Marginal vs Effective Tax Rate Explained: Why You're Not Actually 'In the 30% Bracket' on Every Rupee

By Tapabrata Biswas · Published May 25, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of marginal vs effective tax rates, applicable to any progressive tax system. This post is not tax planning advice. The specific rates that apply to your situation depend on your income level, regime choice (in India), deduction profile, filing status (in the US), and several other variables that only a qualified Chartered Accountant (India) or Certified Public Accountant (US) familiar with your situation can correctly assess. Consult the appropriate professional for any decision that turns on your exact marginal or effective rate.

The terms "marginal tax rate" and "effective tax rate" sit at the heart of a misconception that costs Indian and US taxpayers measurable amounts of money every year — the belief that being "in the 30% bracket" means paying 30% on all income. The misconception leads people to refuse promotions, decline freelance work, and undersize their retirement contributions because they assume tax will eat the additional income. Progressive tax systems don't work that way. Each slab is taxed at its own rate, and only the portion of income falling in the top slab gets the top rate.

This post covers what each rate actually is, how they differ structurally in progressive tax systems, worked examples for India (new regime) and the US (federal), why each rate matters for different decisions, and the common bracket misconception that gets in the way of straightforward income decisions.

What the marginal tax rate actually is

The marginal tax rate is the percentage applied to your next rupee or dollar of income — the rate on the last band of income you've earned within a progressive tax structure.

In a progressive system, income is divided into bands (slabs in India, brackets in the US), and each band is taxed at a different percentage. Your marginal rate is the rate on the highest band your income actually reaches.

A salaried Indian earning ₹14,25,000 taxable income under the new regime (FY 2025-26) reaches the ₹12-16 lakh slab. That slab is taxed at 15%. Their marginal rate is 15% — meaning the next ₹1 they earn gets taxed at 15% (plus the 4% Health and Education Cess).

The marginal rate is the relevant number when evaluating:

- A salary raise or promotion (additional income at the top end)

- A bonus or one-time payment

- Freelance side income added to a primary salary

- Whether to convert salary to a different income category

- Tax savings from a marginal-rate deduction (a ₹1.5 lakh Section 80C deduction at 15% marginal saves 15% × ₹1.5L = ₹22,500 in tax, not 22.5% × ₹1.5L)

For the underlying slab structure these marginal rates come from, see income tax slab India explained.

