Banking and Account Basics Explained: What Each Account Type Is and How It Works

By Tapabrata Biswas · Published June 1, 2026 · 11 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

Banks are the institutions underneath almost every other personal-finance decision. Whether you're receiving salary, paying rent, investing, borrowing, or saving for a goal, money has to live somewhere safe and move somewhere accessible. That somewhere is a bank account, and the rules governing it — what account types exist, how deposits are protected, which payment rails connect them, what fees apply — form the foundation of personal money management. The Reserve Bank of India regulates Indian banking under the Banking Regulation Act of 1949; the US regulates banking through a layered structure of the Federal Reserve, FDIC, OCC, and state banking departments. Beneath both systems, the same architectural building blocks repeat — account types for liquidity tiers, deposit insurance for trust, payment rails for movement, fees that compound silently — just with different names.

This pillar page introduces banking as a discipline, summarizes the 10 posts in the Pillar 9 cluster, synthesizes the meta-principles that work across the India and US systems, and links to each individual post for deeper exploration of specific topics.

What banking basics actually is

Banking is the system of regulated institutions, account types, and payment rails that hold, protect, and move money for households and businesses. The system rests on three structural features:

- Account types matched to liquidity tiers. Checking for daily transactions, savings for short-horizon accumulation, fixed-term deposits for locked savings, money market for mid-tier yield with check access. Each type trades yield for accessibility along a predictable curve.

- Deposit insurance as the trust foundation. Government-backed coverage (FDIC in the US, DICGC in India) protects depositors up to a statutory cap even if the bank fails — converting bank deposits from credit risk into something close to sovereign risk.

- Payment rails for value movement. Different rails optimize for different combinations of speed, cost, and use-case (UPI for instant retail in India, ACH for batched recurring in the US, wires/RTGS for high-value urgent, NEFT/Zelle for the in-between cases).

The regulators and authorities that define how all this works:

| Authority | Jurisdiction | What they govern |

|---|---|---|

| Reserve Bank of India (rbi.org.in) | India | All scheduled commercial banks, monetary policy, payment systems oversight |

| NPCI (npci.org.in) | India | UPI, IMPS, RuPay, NACH — the operational backbone of Indian retail payments |

| DICGC (dicgc.org.in) | India | Deposit insurance up to ₹5 lakh per depositor per bank |

| US Federal Reserve (federalreserve.gov) | US | Monetary policy, bank supervision, payment systems (Fedwire, FedNow) |

| FDIC (fdic.gov) | US | Deposit insurance up to $250,000 per depositor per insured bank |

| Consumer Financial Protection Bureau (consumerfinance.gov) | US | Consumer protection, fee disclosure rules, overdraft regulations |

| US Treasury (home.treasury.gov) | US | Currency, government accounts, AML compliance |

The 10 banking concepts covered in this pillar

1. What a checking account is — built for transactions, not yield

A checking account is a deposit account designed for everyday transactions — unlimited debit and ATM access, bill pay, debit card linkage, direct deposit, paper checks (in the US). Checking accounts typically pay little to no interest (0.07% national average APY per FDIC data as of 2025) because the bank uses the float to fund operations. The defining property is access frequency, not yield. Most households use checking as the central hub for monthly cash flow, with money routed in (salary) and out (rent, bills, transfers to savings) before settling at a baseline working balance.

Read the full post: What Is a Checking Account

2. What a savings account is — built to accumulate, with interest

A savings account is a deposit account designed to hold money and pay interest on the balance. US national average savings APY was 0.46% as of 2025 per FDIC, but high-yield savings accounts (HYSAs) from online banks pay 4-5% APY (Marcus, Ally, SoFi, others as of Q2 2026). Indian savings rates range from 2.7% at SBI to 7% at IDFC FIRST and small finance banks. Historically the US Regulation D 6-per-month withdrawal cap distinguished savings from checking; that cap was suspended in 2020 and most banks have not reinstated it. The split between checking and savings remains the foundation of personal banking — checking for flow, savings for accumulation.

