furnishing) incometax.gov.in

-

Income Tax Department, Income Tax Returns, e-filing services (which ITR forms apply for AY 2026-27 under the Income Tax Act 1961) incometax.gov.in

-

Income Tax Department, Latest news feed, read 19 July 2026 (no due-date extension notified, and the 24x7 helpdesk banner running to 23:59 hrs on 31 July 2026) incometax.gov.in

-

Press Information Bureau, Ministry of Finance, Union Budget 2025-26, 1 February 2025 (the Rs 75,000 standard deduction and the Rs 12.75 lakh salaried threshold, and the exclusion of special-rate income) pib.gov.in

-

Press Information Bureau, The Income-tax Act 2025 comes into force, 1 April 2026 (commencement on 1 April 2026, passage on 12 August 2025, assent on 21 August 2025, and the Income-tax Rules 2026 notified 20 March 2026) pib.gov.in

You might also like

A plain-English guide to the core tax concepts in India and the US: slabs, deductions, TDS, GST, capital gains, FICA, and an India and US tax glossary.

16 min read

Income tax slabs in India for FY 2025-26 (AY 2026-27): new and old regime rates, the ₹12.75 lakh salaried zero-tax point, the 87A rebate, surcharge, and cess.

13 min read

What is Form 16? The password to open it, Part A vs Part B, why you can't download it from TRACES, the 15 June 2026 deadline, and filing ITR without it.

15 min read