Pillar 11

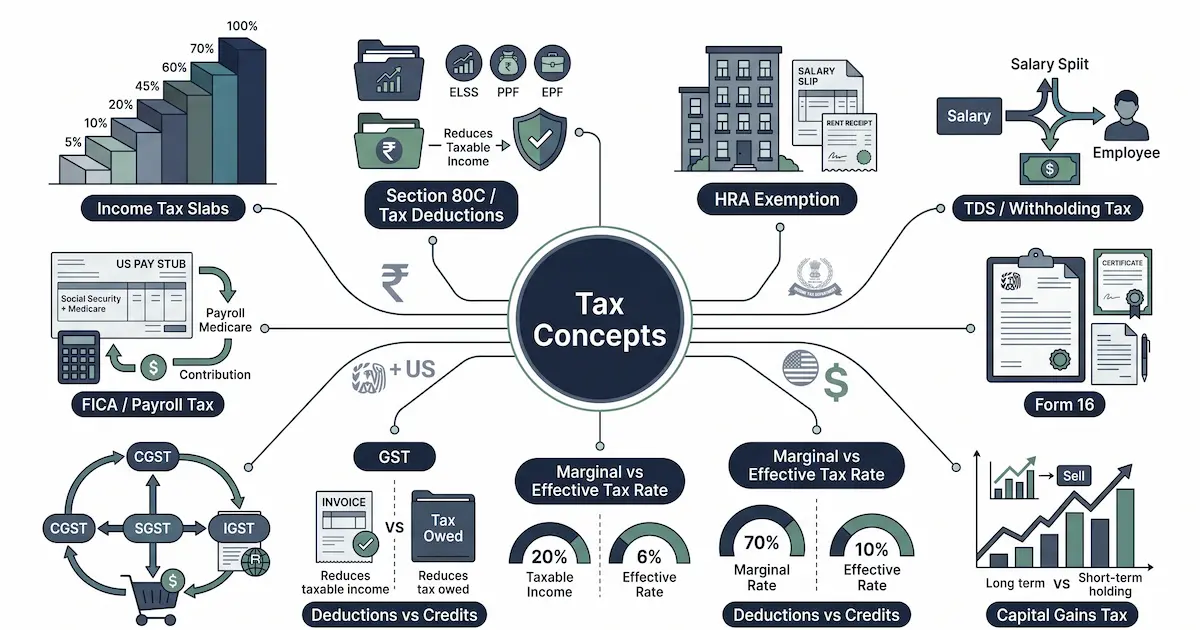

Tax Concepts

Taxes are confusing because the language is technical and the rules change yearly. This section explains the underlying concepts: what tax slabs are, what deductions and credits do, what capital gains tax is, what HRA exemption means in India, what FICA tax funds in the US. These are definitional explainers, not filing advice. For your specific tax situation, consult a qualified Chartered Accountant in India or a Certified Public Accountant in the US.

12 articles

Complete India income tax guide for salaried employees for FY 2025-26 (AY 2026-27), new vs old regime, Form 16, HRA, 80C, capital gains, ITR-1 vs ITR-2, step-by-step filing, common mistakes, and when to consult a CA.

26 min read

What is GST in India? The Goods and Services Tax, a comprehensive destination-based indirect tax introduced on 1 July 2017 that subsumed 17 earlier central and state-level taxes. Covers the 5-slab rate structure (0%, 5%, 12%, 18%, 28% + cess), the CGST/SGST/IGST split between centre and state, Input Tax Credit, the GST Council, registration thresholds (₹40L for goods, ₹20L for services in most states), and the composition scheme for small businesses. For your specific business or filing situation, consult a Chartered Accountant or GST practitioner.