Read the full post: What Is a Savings Account

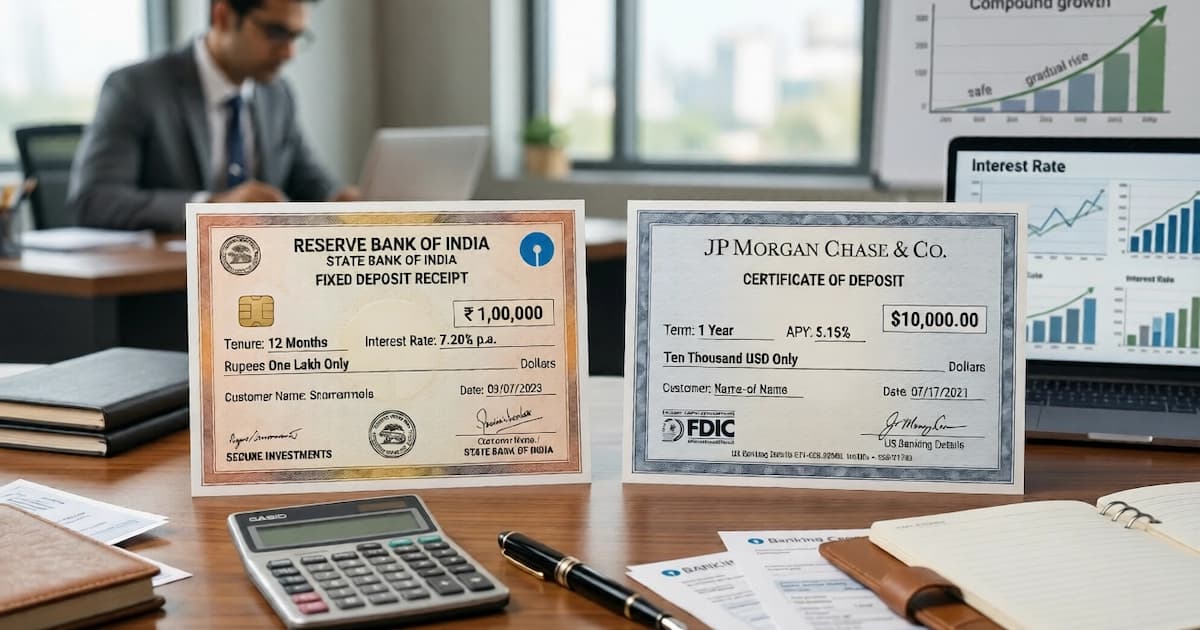

3. What FD vs CD is — the same instrument with different names

A Fixed Deposit (India) and a Certificate of Deposit (US) are the same instrument under different names — a deposit where the customer commits to leaving money with the bank for a fixed term in exchange for a guaranteed interest rate higher than the regular savings rate. Indian FD rates range 6.5%-8.5% across PSU banks and small finance banks as of Q2 2026; US CD rates range 4-5% on 1-5 year terms at most banks. Both penalize early withdrawal (typically 0.5%-1% interest deduction or last 90 days of interest forfeited). The mechanics are identical; only the regulatory wrapper and currency differ.

Read the full post: What Is FD vs CD Explained

4. FDIC vs DICGC — the deposit insurance that makes the system work

Deposit insurance is the government-backed guarantee that protects deposits up to a statutory cap if the bank fails. FDIC (US) covers $250,000 per depositor per insured bank — the current cap set by the Dodd-Frank Act of 2010 (raised from $100,000). DICGC (India) covers ₹5 lakh per depositor per bank — raised from ₹1 lakh in February 2020 after the PMC Bank crisis. Both are government-backed (FDIC by the US Treasury implicitly, DICGC by the RBI as a wholly-owned subsidiary). Below the cap, deposits are protected even if the bank collapses; above the cap, deposits become unsecured claims in liquidation. Spreading large balances across multiple insured banks preserves full coverage.

Read the full post: FDIC vs DICGC Deposit Insurance Explained

5. What UPI is — the payment system that reshaped Indian banking

UPI (Unified Payments Interface) is an instant, interoperable, mobile-first payment system that lets any UPI-linked Indian bank account send or receive money to/from any other UPI-linked account using a virtual ID. Launched by NPCI in April 2016, UPI processed 18.4 billion transactions worth ₹24.77 lakh crore in March 2025 alone — making it the largest real-time payment system in the world by volume. Transactions are free for retail users, instant (sub-second settlement), and capped at ₹1 lakh per transaction (₹2 lakh for some categories like education and insurance). UPI has structurally displaced cash for everyday transactions in urban India, and is the reason Indian retail banking looks fundamentally different from US retail banking.

