Income Tax Slab India Explained: How the Old and New Regime Slabs Actually Work

By Tapabrata Biswas · Published May 23, 2026 · 10 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led explainer of India's income tax slab structure as notified by the Income Tax Department. It is not tax advice. Tax law changes annually with each Union Budget, individual circumstances vary, and the correct application of slabs and exemptions to your specific salary structure, deductions, and other income depends on details that only a qualified Chartered Accountant familiar with your situation can correctly assess. Consult a CA before filing your ITR or making tax-relevant financial decisions.

India's income tax structure has two parallel slab systems running side by side — the new regime (default since FY 2023-24) and the old regime (continues as an option for taxpayers who explicitly elect it). Both produce progressive taxation, meaning the rate increases as income rises through bands. Under the new regime for FY 2025-26 (AY 2026-27), a salaried person earning up to ₹12 lakh effectively pays zero income tax after the standard deduction and Section 87A rebate. Above ₹12 lakh, slab rates apply, and additional surcharge plus a 4% Health and Education Cess layer on top of the slab-calculated tax.

This post covers what tax slabs actually are, the current new regime and old regime slabs as notified by the Ministry of Finance, the Section 87A rebate that creates the ₹12 lakh effective-zero-tax threshold, surcharge and cess calculations, and a worked example showing the full tax computation step by step.

What an income tax slab actually is

A tax slab is a band of annual income that is taxed at a specific percentage rate. India uses a progressive tax structure — the first band of income is taxed at a lower rate (or zero), and each higher band is taxed at a progressively higher rate.

The structural mechanic, illustrated:

- A person earning ₹8 lakh doesn't pay 10% on the entire ₹8 lakh

- They pay 0% on the first slab band, 5% on the second slab band, and 10% only on the portion of income that falls in the third slab band

- The effective rate (total tax ÷ total income) is therefore always lower than the marginal slab rate they reach

This structural concept is shared with most income-tax systems globally — the US, UK, Canada, Australia, and India all use progressive slabs. The differences are the specific band thresholds and percentage rates set by each country's legislature.

The Indian slab structure is notified by the Ministry of Finance through the annual Union Budget, presented to Parliament each February. The slabs that apply to a given financial year are confirmed by the Finance Act passed shortly after the Budget speech, then implemented by the Income Tax Department and the Central Board of Direct Taxes.