9 min read

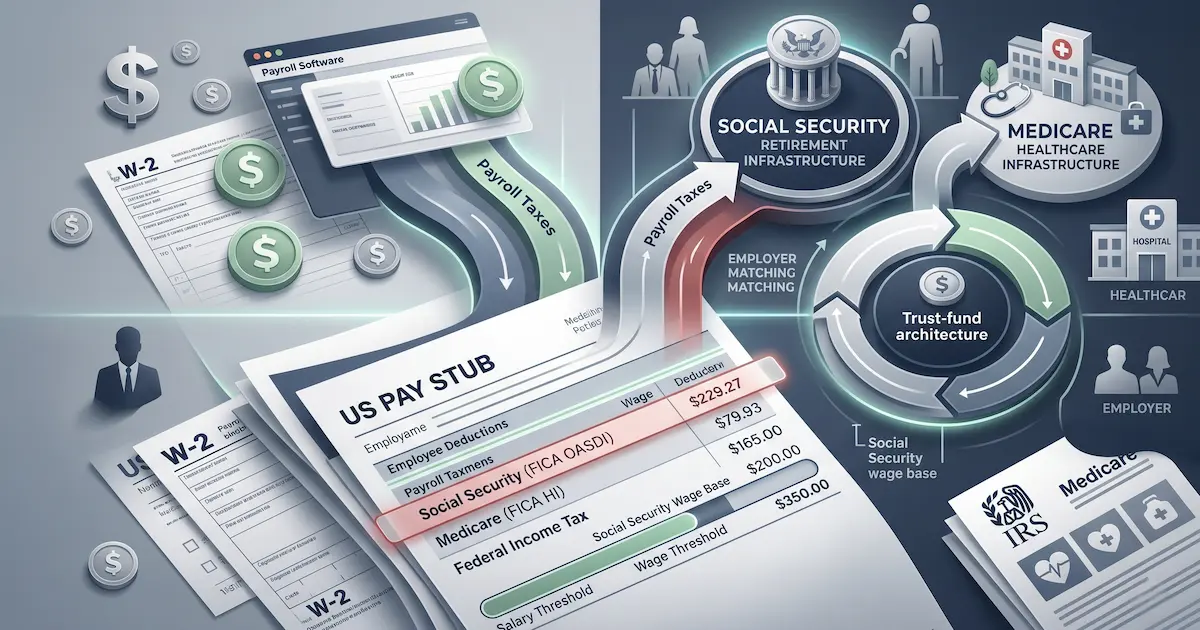

What is FICA tax in the US? The Federal Insurance Contributions Act payroll tax funding Social Security (6.2% on wages up to the wage base) and Medicare (1.45% on all wages, plus 0.9% Additional Medicare above income thresholds). Covers the 2025 wage base of $176,100, employer match doubling the total burden to 15.3% up to the wage base, self-employed treatment under SECA (Schedule SE), and brief comparison to India's EPF + ESIC payroll-based social security.

