Is 30% the Official CIBIL Credit Utilization Rule?

By Tapabrata Biswas · Last updated June 22, 2026 · 8 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

An Indian cardholder with a ₹1,00,000 limit and a ₹30,000 reported balance is sitting at exactly 30% credit utilization, the threshold TransUnion CIBIL flags. Drop that balance to ₹10,000 and utilization falls to 10%, the range tied to the highest CIBIL scores. The same single figure, the credit utilization ratio, is one of four major factors in a CIBIL score and accounts for 30% of a FICO score in the US, which makes it the second most powerful lever in credit scoring after payment history.

This post covers what credit utilization actually measures, why the 30% threshold matters, the difference between per-card and aggregate utilization, when in the billing cycle it gets reported, and how the same mechanic applies under both FICO (US) and CIBIL (India) scoring frameworks.

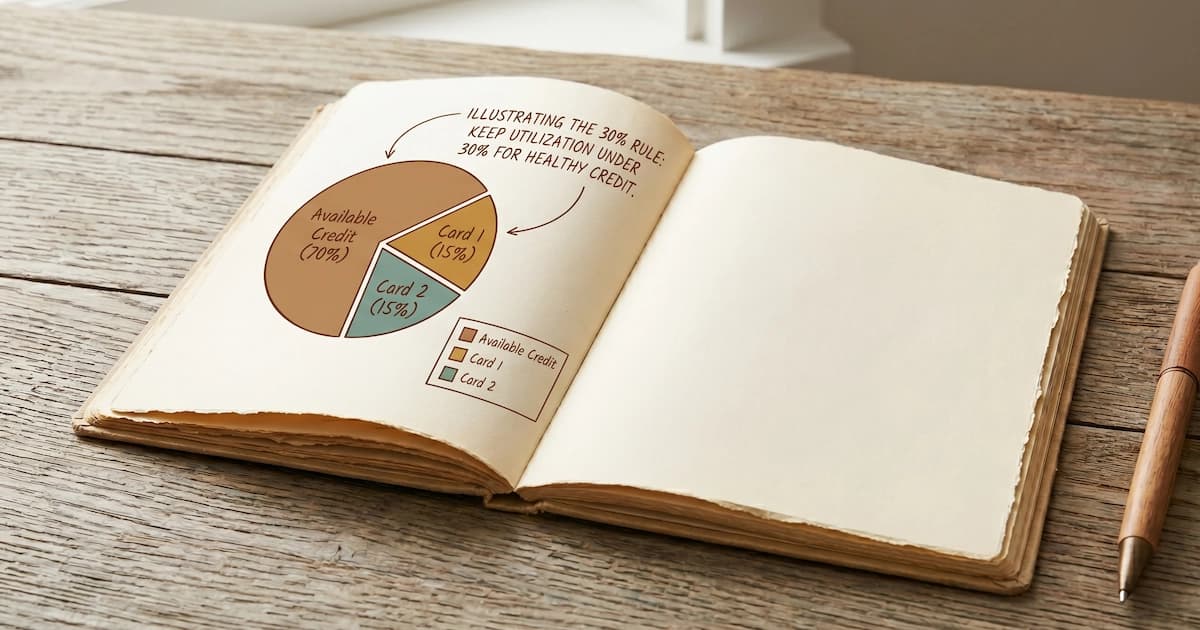

Is 30% the official CIBIL credit utilization rule?

Yes. TransUnion CIBIL's published guidance recommends keeping your credit utilization ratio below 30% of your total available limit. It is a recommended guideline rather than a hard cut-off: CIBIL treats usage above 30% as credit-hungry behaviour that can lower your score, and the highest CIBIL scores typically belong to people who stay well under it. On a ₹1,00,000 credit card limit, that means keeping the reported balance under ₹30,000; drop it to ₹10,000 and you are at 10%, the range usually linked to 750+ CIBIL scores.

| Credit utilization | What CIBIL reads it as |

|---|---|

| Under 10% | Ideal, linked to the highest scores (750+ to 800+) |

| 10% to 30% | Healthy, the widely cited CIBIL guideline |

| 30% to 50% | Warning, read as credit-hungry, score drag begins |

| Above 50% | Damaging, tends to push scores toward the 600s |

The same 30% threshold applies under FICO in the US, where utilization sits inside the "amounts owed" factor. The rest of this guide covers how the ratio is calculated, when it gets reported, and how to lower it, under both CIBIL and FICO.