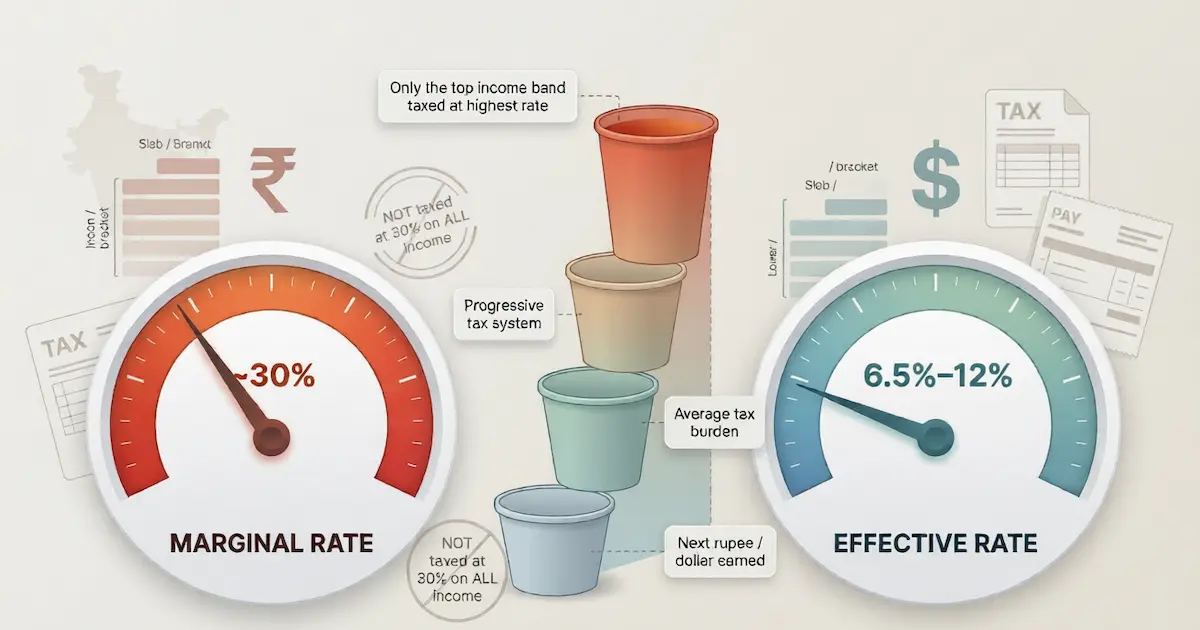

What the effective tax rate actually is

The effective tax rate is your total tax paid divided by your total income — the "average" rate that reflects what fraction of your total income actually went to tax across all slabs combined.

Using the same Indian salaried example: total tax of ₹97,500 (per the worked example in the slab post) divided by ₹15,00,000 gross income = 6.5% effective rate. This person's marginal rate is 15%, but their effective rate is 6.5% — less than half the marginal rate.

The structural reason for the gap: progressive systems tax lower bands at lower rates. The first ₹4 lakh gets 0%, the next ₹4 lakh gets 5%, and so on. Only the very top portion of income reaches the marginal-rate band. When you average across all bands, the result is always lower than the top rate.

The effective rate is the relevant number when:

- Calculating your actual post-tax disposable income (for budgeting, savings-rate planning)

- Comparing your tax burden to other households or other tax years

- Computing your retirement-savings rate as a fraction of total income after tax

- Understanding what "tax burden" actually means for your household

Critical: the effective rate is wrong for evaluating new income. A ₹2 lakh raise doesn't get taxed at your current 6.5% effective rate — it gets taxed at your marginal 15% (plus cess), because it's entirely at the top of your existing income. People who confuse the two rates underestimate the tax cost of additional income.