9 min read

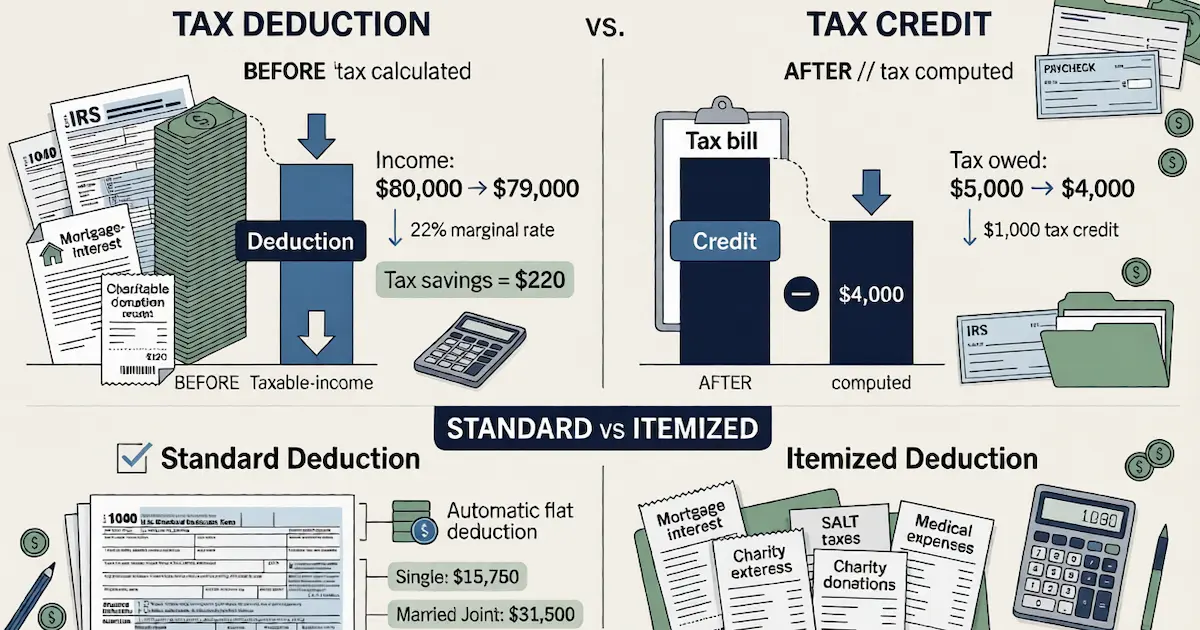

What is the difference between a tax deduction and a tax credit, and between standard and itemized deduction? Tax deductions reduce taxable income (worth your marginal rate × deduction amount); tax credits reduce tax owed dollar-for-dollar. Standard deduction is the flat IRS-fixed amount ($15,750 single / $31,500 married joint for TY 2025); itemized deduction sums specific expenses (SALT cap $10K, mortgage interest, charitable contributions, medical above 7.5% AGI). Covers the math, the structural distinction, and when each makes sense, for educational understanding, not filing advice.

10 min read

What are the foundational tax concepts every Indian and US taxpayer should understand? This pillar page synthesizes 10 definitional explainers covering income tax slabs (India new + old regime), Section 80C, HRA exemption, TDS, Form 16, capital gains, marginal vs effective tax rates, deductions vs credits, standard vs itemized deduction, GST, and FICA. Research-led definitions, not tax planning advice. For your specific situation, consult a Chartered Accountant (India) or Certified Public Accountant (US).

12 min read

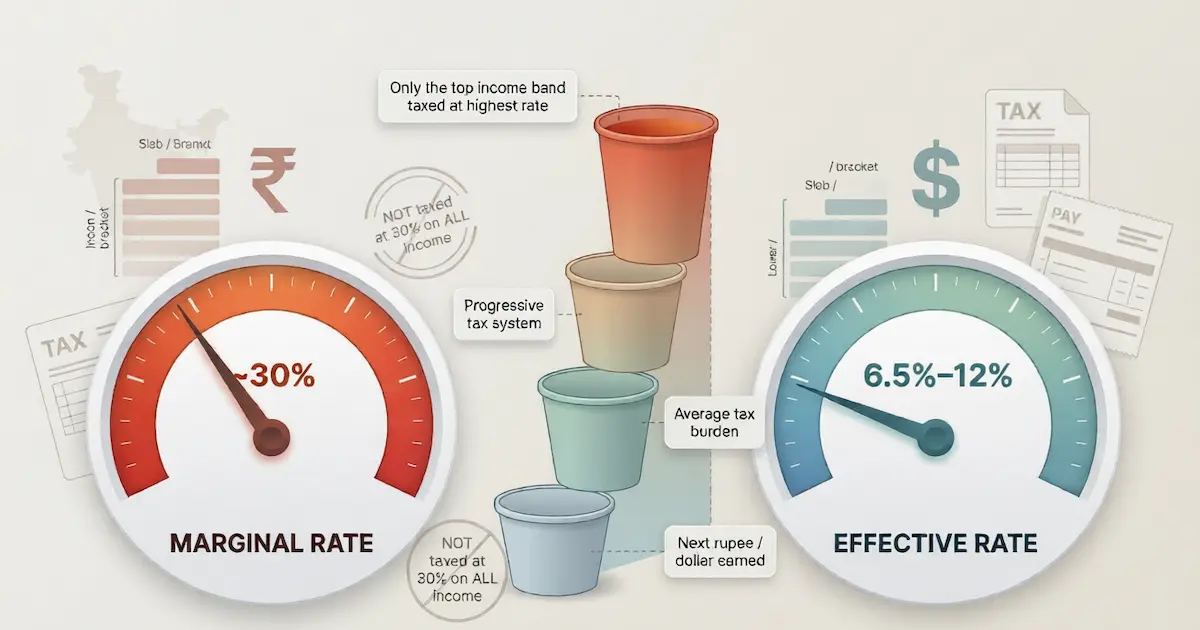

What is the marginal tax rate vs the effective tax rate? Two related but distinct concepts in progressive tax systems. Marginal rate is the percentage applied to your next rupee or dollar of income; effective rate is total tax divided by total income. Covers worked examples for India (new regime ₹15L salary at 15% marginal / 6.5% effective) and the US (federal marginal 22% / effective ~12-14% typical), the most common bracket misconception, and why each rate matters for different decisions.