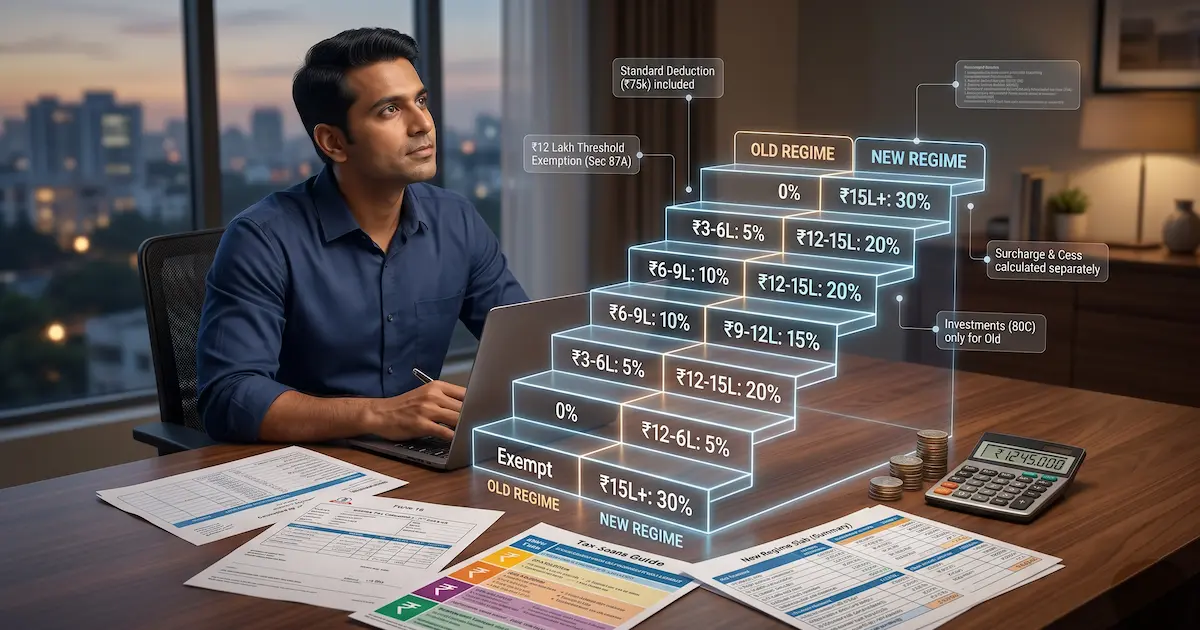

The new regime — slabs and structure for FY 2025-26

The new regime was introduced in FY 2020-21 and made the default option in FY 2023-24 — meaning taxpayers who don't actively elect the old regime are automatically assessed under new regime slabs.

New regime slabs for FY 2025-26 (Assessment Year 2026-27):

| Total income | Tax rate |

|---|---|

| Up to ₹4,00,000 | 0% |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Standard deduction: ₹75,000 (raised from ₹50,000 in Budget 2024 specifically for the new regime).

Section 87A rebate: Up to ₹60,000 if total income (after standard deduction) is up to ₹12 lakh. This rebate is the mechanism that produces the widely-cited "₹12 lakh zero tax" figure under the new regime — the slab calculation gives a positive tax liability, then the 87A rebate reduces it to zero.

What the new regime disallows:

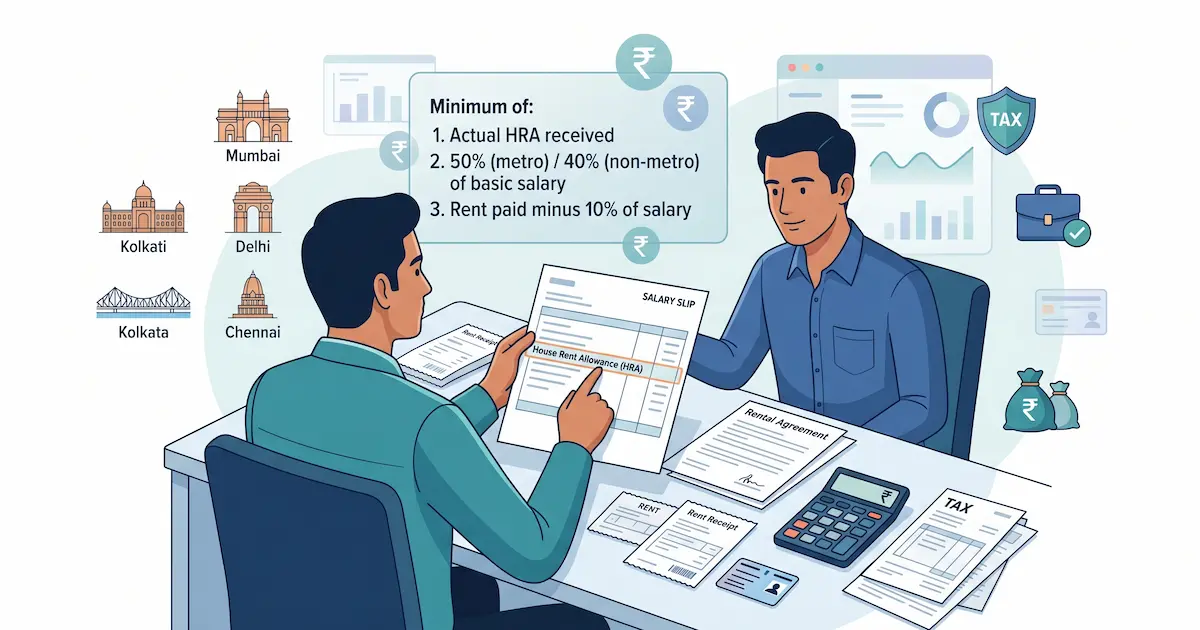

- HRA exemption — see what is HRA exemption

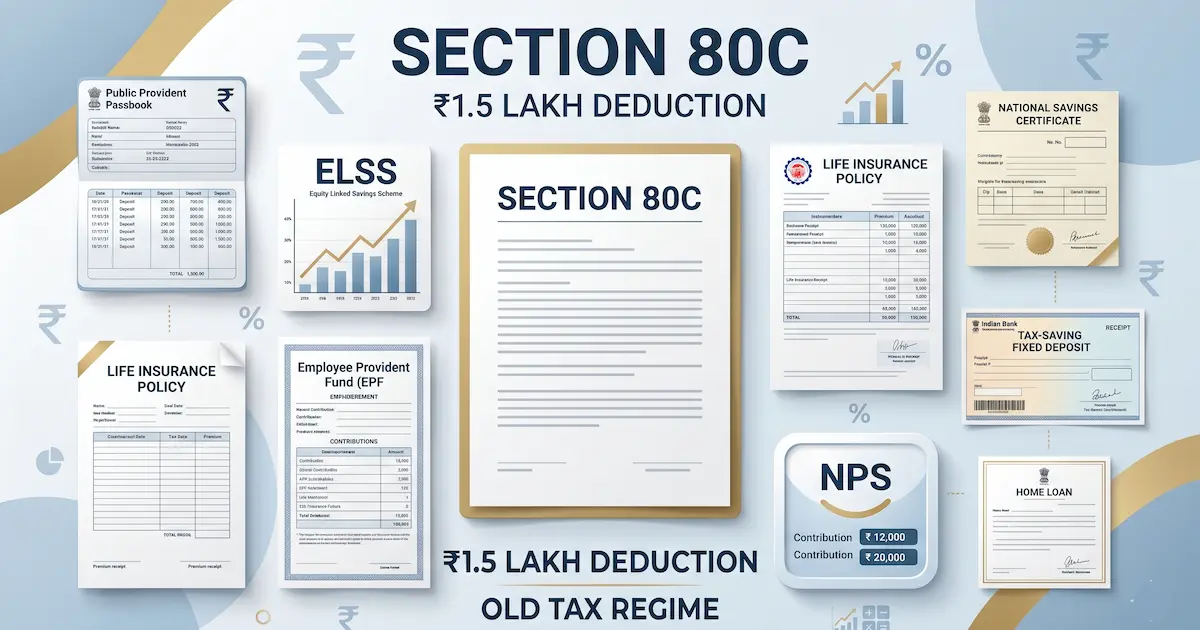

- Section 80C deductions (PPF, ELSS, life insurance, etc.) — see what is Section 80C deduction

- Home loan interest deduction under Section 24

- LTA (Leave Travel Allowance)

- Most other Chapter VI-A deductions

What the new regime continues to allow:

- Standard deduction (₹75,000)

- Section 80CCD(1B) — additional ₹50,000 deduction for NPS Tier 1 contributions

- Employer contribution to NPS (Section 80CCD(2))

- Family pension deduction

- Agniveer Corpus Fund contribution (Section 80CCH)

The old regime — slabs and structure (unchanged)

The old regime continues as an option for taxpayers who explicitly opt out of the new regime each year by selecting "old regime" on their Form 10-IEA filing.

Old regime slabs (unchanged for FY 2025-26):

| Total income | Tax rate |

|---|---|

| Up to ₹2,50,000 | 0% |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Standard deduction: ₹50,000 under the old regime.

Section 87A rebate: Up to ₹12,500 if total income is up to ₹5 lakh — meaning effective zero tax up to ₹5 lakh.

The old regime keeps the full set of exemptions and deductions that the new regime disallows — HRA, Section 80C up to ₹1.5 lakh, home loan interest, LTA, etc. Mathematically, the old regime produces lower total tax when the cumulative value of allowable exemptions and deductions (large home loan interest, HRA in metro cities, full ₹1.5 lakh 80C, education loan interest) exceeds the new regime's slab-rate savings. Whether this is the case for any specific taxpayer requires individual computation by a Chartered Accountant.