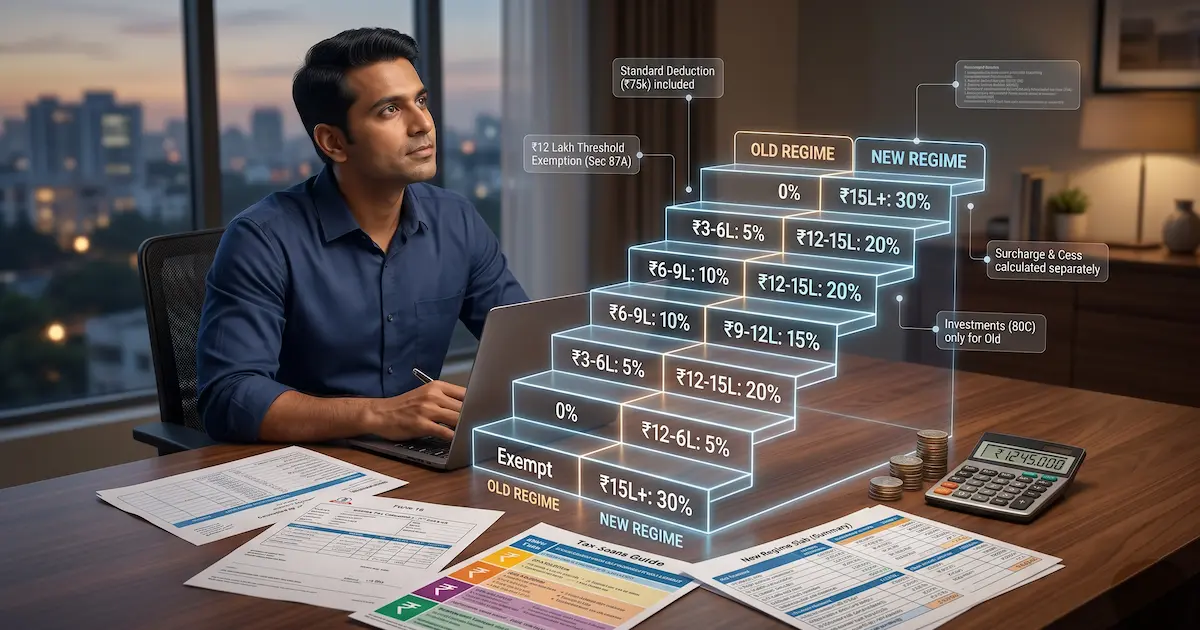

Worked example — Indian salaried employee, FY 2025-26 new regime

Recapping the example from the slab post with the marginal-vs-effective angle:

A salaried employee in Mumbai earning ₹15 lakh gross salary. New regime, only the standard deduction (₹75,000).

| Step | Computation | Amount |

|---|---|---|

| Gross salary | ₹15,00,000 | |

| Less: Standard deduction | −₹75,000 | |

| Taxable income | ₹14,25,000 |

Slab-by-slab tax computation:

| Income band | Income in band | Rate | Tax in band |

|---|---|---|---|

| 0 – ₹4L | ₹4,00,000 | 0% | ₹0 |

| ₹4-8L | ₹4,00,000 | 5% | ₹20,000 |

| ₹8-12L | ₹4,00,000 | 10% | ₹40,000 |

| ₹12-14.25L | ₹2,25,000 | 15% | ₹33,750 |

| Total slab tax | ₹93,750 | ||

| + 4% Cess | ₹3,750 | ||

| Total tax payable | ₹97,500 |

Marginal rate: 15% (the rate on the ₹12-14.25 lakh band — the top band this income reaches) Effective rate: ₹97,500 / ₹15,00,000 = 6.5%

The 8.5 percentage-point gap between marginal and effective is structural. The first ₹4 lakh contributed zero tax; the ₹4-8 lakh band contributed only ₹20K; the heavy lifting happened only in the upper bands.

Worked example — US single filer, Tax Year 2025

A US single filer earning $90,000 gross income. Standard deduction of $15,750 (TY 2025 figure). No itemized deductions.

| Step | Computation | Amount |

|---|---|---|

| Gross income | $90,000 | |

| Less: Standard deduction | −$15,750 | |

| Taxable income | $74,250 |

US federal tax brackets for single filer, TY 2025 (approximate, based on annual inflation adjustments):

| Income band | Income in band | Rate | Tax in band |

|---|---|---|---|

| $0 – $11,925 | $11,925 | 10% | $1,193 |

| $11,925 – $48,475 | $36,550 | 12% | $4,386 |

| $48,475 – $103,350 | $25,775 | 22% | $5,671 |

| Total federal tax | $11,250 |

Marginal rate: 22% federally (plus state — varies) Effective rate: $11,250 / $90,000 = 12.5% (federal only)

The same structural pattern: 22% on the top band, but only 12.5% on average across all income. State tax adds further complexity — California adds roughly 9.3% marginal at this income, Texas/Florida add 0%. For US employees, the $90,000 gross figure originates from Box 1 of the annual W-2 form — that's the number that flows directly into the tax computation above.

The "tax bracket" misconception

The most common misunderstanding of progressive tax systems is believing that being "in" a bracket means paying that rate on all income.

The misconception in practice:

"If I take this ₹2 lakh raise, I'll cross into the 30% bracket and lose 30% of my entire ₹20 lakh salary to tax."

This is wrong. In a progressive system:

- Crossing into the 30% bracket means only the income above the bracket threshold is taxed at 30%

- The lower bands continue to be taxed at their lower rates (0%, 5%, 10%, 15%, 20%, 25%)

- Your effective rate increases slightly (because the new income is at a higher rate), but never approaches your marginal rate

The same misconception appears in the US around the 22%, 24%, or 32% federal brackets. People decline overtime work, refuse promotions, or strategically reduce income to "stay below the bracket" — based on the false belief that crossing a bracket retroactively re-taxes their entire income at the higher rate.

