Tax Concepts Explained: Definitions and Mechanics for India and US Taxpayers

By Tapabrata Biswas · Published May 25, 2026 · 12 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is the pillar page for The Money Decoded's Tax Concepts cluster — a research-led catalog of definitional explainers covering the most-discussed tax concepts in India and the United States. Nothing in this pillar is tax planning, filing, or compliance advice. Tax law is statutory, changes with every Union Budget (India) and Tax Act (US), and applies to individual situations in ways that only a qualified Chartered Accountant in India or Certified Public Accountant in the US can correctly assess. For any tax decision affecting your specific situation, consult a CA or CPA.

The pillar exists because tax content on the open internet sits at one of two extremes: highly technical primary-source documentation (Income Tax Act sections, IRS publications, CBDT notifications) that requires professional training to read fluently, or marketing-driven prescription content ("best 80C investments", "tax-saving strategies for salaried", "how to maximise your refund") that confuses Zone A education with Zone B advice. This pillar deliberately occupies a third position: definitional, research-led, explicitly non-prescriptive. Every post tells you what a concept is, how it is structured by law, and where it sits in the broader tax architecture — and tells you to bring your specific situation to a CA/CPA for any decision that turns on it.

This page synthesizes the 10 cluster posts, summarises the foundational concepts, surfaces meta-principles that apply across them, and provides a three-step starting guide for new readers.

For salaried filers: our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26) pulls the most-used concepts in this pillar — regime choice, Form 16, Section 80C, HRA, capital gains, and step-by-step filing — into one complete walkthrough for the return due July 31, 2026.