Surcharge and Cess — the layers on top of slab tax

Two additional layers apply to the tax calculated from the slabs themselves:

Surcharge

An additional percentage charged on the tax (not on income) when total income crosses specific thresholds. The new regime surcharge rates for FY 2025-26:

| Total income | Surcharge on tax |

|---|---|

| Up to ₹50 lakh | 0% |

| ₹50 lakh to ₹1 crore | 10% |

| ₹1 crore to ₹2 crore | 15% |

| Above ₹2 crore | 25% |

(Under the old regime, an additional 37% surcharge tier applied above ₹5 crore historically; the new regime capped the top surcharge at 25% from FY 2023-24, which significantly reduced the effective tax burden on very high earners who chose the new regime.)

Health and Education Cess

A flat 4% applied to the slab-calculated tax plus any surcharge. The cess was introduced in 2018 (combining the earlier Education Cess of 2% and Secondary & Higher Education Cess of 1%) and funds health and education programmes administered by the central government via the Ministry of Education and the Ministry of Health and Family Welfare.

The cess applies to all taxpayers regardless of regime choice.

A fully worked example — salary ₹15 lakh under new regime

A salaried employee in Bengaluru earning ₹15 lakh gross annual salary in FY 2025-26. No special exemptions, no home loan, no NPS contribution. Filing under the new regime (default).

Step 1: Calculate total income

- Gross salary: ₹15,00,000

- Less: Standard deduction: −₹75,000

- Total income: ₹14,25,000

Step 2: Apply new regime slabs

| Band | Income in band | Rate | Tax |

|---|---|---|---|

| Up to ₹4,00,000 | ₹4,00,000 | 0% | ₹0 |

| ₹4–8 lakh | ₹4,00,000 | 5% | ₹20,000 |

| ₹8–12 lakh | ₹4,00,000 | 10% | ₹40,000 |

| ₹12–14.25 lakh | ₹2,25,000 | 15% | ₹33,750 |

| Total slab tax | ₹93,750 |

Step 3: Section 87A rebate

Total income ₹14,25,000 is above the ₹12 lakh threshold for full 87A rebate under the new regime. Marginal relief applies but the full rebate doesn't — the taxpayer pays the slab-calculated tax.

Step 4: Add Health and Education Cess

Cess = 4% of ₹93,750 = ₹3,750

Step 5: Total tax payable

₹93,750 + ₹3,750 = ₹97,500

Effective tax rate = ₹97,500 ÷ ₹15,00,000 = 6.5%

Note the gap between marginal rate (15% — the rate on the last rupee earned) and effective rate (6.5% — total tax ÷ total income). This gap is structural to all progressive tax systems and is explored in detail in marginal vs effective tax rate explained.

This worked example uses round numbers for clarity. Actual salary structures include components like HRA, special allowances, performance bonuses, and statutory deductions (EPF, professional tax) that affect both gross salary and the relevant tax computation. The exact tax liability for your specific salary structure depends on details a Chartered Accountant familiar with your situation can correctly assess.

For how these slabs feed a complete salaried return — Form 16, deductions, capital gains, and filing — see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

What this post does not cover

Deliberately out of scope for this explainer:

- Which regime to choose — that is a planning decision dependent on individual exemption/deduction claims and falls under tax planning, which is the domain of a Chartered Accountant who knows your full income profile

- How to file your ITR — filing mechanics are covered by the Income Tax Department's own e-filing portal and by CA-led tutorials

- Capital gains tax computation — capital gains follow a separate tax structure with different slab rates depending on holding period and asset class. See what is capital gains tax — short vs long term once it ships

- Tax-saving investment strategies — this is investment planning + tax planning combined, requiring personalised analysis

The structural takeaway from this post: India's tax slabs are progressive, two parallel regimes exist as of FY 2025-26, the new regime offers effective zero tax up to ₹12 lakh after the standard deduction and 87A rebate, and the slab-calculated tax is then increased by surcharge (if applicable) and the 4% Health and Education Cess. Understanding this much is the foundation; the application to your specific situation requires a qualified professional.