9 min read

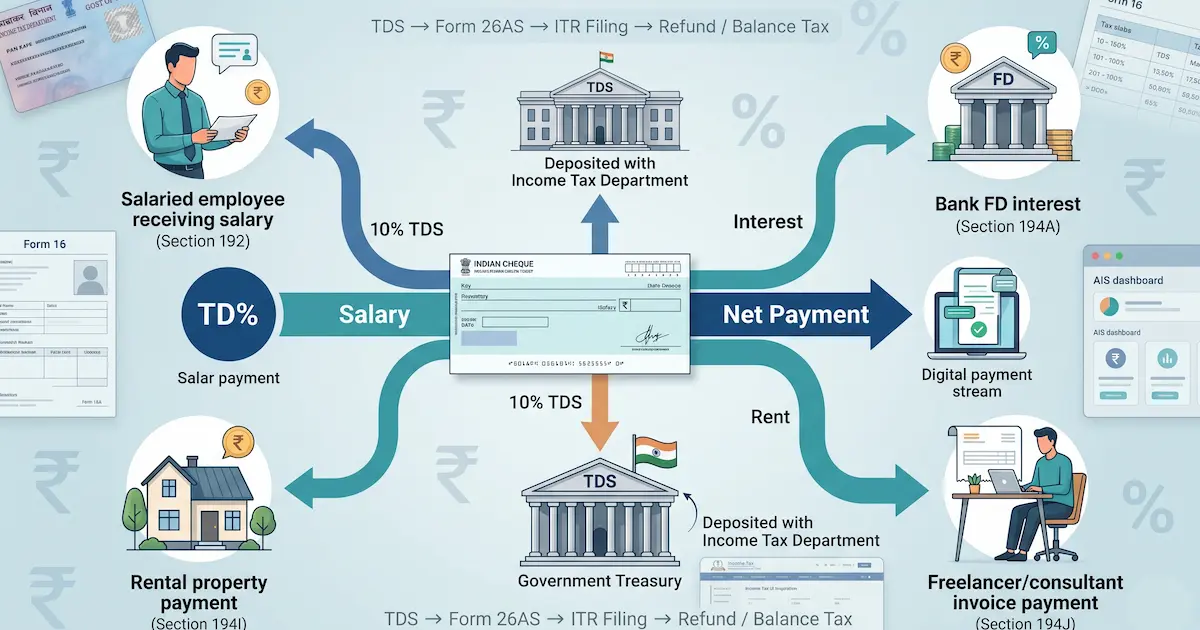

What is TDS? Tax Deducted at Source, the mechanism where the payer of certain income deducts tax before paying the recipient and deposits it with the government. Covers Section 192 (salary), 194A (interest), 194I (rent), 194J (professional fees), 194C (contractor payments), 194 (dividends), the PAN requirement under Section 206AA, current FY 2025-26 thresholds, and how TDS reconciles against ITR liability via Form 26AS.