Read the full post: What Is UPI Explained

6. IMPS vs NEFT vs RTGS — three payment rails for different jobs

IMPS, NEFT, and RTGS are three Indian payment rails optimized for different combinations of speed, settlement timing, and transfer value. IMPS (Immediate Payment Service) is instant 24/7, free at most banks, capped at ₹5 lakh per transaction. NEFT (National Electronic Funds Transfer) is batched (half-hourly settlement), free since January 2020, no value cap. RTGS (Real-Time Gross Settlement) is real-time for high-value transfers, minimum ₹2 lakh, no fee. UPI runs on top of the IMPS rail. Choosing the right rail is a function of value, urgency, and whether the recipient bank supports UPI or IMPS.

Read the full post: IMPS vs NEFT vs RTGS

7. Routing number vs IFSC code — the same identifier under different names

A routing number (US) and an IFSC code (India) are both bank-identifier codes that uniquely identify a bank branch in the country's payment system — required when initiating ACH/wire transfers (US) or NEFT/RTGS/IMPS transfers (India). US routing numbers are 9 digits, assigned by the American Bankers Association (ABA), and identify the bank itself (not the branch — the same routing number is shared across all branches of the same bank in many cases). IFSC codes are 11 alphanumeric characters, assigned by the RBI, and identify a specific branch (first 4 letters bank, 5th character "0" reserved, last 6 characters branch). Both serve the same function: route the transfer to the correct destination institution.

Read the full post: Routing Number vs IFSC Code Explained

8. What overdraft protection is — and why it's controversial

Overdraft protection is a bank service that covers transactions when the account balance is insufficient — typically by charging an overdraft fee per transaction. The US CFPB reported overdraft fees totalled $5.8 billion across US banks in 2023 (down from a peak of $14 billion in 2019 after CFPB scrutiny). Typical fees run $25-35 per overdraft transaction, often levied multiple times per day. In India, overdraft facilities are typically tied to current accounts and small-business accounts, with interest charged on the overdrawn amount rather than a flat fee. The structural critique: opt-in overdraft is now required in the US for one-time debit transactions per CFPB Regulation E amendments — meaning customers actively choose this service rather than being defaulted into it.

Read the full post: What Is Overdraft Protection

9. What a money market account is — a savings-CD hybrid

A money market account (MMA) is a deposit account that pays higher interest than a regular savings account in exchange for higher minimum balance requirements and limited check-writing. US MMA rates run 4-5% at top online banks (similar to HYSA rates), with typical minimum balances of $1,000-$10,000 and 6-check-per-month limits at most institutions. MMAs are FDIC-insured like other deposit accounts. The distinguishing feature from a savings account is the limited check-writing capability — useful for a household keeping a large balance but occasionally needing to write a check from it without moving the money to checking first. India does not have a direct MMA equivalent; the functional analogue is a flexi-FD or sweep account.

Read the full post: What Is a Money Market Account

10. Bank fees — the silent compounding cost

Bank fees are the recurring charges banks levy for account maintenance, transaction processing, and service usage — and their cumulative cost over years is often larger than depositors realize. Common categories: monthly maintenance fees ($5-25/month US, often waived with minimum balance), ATM fees ($2-5 per out-of-network withdrawal), overdraft fees ($25-35 US), wire transfer fees ($15-50 US, ₹25-200 India), foreign transaction fees (2-3% on debit card transactions abroad), and minimum-balance penalty fees. A worked example: a US household paying a $12 monthly maintenance fee + 4 out-of-network ATM withdrawals at $3 each = $24/month in fees, or $288/year — equivalent to a 7% drag on a $4,000 balance held in that account. The mitigation: choose fee-free accounts (online banks, credit unions, India's Jan Dhan Yojana zero-balance accounts) and audit fee disclosure statements annually.

Read the full post: What Are Bank Fees Explained

The synthesis — three principles that work across the system

Reading 10 individual concept explanations is useful; the practical payoff is understanding the meta-principles that hold across both India and US banking systems.

Principle 1: Deposit insurance is the foundation, not yield

The yield difference between a 0.5% savings account and a 5% HYSA looks dramatic, but neither matters if the bank fails and the deposit is above the insurance cap. The single most important question for any deposit account is: is this institution covered by FDIC or DICGC, and is my balance within the per-depositor-per-bank cap? Once that's confirmed, optimize for yield within the insured envelope. Spread balances above the cap across multiple insured banks rather than chasing yield at a single uninsured institution.

Principle 2: Account type matches liquidity horizon, not preference

The right account isn't a matter of preference — it's a function of when the money is needed. Money you'll use this month belongs in checking. Money you might need within 6 months belongs in a high-yield savings account. Money you genuinely won't need for 1-5+ years belongs in an FD or CD (or longer-horizon instruments outside the scope of this pillar). Matching liquidity horizon to account type maximizes yield without sacrificing access. Mismatches go in both directions: large emergency funds in 0.07% checking accounts forfeit ~5% of yield annually; rent money locked in a 5-year CD triggers early-withdrawal penalties that erase the yield premium.