The reality: a ₹2 lakh raise that pushes you from 15% marginal to 20% marginal only increases the tax on the portion of income that crossed the threshold. The pre-raise income continues to be taxed at the lower rates.

A simple way to internalise this: think of slabs as buckets that fill from bottom to top. The first bucket (lowest band) fills first at the lowest rate. Income overflows into the next bucket. Only when the lower buckets are full does income reach the higher-rate buckets. Adding income only adds to the topmost bucket you've reached — it doesn't change the rate at which the lower buckets were filled.

When marginal matters and when effective matters

The two rates answer different questions:

| Question | Use which rate? | Why |

|---|---|---|

| Should I accept this raise / bonus / overtime? | Marginal | The new income is entirely at the top |

| What's my total tax burden? | Effective | Averages across all slabs |

| How much will a ₹1.5L Section 80C deduction save me? | Marginal | Deduction subtracts from the top |

| What's my real take-home as a fraction of gross? | Effective | Total tax / total income |

| Is taking on freelance side income worth it? | Marginal | Side income stacks on top |

| What savings rate should I plan to? | Effective | Budget planning is on total income |

| Should I do a Roth vs Traditional 401(k) (US)? | Marginal (current) vs Marginal (expected retirement) | Both decisions concern the top of income |

| Comparing tax burden across countries / years | Effective | Apples-to-apples comparison |

The confusion most often appears in two places:

- Salary negotiation: people calculate post-tax take-home from a raise using their effective rate, which overstates take-home. Use marginal.

- Budget planning: people calculate total tax from their marginal rate, which overstates total tax. Use effective.

A note on "all-in" marginal rates

In both countries, your "all-in" marginal rate on an additional rupee/dollar of income often exceeds the slab/bracket rate because of additional layers:

India: marginal rate + 4% Health and Education Cess (cess applies to the tax, not income, so effectively multiplies marginal by 1.04). High earners also face surcharge (10/15/25%). So a 30% slab earner in the ₹20L-1cr band pays a marginal of roughly 30% × 1.04 = 31.2% on the next rupee.

US: marginal federal rate + state marginal rate + FICA (7.65% on wages up to the Social Security wage base) + Medicare additional 0.9% on income above $200K + 3.8% NIIT on investment income above income thresholds. A typical California earner in the 24% federal bracket faces an all-in marginal rate closer to 40-45% on additional wages once everything is layered. See what is FICA tax once it ships for the US payroll-tax mechanics.

The exact all-in marginal rate for your specific situation depends on multiple variables that warrant CA/CPA computation.

To see these rates applied across a full salaried return for FY 2025-26, see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

What this post deliberately does not cover

Three out-of-scope topics:

1. "How do I lower my marginal rate?" — Strategies to manage marginal rate (income smoothing, deferred compensation, Roth conversions in US, regime choice in India) are tax-planning decisions specific to each situation. Consult a CA/CPA.

2. "Which deductions give the biggest marginal-rate benefit?" — Deduction selection within available eligible options is investment planning combined with tax planning, requiring personalised input.

3. "Should I avoid the next bracket?" — Specific income-management strategies depend on individual circumstances, available tools (NPS, deferred bonuses, retirement contributions), and personal financial goals.

The structural takeaway: in any progressive tax system, marginal and effective rates are different things and the difference matters. Marginal is the rate on additional income; effective is the rate on average income. The two are always different (effective is always lower) because lower slabs get lower rates. Understanding which one to use for which decision avoids both the bracket-misconception trap and the opposite mistake of underestimating tax on additional income.