9 min read

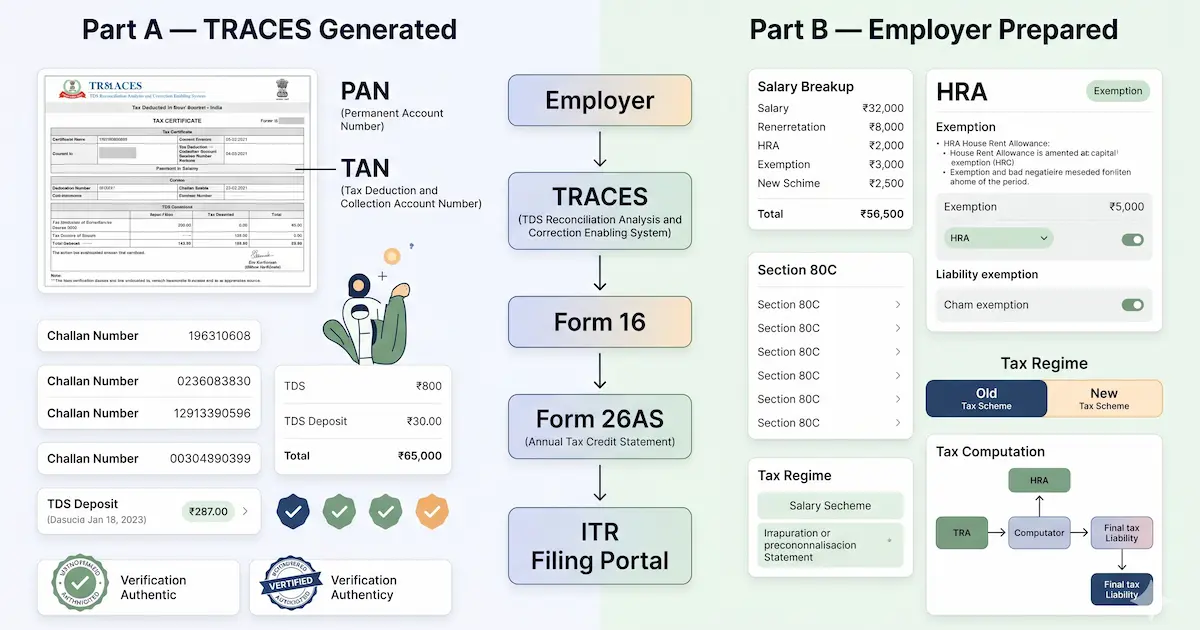

What is Form 16? The TDS certificate Indian employers issue to salaried employees under Section 203 of the Income Tax Act, documenting tax deducted from salary across the financial year. Covers Part A (TRACES-generated, TDS quarter-by-quarter) vs Part B (employer-prepared, salary and deduction breakup), the June 15 issuance deadline, Form 16A for non-salary TDS, how to reconcile Form 16 against Form 26AS, and what to do about mismatches.