What credit utilization actually is

Credit utilization is the ratio of credit card balance to credit card limit, expressed as a percentage. The formula is straightforward:

Credit utilization = (Total balance owed ÷ Total credit limit) × 100

A single card example. Card limit: $5,000. Current balance reported to the bureau: $1,500. Utilization: 30%.

The ratio is calculated two ways simultaneously, and both matter to scoring models.

Per-card utilization: each individual card's balance divided by its individual limit. A single card maxed out at $5,000 of a $5,000 limit shows 100% utilization on that card, even if the cardholder's other cards are at zero.

Aggregate utilization: the sum of all card balances divided by the sum of all card limits. A cardholder with three cards at $5,000 / $10,000 / $15,000 limits ($30,000 total) and balances of $1,500 / $0 / $1,500 ($3,000 total) has 10% aggregate utilization.

Both numbers feed into the credit score. A high per-card utilization on even one card can drag the score down, even if aggregate utilization looks healthy. This is why scoring optimisation usually involves spreading balances across cards rather than concentrating them on one.

Why the 30% rule exists

The "30% rule" — keep utilization below 30% — is the most widely cited credit card guideline in personal finance writing. The threshold is not arbitrary. It comes from FICO's published research on score distributions: consumers with utilization above 30% historically show meaningfully higher rates of future delinquency than consumers below 30%, and FICO's scoring algorithms weight the ratio accordingly.

The relationship between utilization and score is not strictly linear. Research from FICO and the Consumer Financial Protection Bureau indicates the score impact at different utilization tiers approximately follows this pattern:

| Utilization | Typical FICO impact |

|---|---|

| 0% (no balance reported) | Slight negative — bureau may interpret as inactive use |

| 1–10% | Optimal — associated with highest scores |

| 10–30% | Healthy — minimal score drag |

| 30–50% | Moderate negative — visible score reduction |

| 50–75% | Significant negative — meaningful score reduction |

| 75–100% | Severe negative — large score reduction |

The exact point gain or loss depends on the starting score (a higher score has more room to fall), the rest of the credit profile, and the scoring model in use. But the directional pattern is consistent across FICO 8, FICO 9, VantageScore 3.0, VantageScore 4.0, CIBIL TransUnion 2.0, and Experian India's models.

A practical implication: the difference between 28% and 32% utilization can produce a noticeable score change, while the difference between 35% and 45% can be smaller in absolute points. The 30% threshold is more of a step than a slope.

How FICO weights credit utilization

FICO publishes the relative weight of each factor in its US scoring model:

| FICO factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | On-time vs late payments across all accounts |

| Amounts owed (utilization) | 30% | Total debt and credit utilization ratio |

| Length of credit history | 15% | Average age of accounts, oldest account |

| Credit mix | 10% | Variety of account types (cards, loans, mortgage) |

| New credit | 10% | Recent applications and newly opened accounts |

Credit utilization sits inside the 30% "Amounts owed" category, alongside total debt balances and the number of accounts with balances. Within that 30%, utilization is the single largest sub-factor — meaning roughly 20–25% of the entire FICO score is driven by the utilization ratio alone.

Utilization is the fastest credit-score lever a consumer has access to — the only FICO factor that can change month to month. Payment history takes years to build. Length of credit history accumulates with time. Credit mix changes only when new account types are opened. Utilization, by contrast, can swing 50 percentage points in a single billing cycle by either swiping or paying down a balance — and the score moves with it. Paying down a high balance ahead of a mortgage or auto loan application often produces measurable score improvement within 30–60 days as the new lower balance gets reported.