Principle 3: Payment rails are tools, not defaults

The right payment rail for any given transfer is a function of value, urgency, and recipient setup — not personal habit. Sending ₹500 to a friend? UPI is free and instant. Sending ₹3 lakh to a vendor? IMPS or NEFT, not UPI (which caps at ₹1 lakh). Paying a US contractor $50,000? Wire transfer for same-day, or ACH for 2-3 business days at no fee. Using the wrong rail wastes either money (wire fee for low-urgency transfer) or time (ACH for an urgent payment). The matrix worth memorizing:

| Need | India | US |

|---|---|---|

| Instant small retail | UPI (free, ₹1L cap) | Zelle (free between supported banks) |

| Same-day larger | IMPS (free, ₹5L cap) | Wire ($15-50 fee) |

| Non-urgent recurring | NEFT (free, any amount) | ACH (free, 1-3 days) |

| High-value urgent | RTGS (free, ₹2L minimum) | Wire / Fedwire ($15-50) |

The cumulative cost of mismatched banking choices

How much do banking misalignments cost a household across a career? Order-of-magnitude estimates:

| Misalignment | Approx. annual cost (typical household) | 30-year compounded cost |

|---|---|---|

| Emergency fund in 0.5% bank instead of 5% HYSA (₹3 lakh / $4,000) | ₹13,500 / $180 | ~₹6-8 lakh / $10-12K foregone |

| Salary parked in checking instead of swept to savings | ₹5K-15K / $100-300 | ~₹3-9 lakh / $6-18K foregone |

| Recurring overdraft fees | — / $200-500 | — / $15-40K compounded |

| Wire transfer fees for non-urgent recurring transfers | $200-500 | $15-40K compounded |

| Account spread above DICGC/FDIC cap, single-bank concentration | Variable; catastrophic in tail risk | One bank failure = up to ₹5L+ / $250K+ loss |

| Monthly maintenance fees on accounts that could be fee-free | ₹0-3K / $60-300 | ~₹1-3 lakh / $5-18K |

| Foreign transaction fees on routine international spending | 2-3% of FX volume | Variable; substantial for cross-border earners |

A household that consistently makes the right account-type and payment-rail choices captures roughly ₹10-30 lakh (Indian context) or $25,000-$80,000 (US context) of additional terminal wealth across a career — without any change in income or investment behaviour.

Where to start

If you're new to banking optimization and want a concrete starting point rather than reading all 10 individual posts immediately, four sequenced steps that capture most of the practical benefit:

1. Confirm deposit insurance on every account. List your current bank accounts. For each, confirm the bank is FDIC-insured (US: search at fdic.gov/banks) or DICGC-insured (India: most scheduled banks are; co-operative banks may not be — verify at dicgc.org.in). For any account with balance above the per-bank cap ($250,000 US or ₹5 lakh India), split the excess to a second insured bank.

2. Move idle savings to a high-yield account. If your emergency fund is sitting in a 0.5% savings account, move it to a HYSA paying 4-5% (US) or to one of the higher-paying private/small finance banks (India). The migration takes 30 minutes and is the single highest-ROI banking optimization available — typically $150-300 (US) or ₹10,000-25,000 (India) of additional annual interest on a typical emergency fund balance.

3. Audit your bank statement for recurring fees. Pull the last 12 months of statements. Highlight every fee. Calculate the annual total. For each recurring fee, evaluate whether it can be eliminated by switching to a fee-free account or by changing usage (avoid out-of-network ATMs, set up direct deposit to waive maintenance fees, opt out of overdraft protection if you don't actively want it).

4. Match each payment to the right rail. Stop defaulting to one payment method for everything. Use UPI / Zelle for small instant transfers, NEFT / ACH for non-urgent recurring, IMPS / wire for same-day larger, RTGS / Fedwire for high-value urgent. The rail-selection discipline saves both money (wire fees) and time (failed/delayed transfers).

Beyond these four, the individual posts in this pillar each cover specific accounts, rails, and fee structures in depth. Browse the list above and read whichever ones match the banking decisions you're currently navigating.

The deeper principle: banking isn't a single product to optimize — it's a small portfolio of accounts and rails that, configured correctly, quietly compound advantages across every other personal-finance decision you make.