9 min read

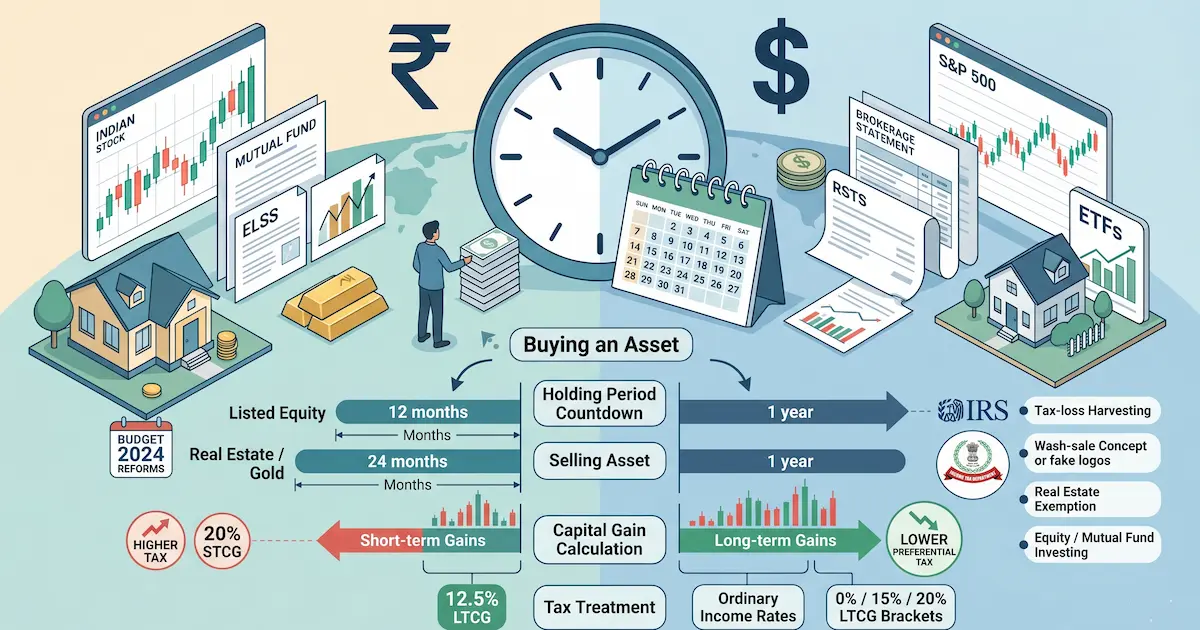

What is capital gains tax? The tax on profit from selling a capital asset, with rates depending on how long you held it. Covers India's post-Budget-2024 rates (12.5% LTCG on equity above ₹1.25L, 20% STCG on equity, 12.5% LTCG on all other assets without indexation, 12-month / 24-month holding periods) and the US structure (0/15/20% long-term rates by income, ordinary slab rates on short-term). Includes worked examples in both countries.