How CIBIL weights credit utilization in India

TransUnion CIBIL — the dominant Indian credit bureau — uses a 300–900 score range and groups its scoring factors slightly differently from FICO. CIBIL identifies four major factors in score calculation but does not publish exact percentage weights the way FICO does:

| CIBIL factor | Description |

|---|---|

| Payment history | On-time payments across all credit accounts |

| Credit utilization | Total credit used vs total credit available |

| Credit mix and duration | Mix of secured and unsecured credit, length of history |

| Other factors | Recent inquiries, new accounts, etc. |

While CIBIL doesn't publish weights, industry practice holds that payment history and utilization together drive the largest share of the score — broadly similar to the FICO 35% + 30% pattern, though the exact split varies by model version.

A CIBIL score of 750+ is the widely accepted threshold for "good" credit at most Indian banks. Below 750, loan applications often face higher interest rates or rejection. The same utilization mechanics apply: keeping utilization below 30% supports scores in the 750+ range, while consistently high utilization (above 50%) tends to push scores into the 600s.

The mechanics covered in our credit report explainer cover how Indian bureaus collect and report this data — the four major bureaus (CIBIL, Experian India, Equifax India, CRIF High Mark) all calculate utilization the same way, though their proprietary scoring algorithms produce slightly different scores from the same underlying data.

When utilization gets reported (and why timing matters)

This is the mechanic most cardholders never realise until they see a score change.

Issuers report account information to the credit bureaus once per month, on a fixed reporting date set by each issuer. The balance reported is whatever the balance was on that reporting date — at most issuers, the statement closing date.

A worked example. Card limit: $5,000. Statement closes on the 15th of each month. Payment due on the 10th of the following month. The cardholder swipes $4,000 between the 1st and the 14th, then pays the full $4,000 on the 9th of the next month before the due date.

Despite paying the balance in full and avoiding all interest charges as covered in our piece on how credit card interest works, the credit bureau receives a $4,000 balance reading on the 15th. Utilization for that card reports as 80%. The score impact is the same as if the cardholder had carried that balance.

The fix: pay down the balance before the statement closing date, not just before the payment due date. A small pre-statement payment that brings the reported balance to $1,000 (20% utilization) instead of $4,000 (80%) keeps the score impact minimal while still allowing the cardholder to use the card normally.

This is sometimes called "AZEO" (All Zero Except One) in credit-optimisation circles — the practice of paying all cards to zero before statement close except one card carrying a small balance. The single small balance reports as low utilization (e.g., $50 on a $5,000 limit = 1%), and the rest report at 0%, producing the most favourable possible utilization snapshot at reporting time.

Common mistakes that hurt utilization

Three patterns regularly damage utilization without the cardholder realising why.

Paying after the statement closing date but before the due date. The cardholder pays in full, avoids interest, but the credit report still shows the high pre-payment balance for the entire month until the next reporting cycle. The score effect can persist for 30–60 days even though the balance is technically paid.

Closing unused credit cards to "simplify" finances. Closing a card removes its credit limit from the aggregate denominator. A cardholder with $30,000 total limits and $5,000 balance has 17% utilization. Close a $10,000 card and the same $5,000 balance is now 25% of $20,000. Utilization jumped without any spending change. The Federal Reserve's research on consumer credit consistently notes that closing the oldest cards also damages credit history length, compounding the score impact.

Concentrating all charges on one card to chase rewards. The reward optimisation strategy of putting all spend on a single high-rewards card raises that card's per-card utilization. A cardholder spending ₹40,000/month on a card with a ₹50,000 limit shows 80% per-card utilization at statement time, even with ₹2,00,000 in unused limits across other cards. The aggregate may be fine; the per-card number is not.

What experts say

The FICO consumer credit education materials document the exact weighting of utilization in the FICO model and the research basis for the 30% threshold. It's the canonical US reference for how the ratio interacts with the rest of the score.

The Consumer Financial Protection Bureau's credit score primer covers utilization in the broader context of how scoring models work and includes guidance on the timing of payments versus statement dates.

TransUnion CIBIL's score factors page lists the four major factors that drive Indian credit scores, including utilization. While CIBIL doesn't publish exact weights, the factor ordering signals that payment history and utilization are the dominant drivers.