Frequently asked questions

What's the difference between a checking account and a savings account? A checking account is built for everyday transactions — unlimited debit and ATM access, bill pay, debit card linkage — and typically pays little to no interest. A savings account is built for accumulating money, pays interest (0.46% national-average APY in the US per FDIC as of 2025; 2.5%-7% in Indian banks depending on the bank), and historically had stricter transaction limits (the US Regulation D 6-per-month cap was suspended in 2020 and remains relaxed at most banks). Most households use both — checking for monthly cash flow and bills, savings for the emergency fund and short-term goals. The split is the foundation of personal banking, with the savings account paying interest on idle money the checking account would not.

How safe is my money in a bank? Bank deposits at regulated banks are insured up to a per-depositor cap — $250,000 per depositor per insured bank in the US (FDIC, Dodd-Frank Act 2010), ₹5 lakh per depositor per bank in India (DICGC, raised from ₹1 lakh in February 2020 after the PMC Bank crisis). The insurance is government-backed: FDIC by the US government, DICGC by the Reserve Bank of India as a wholly-owned subsidiary. Below the cap, deposits are protected even if the bank fails. Above the cap, deposits become unsecured claims in the bank's liquidation. The practical implication: spread large balances across multiple insured banks to keep the entire balance within insured limits.

Which payment rail should I use for which type of transfer? In India (as of Q2 2026): UPI for small everyday transactions (free, instant, ₹1 lakh per transaction cap, processed 18.4 billion times in March 2025 alone per NPCI), IMPS for instant transfers above the UPI limit (free at most banks, ₹5 lakh cap), NEFT for non-urgent transfers in batches (free since January 2020), and RTGS for high-value urgent transfers (₹2 lakh minimum, no fee). In the US: ACH for low-cost recurring transfers (free, 1-3 business days), wire transfers for same-day high-value transfers ($15-50 sender fee), and Zelle for instant person-to-person transfers between US banks (free between supported banks).

Where should I start if I'm setting up banking from scratch? Three accounts handle 95% of cases. First, one checking account at any major regulated bank for everyday cash flow. Second, one high-yield savings account (HYSA in the US offering 4-5% APY at top online banks as of 2026, regular savings at the higher-paying private banks in India) for the emergency fund and short-term goals. Third, one fixed-term deposit (FD in India, CD in the US) for any money you genuinely will not need for 6-12+ months. Confirm FDIC or DICGC insurance coverage on each bank before depositing meaningful sums. Skip money market accounts unless you specifically need check-writing on a higher-yield account, and skip overdraft protection unless you understand exactly what the fee structure is.

Sources

- Reserve Bank of India, Banking Regulation Act and Master Directions — rbi.org.in

- National Payments Corporation of India, UPI / IMPS / NACH Operations — npci.org.in

- Deposit Insurance and Credit Guarantee Corporation, Deposit Insurance Scheme — dicgc.org.in

- Federal Deposit Insurance Corporation, Deposit Insurance Coverage — fdic.gov

- US Federal Reserve, Payment Systems and Bank Supervision — federalreserve.gov

- Consumer Financial Protection Bureau, Overdraft Practices and Fees Report 2023 — consumerfinance.gov

- US Treasury, Currency and Financial System Oversight — home.treasury.gov

- FDIC National Rates and Rate Caps Report (monthly) — fdic.gov/resources/bankers/national-rates

- NPCI UPI Product Statistics (monthly) — npci.org.in/what-we-do/upi/product-statistics

- Indian Banks' Association, Service Charges and Fee Disclosure Norms — iba.org.in

You might also like

A checking account is the bank account you use for everyday spending. How it works, the types, what you need to open one, and the fees to watch for.

10 min read

What is a savings account? An interest-bearing deposit account designed to park money you don't need immediately, paying 2.5-4% in Indian SB accounts, 0.46% in average US accounts, and 4-5% in US high-yield online savings. Covers how interest is calculated, the DICGC ₹5 lakh and FDIC $250,000 coverage limits, minimum balance rules, and the practical difference between savings and a fixed deposit.

9 min read

What is a fixed deposit (FD) in India and a certificate of deposit (CD) in the US? Both are time deposits, money locked at a fixed interest rate for a set tenure. Indian FDs paid 6.5-8% in Q1 2026 (small finance banks at the top end), US CDs paid 4.5-5.25% at online banks. Covers the math, the early-withdrawal penalty, DICGC vs FDIC coverage, and the senior-citizen rate bump.

10 min read