10 min read

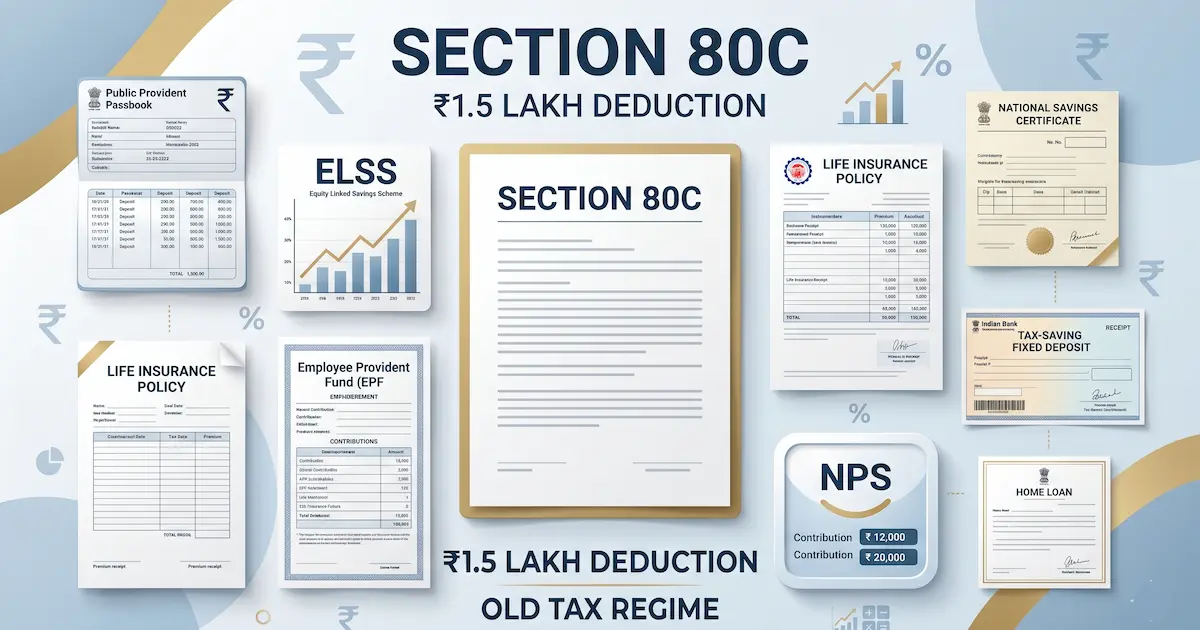

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read

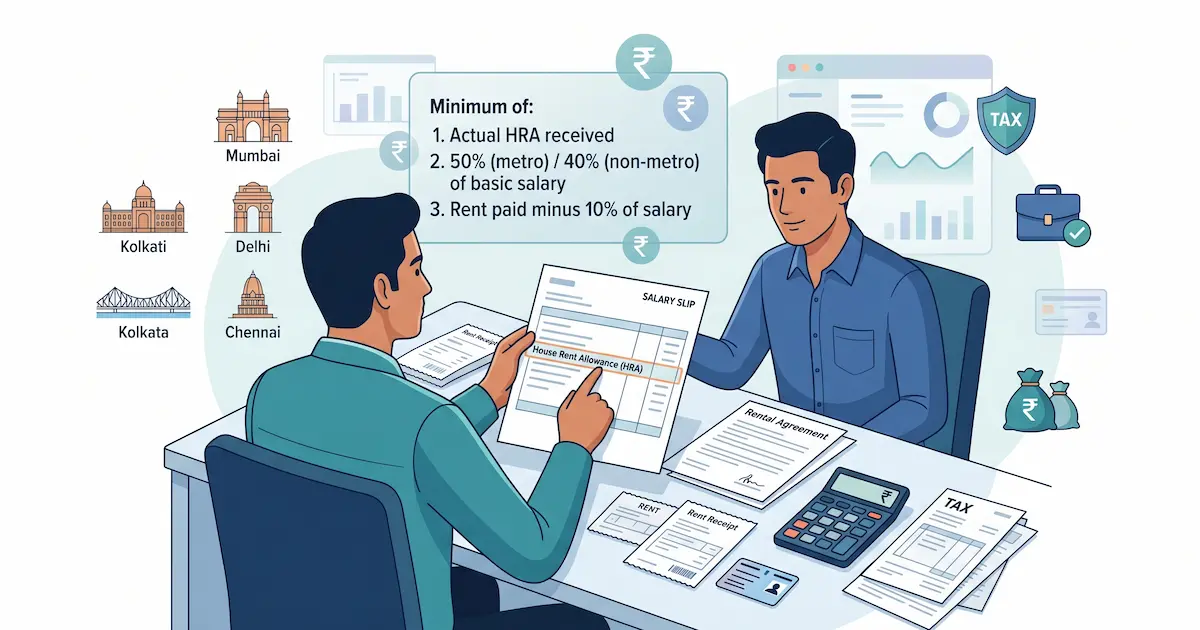

HRA exemption is the least of three amounts under Section 10(13A). See the FY 2025-26 formula, a worked example, metro cities, the limit, and the claim rules.

13 min read

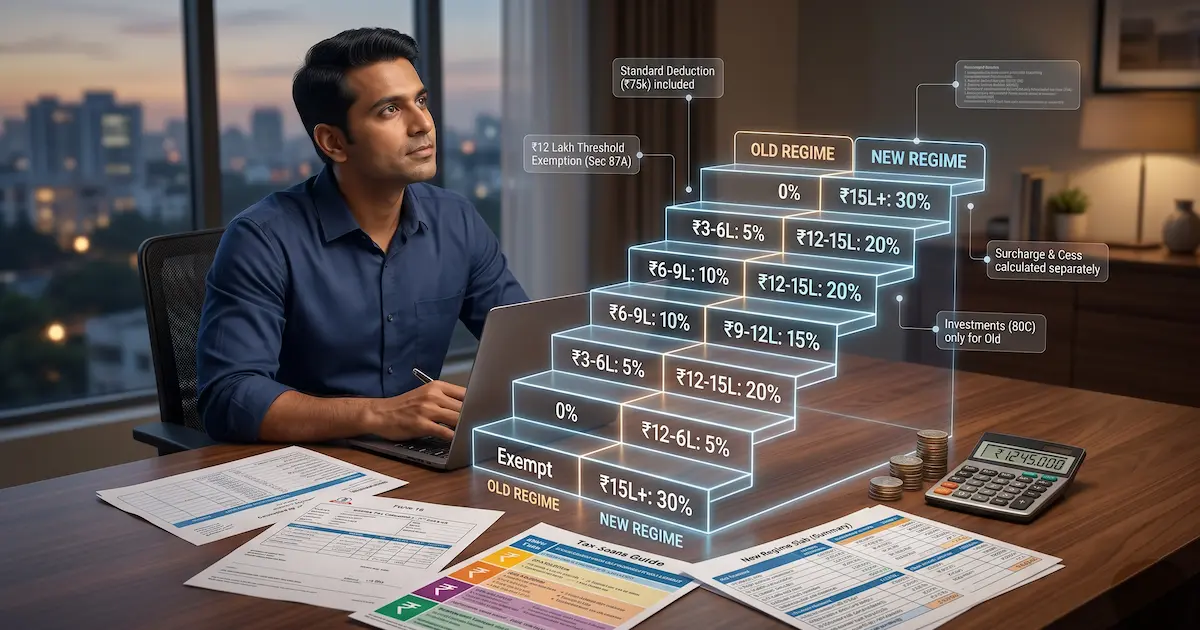

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read