Pillar 9

Banking and Account Basics

Bank accounts are the foundation underneath every other personal-finance decision, and most people use them without understanding what each account type actually is. This section covers checking accounts, savings accounts, fixed deposits, UPI, IFSC codes, deposit insurance, and the mechanics underneath everyday banking. Universal concepts plus India-specific instruments (UPI, IFSC, FD, DICGC) and US-specific ones (FDIC, routing numbers, money market accounts).

14 articles

What a joint bank account is and how it works, compared for the US and India: types and operating modes, deposit insurance (FDIC vs DICGC), survivorship, and the risks.

13 min read

Wire transfer vs ACH compared on speed, cost, reversibility, and safety, with a full table, where FedNow and RTP fit, and how it maps to India's NEFT, RTGS, and UPI.

12 min read

Current account vs savings account in India: a current account is a non-interest bank account built for businesses and high-volume transactions, while a savings account is an interest-bearing account for individuals. How they differ on interest, transaction limits, and minimum balance.

9 min read

What is banking? A comprehensive introduction to the account types, payment rails, deposit insurance, and fee structures that form the foundation of personal finance. Covers checking and savings accounts, fixed deposits and CDs, FDIC and DICGC deposit insurance, UPI and the India payments stack, US ACH and wire transfers, overdraft protection, money market accounts, and bank fees, for India and US audiences.

11 min read

What are the bank fees you're actually paying? Monthly maintenance, overdraft, ATM, wire, foreign transaction, minimum balance penalties, SMS alert charges, debit card annual fees, covers the full fee surface at both US and Indian banks, with current Q1 2026 fee schedules, the waiver conditions that eliminate most fees, and the structural choice of online vs traditional banks that determines the baseline.

10 min read

What is overdraft protection? An opt-in bank service that covers transactions exceeding your account balance, usually for a $35 average fee per occurrence in the US (CFPB data). Covers how overdraft fees work, the Regulation E opt-out, the cheaper alternative of linking a savings account, and India's overdraft facility (OD against FD or salary) which functions differently from US overdraft protection.

9 min read

What is a money market account (MMA)? A US deposit account that blends savings-account FDIC coverage with checking-account features, paying 4-5% APY at top online banks in Q1 2026, allowing limited cheque writing and debit card use, and requiring higher minimum balances ($1,000-25,000) than standard savings. Covers how MMAs differ from money market mutual funds, why India's liquid mutual funds fill the same role, and when an MMA beats a HYSA.

9 min read

India uses IFSC codes; the US uses ABA routing numbers. See each format, the US-India equivalents, and the SWIFT code you need to wire money abroad.

13 min read

What is UPI? The Unified Payments Interface built by NPCI on RBI's mandate in 2016, instant 24/7 bank-to-bank transfers using a Virtual Payment Address (VPA). Covers the underlying architecture, transaction limits, the ₹16+ lakh crore processed monthly across 600+ member banks, autopay mandates, UPI Lite for small payments, and how the rails differ from IMPS/NEFT/RTGS.

10 min read

What is the difference between IMPS, NEFT, and RTGS? Three Reserve Bank of India payment systems with different speeds, limits, and use cases, IMPS is instant 24/7 up to ₹5 lakh, NEFT settles in 30-minute batches with no upper limit, RTGS is real-time for transfers ₹2 lakh and above. Covers fee structures, processing times, transaction limits, and which rail to pick for different scenarios.

10 min read

DICGC insures ₹5 lakh per Indian bank; FDIC insures $250,000 per US bank. The rules, what is and isn't covered, the 90-day payout, and FDIC vs NCUA vs SIPC.

16 min read

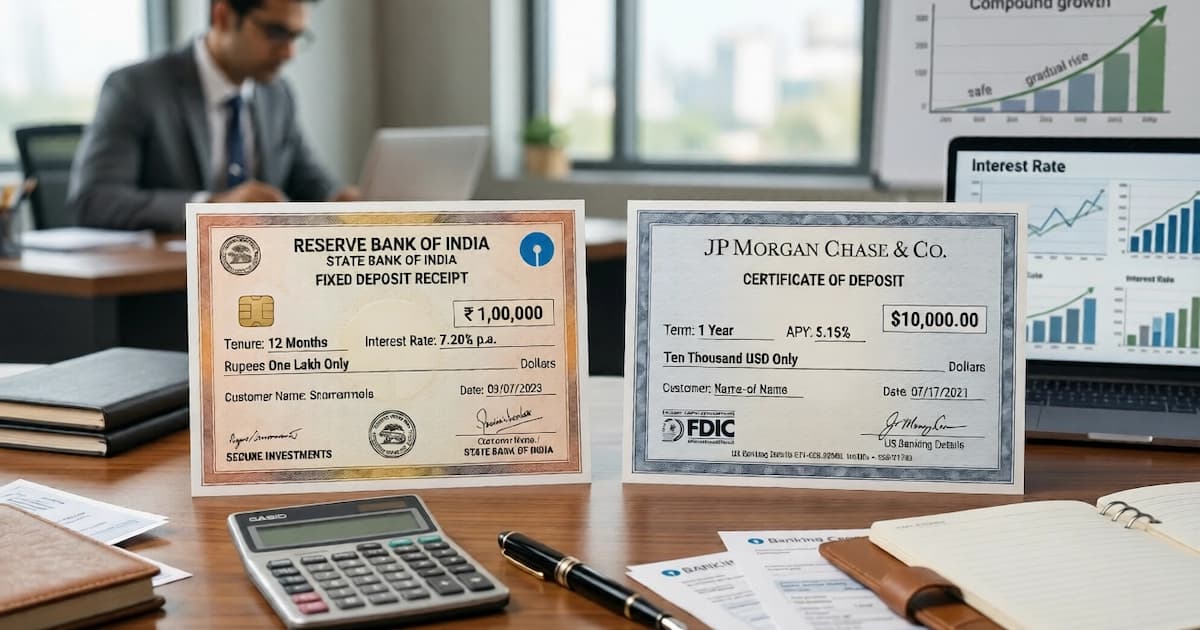

What is a fixed deposit (FD) in India and a certificate of deposit (CD) in the US? Both are time deposits, money locked at a fixed interest rate for a set tenure. Indian FDs paid 6.5-8% in Q1 2026 (small finance banks at the top end), US CDs paid 4.5-5.25% at online banks. Covers the math, the early-withdrawal penalty, DICGC vs FDIC coverage, and the senior-citizen rate bump.

10 min read

What is a savings account? An interest-bearing deposit account designed to park money you don't need immediately, paying 2.5-4% in Indian SB accounts, 0.46% in average US accounts, and 4-5% in US high-yield online savings. Covers how interest is calculated, the DICGC ₹5 lakh and FDIC $250,000 coverage limits, minimum balance rules, and the practical difference between savings and a fixed deposit.

9 min read

What is a checking account? A transactional bank account for daily spending, debit card, direct deposit, bill pay, paper checks, that typically earns 0.01-0.07% APY, charges $5-35 in monthly and overdraft fees, and sits under $250,000 FDIC coverage in the US. India has no direct retail equivalent: savings accounts handle the transactional role, current accounts are for businesses.

9 min read