Frequently asked questions

What is a marginal tax rate in simple terms? The marginal tax rate is the percentage applied to your next rupee or dollar of income — the rate on the last band of income you've earned. In a progressive tax system (like India's and the US's), income is divided into bands and each band gets a different rate. The highest band your income reaches is your marginal rate. For example, a salaried Indian earning ₹14,25,000 taxable income under the new regime reaches the ₹12-16 lakh slab, which is taxed at 15% — so their marginal rate is 15%, meaning the very next ₹1 they earn gets taxed at 15% (plus cess). The marginal rate matters for decisions about additional income: a raise, a bonus, freelance side income, or whether to take on extra work. It is the rate at which any new income above your current level will be taxed.

What is an effective tax rate and how is it different? The effective tax rate is your total tax paid divided by your total income — the 'average' rate across all your income, not just the marginal band. In progressive tax systems, the effective rate is always lower than the marginal rate (often dramatically so) because the lower slabs are taxed at lower rates. The Indian salaried example earning ₹14,25,000 with ₹97,500 tax (per our worked example in the income tax slab post) has an effective rate of 6.5% even though their marginal rate is 15%. The effective rate matters for budgeting and planning — it tells you what portion of your total income you actually keep after tax, which is the relevant number for retirement-savings rate calculations, household budget planning, and similar long-horizon decisions. The marginal rate is wrong for these purposes because it overstates the actual tax burden on average income.

What is the common 'tax bracket' misconception? The most common tax misconception is believing that 'being in the 30% bracket' means paying 30% on all your income. A person says 'I'm in the 30% bracket so my ₹20 lakh salary loses ₹6 lakh to tax' — that's wrong. Their actual tax is much lower because only the portion of income above the bracket threshold gets the 30% rate. The lower bands get 0%, 5%, 10%, 15%, 20%, 25% respectively. The same misconception appears in the US around the 22% or 24% federal bracket. The result of this misconception: people sometimes refuse promotions or extra work assuming the extra income will be 'eaten' by tax, when in reality the marginal rate on the extra income is the only rate that applies to it — and the rest of their income keeps its existing lower-band rates. Understanding marginal vs effective is the antidote to this misconception.

Should I look at marginal or effective rate when evaluating a raise or bonus? Marginal rate. A raise or bonus is additional income on top of your existing salary, so it falls in your current top slab (or pushes you slightly into the next slab if the raise is large enough to cross a threshold). The relevant question for 'how much of this raise do I actually keep' is: 'what percentage will be taken by tax at my marginal rate?' If you're at 15% marginal (₹12-16L Indian new regime), a ₹2 lakh raise gets taxed at 15% (plus cess) — meaning you keep roughly ₹1.7 lakh. The effective rate would understate the tax bite because the raise is entirely at the top end. Conversely, for evaluating your total tax burden as a percentage of total income (for budget planning, savings-rate calculations), effective rate is the right number — because it averages across all your income. Both numbers are correct for their respective uses; the mistake is using one when you should use the other.

Sources

- Income Tax Department of India, Income Tax Slabs and Rate Computation — incometax.gov.in

- Central Board of Direct Taxes (CBDT), Tax Computation Procedures — incometaxindia.gov.in

- Ministry of Finance, Union Budget 2025 — Finance Act Provisions — indiabudget.gov.in

- US Internal Revenue Service, Tax Brackets and Rates for Individuals — irs.gov

- US Internal Revenue Service, How Your Income Tax Is Calculated — irs.gov/individuals

- Tax Policy Center, How Do Federal Income Tax Rates Work? — taxpolicycenter.org

- Congressional Budget Office, The Distribution of Household Income — cbo.gov

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read

What is capital gains tax? The tax on profit from selling a capital asset, with rates depending on how long you held it. Covers India's post-Budget-2024 rates (12.5% LTCG on equity above ₹1.25L, 20% STCG on equity, 12.5% LTCG on all other assets without indexation, 12-month / 24-month holding periods) and the US structure (0/15/20% long-term rates by income, ordinary slab rates on short-term). Includes worked examples in both countries.

10 min read