For broader context on how all the credit reporting systems work, see our credit report explainer and our overview of personal finance basics.

Frequently asked questions

What is the ideal credit utilization ratio? Below 30% is the widely cited threshold, but FICO research indicates that scores above 800 typically belong to consumers with utilization under 10%. The score impact is roughly linear up to about 30%, then steeper above that. A cardholder with $20,000 in total limits should aim to keep reported balances below $6,000 (30%), and below $2,000 (10%) to maximize score. The threshold applies to both per-card and aggregate utilization.

Does paying off the balance every month help my utilization ratio? It helps total interest cost (you avoid all interest charges by paying in full), but the utilization ratio reported to bureaus depends on the balance at the statement closing date, not on whether the balance is later paid. A card with a $10,000 limit that's swiped to $7,000 mid-cycle and paid in full at the due date can still report 70% utilization if the statement closes before the payment posts. Paying down before the statement closes is what lowers reported utilization.

How does CIBIL calculate utilization compared to FICO? Both calculate the same ratio (balance ÷ credit limit), and both weight it heavily, though the weighting is published publicly only for FICO (30% of the score). CIBIL groups utilization under 'Credit Utilization' as one of four major factors alongside payment history, credit mix/duration, and other factors. CIBIL scores range 300–900 while FICO ranges 300–850, but the underlying mechanics are identical: lower is better, the 30% threshold is widely cited, and reporting timing matters.

Is 30% the official CIBIL recommendation for credit utilization? TransUnion CIBIL's published consumer guidance recommends keeping your Credit Utilisation Ratio (CUR) below 30% — using more than 30% of your available credit limit is treated as a sign of credit-hungry behaviour and can lower your CIBIL score. Utilisation is one of the key factors in the 300–900 CIBIL score, alongside payment history, credit mix, and recent credit-seeking activity. The 30% figure is a widely published guideline rather than a hard cut-off: lower is consistently better, and the highest-scoring consumers typically stay well under 30%. Confirm the current wording on cibil.com, since TransUnion CIBIL updates its educational guidance periodically.

Should I close unused credit cards to manage my credit? In most cases no, because closing a card removes its credit limit from the aggregate calculation, raising the overall utilization ratio. A cardholder with $30,000 in total limits and a $5,000 balance has 17% utilization. Close a card with a $10,000 limit and the same $5,000 balance is now 25% of the remaining $20,000 — utilization jumped without any spending change. Keep low-fee unused cards open and use them occasionally to keep the account active.

In summary

Credit utilization — the ratio of credit card balance to credit limit — is one of the two largest factors in both FICO and CIBIL scoring models, behind only payment history. The 30% threshold is widely cited because of FICO research linking utilization above that level to higher delinquency rates. The mechanic is the same in India and the US: lower is better, both per-card and aggregate matter, and the balance reported to bureaus depends on what the card showed at statement closing, not on whether it's later paid in full. Closing unused cards usually hurts more than it helps because it removes credit limit from the aggregate calculation.

The next read in this series is on debt snowball vs avalanche — the two main strategies for paying down balances when utilization is high across multiple cards. For deeper context on what's accruing on those balances, see how credit card interest works.

Sources

- FICO, How FICO Scores Work — Credit Score Factors — myfico.com/credit-education/credit-scores

- Consumer Financial Protection Bureau, What is a credit score? — consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315

- TransUnion CIBIL, CIBIL Score Factors and Calculation — cibil.com/freecibilscore

- Federal Reserve, Report on the Economic Well-Being of U.S. Households — federalreserve.gov/consumerscommunities/shed.htm

Most read

You might also like

What is a credit report? A plain-English explanation of what's on it, where it comes from, who can see it, and how it differs from a credit score.

8 min read

How does credit card interest work? A plain-English breakdown of daily compounding, the average daily balance method, grace periods, and the minimum payment trap, with India and US numbers.

9 min read

Personal finance basics explained in plain English: income, saving, debt, credit, and investing — the small set of concepts every adult tends to encounter.

8 min read