Frequently asked questions

What is an income tax slab in India in simple terms? An income tax slab is a band of annual income that is taxed at a specific percentage rate. India uses a progressive tax structure — the first band of income is taxed at a lower rate (or zero), and each higher band is taxed at a progressively higher rate. So a person earning ₹15 lakh annually doesn't pay 20% on the entire ₹15 lakh; they pay 0% on the first slab, 5% on the next, and so on up to whatever final slab their income reaches. The slab structure is notified by the Ministry of Finance through the annual Union Budget and published by the Income Tax Department. Two parallel slab structures currently exist: the new regime (default since FY 2023-24) and the old regime (continues for taxpayers who explicitly opt in).

What is the difference between the old and new tax regimes? Two different sets of slabs running in parallel since FY 2020-21. The new regime offers lower marginal rates and a more generous Section 87A rebate (effectively zero tax up to ₹12 lakh of total income in FY 2025-26) but disallows most exemptions and deductions including HRA, Section 80C investments, home loan interest under Section 24, and most other Chapter VI-A deductions. The old regime keeps the higher slab rates but allows the full set of exemptions and deductions. Both regimes allow the standard deduction (₹75,000 under new, ₹50,000 under old) and Section 80CCD(1B) NPS deduction of ₹50,000. Taxpayers choose annually which regime to file under. The Income Tax Department defaults to the new regime if no choice is made.

What is the Section 87A rebate and how does the ₹12 lakh zero-tax claim work? Section 87A is a rebate that reduces a taxpayer's calculated tax liability to zero if their total income falls below a specified threshold. Under the new regime for FY 2025-26, the rebate amount is up to ₹60,000, applicable when total income is up to ₹12 lakh — meaning a salaried person earning ₹12 lakh after the ₹75,000 standard deduction owes zero income tax. Income above ₹12 lakh starts attracting tax at the slab rates without the rebate (with a marginal-relief provision that prevents very small income increases above the threshold from creating a large tax jump). Under the old regime, Section 87A provides a smaller rebate (up to ₹12,500) when income is up to ₹5 lakh.

What is the Health and Education Cess and is it the same as the slab rate? The Health and Education Cess is an additional 4% charge applied to the tax calculated from the slabs — not to the income directly. If your slab-calculated tax comes to ₹1 lakh, the 4% cess adds ₹4,000, bringing your total tax to ₹1,04,000. The cess was introduced in 2018 (combining the earlier Education Cess and Secondary & Higher Education Cess) and funds health and education programmes administered by the central government. Surcharge on tax is also additional: 10% on tax for income above ₹50 lakh, 15% above ₹1 crore, 25% above ₹2 crore (new regime), and historically 37% above ₹5 crore (this top surcharge was reduced to 25% under the new regime from FY 2023-24). For high-income taxpayers, surcharge plus cess can add several percentage points to the effective tax burden.

Sources

- Income Tax Department of India, Income Tax Slabs and Rates for FY 2025-26 — incometax.gov.in

- Central Board of Direct Taxes (CBDT) — incometaxindia.gov.in

- Ministry of Finance, Union Budget 2024 and 2025 — Finance Acts and Notifications — indiabudget.gov.in

- Income Tax Department, Section 87A Rebate Provisions — incometax.gov.in/iec/foportal/help/section-87a

- Income Tax Department, Surcharge Rates — Individual Taxpayers — incometax.gov.in

- Tax Information Network (TIN-NSDL), PAN and TDS Statutory Guidance — tin-nsdl.com

You might also like

What are taxes actually used for? A plain-English breakdown of where federal, state, and local tax dollars go, and why understanding this matters for personal finance.

8 min read

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read

HRA exemption is the least of three amounts under Section 10(13A). See the FY 2025-26 formula, a worked example, metro cities, the limit, and the claim rules.

13 min read