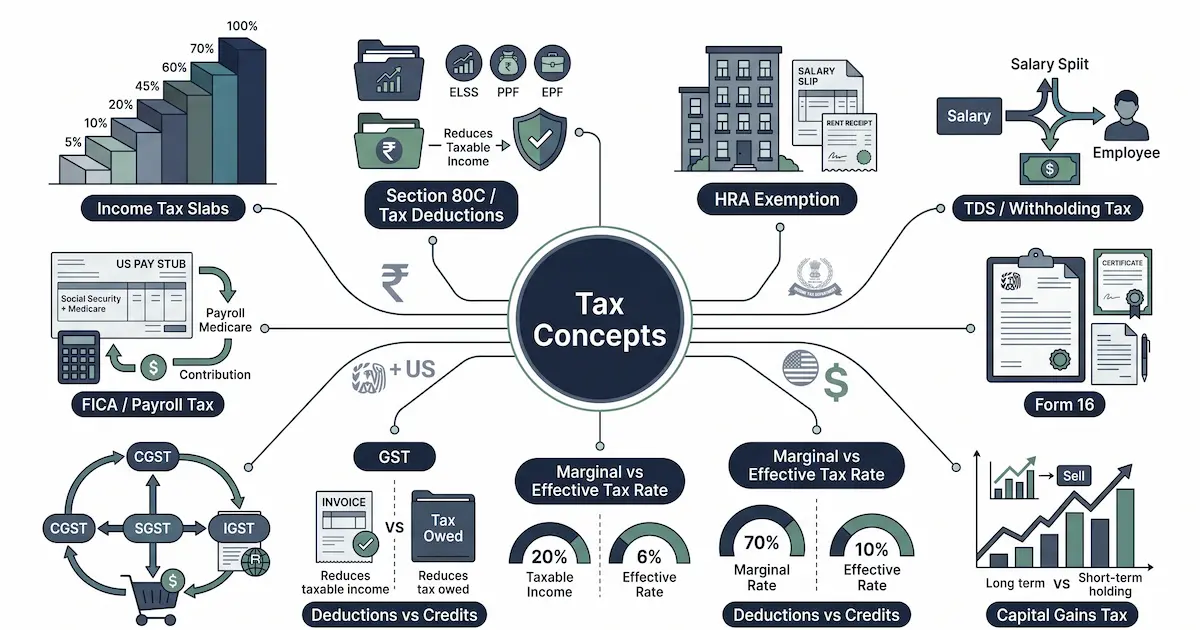

The 10 posts in this pillar

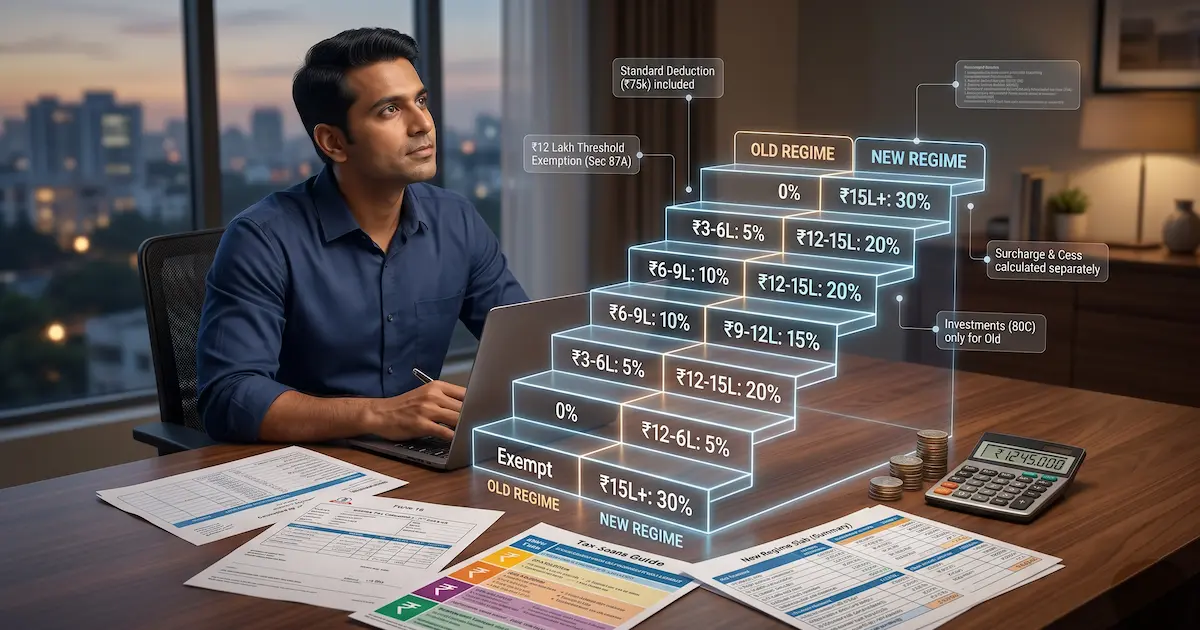

1. Income Tax Slab India Explained

The progressive-slab structure that determines income tax for every salaried and self-employed Indian. Covers the FY 2025-26 new regime slabs (₹4L exempt → 30% above ₹24L), the unchanged old regime slabs (₹2.5L exempt → 30% above ₹10L), the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction (₹75,000 new / ₹50,000 old), surcharge tiers (10/15/25% at ₹50L/₹1cr/₹2cr), and the 4% Health and Education Cess. Includes a fully worked ₹15L salary example arriving at ₹97,500 total tax / 6.5% effective rate.

→ Income Tax Slab India Explained

2. What Is Section 80C Deduction

The ₹1.5 lakh annual deduction available under India's old regime only — the most-discussed tax provision among salaried Indians. Covers the eligible-instrument list (PPF, EPF, ELSS, NSC, life insurance premium, home loan principal, tuition fees, SSY, SCSS), lock-in periods and current Q1 2026 yields per instrument, the related Section 80CCD(1B) additional ₹50,000 NPS deduction (above the ₹1.5L cap), Section 80CCD(2) employer NPS as the only NPS deduction the new regime allows, and the regime-choice trade-off framing.

→ What Is Section 80C Deduction

3. What Is HRA Exemption Explained

The Section 10(13A) + Rule 2A formula that determines how much of your House Rent Allowance escapes income tax. Covers the three-condition formula (minimum of actual HRA / 50%-40% basic / rent minus 10% basic), the metro classification limited to Mumbai/Delhi/Kolkata/Chennai, documentation requirements including the CBDT Circular 8/2013 landlord-PAN requirement above ₹1 lakh annual rent, and a Mumbai worked example arriving at ₹2.4 lakh exempt HRA / ~₹75K tax saved.

→ What Is HRA Exemption Explained

4. What Is TDS (Tax Deducted at Source)

The mechanism where the payer deducts tax before paying you and deposits it with the IT Department on your behalf. Covers the major sections relevant to individuals — Section 192 (salary), 194A (bank interest), 194 (dividends), 194I (rent), 194J (professional fees), 194C (contractor payments) — with current FY 2025-26 thresholds. Includes the Section 206AA 20% rate for PAN-less recipients, the Form 26AS + AIS reconciliation framework, and a worked ₹15L salary + ₹60K FD interest example showing ₹1,03,500 total TDS reconciled against final ~₹1,06,000 liability.

→ What Is TDS (Tax Deducted at Source)

5. What Is Form 16 India

The TDS certificate every salaried Indian receives from their employer by June 15 of the assessment year. Covers the structural split between Part A (TRACES-generated, tamper-resistant, quarter-by-quarter TDS deposit detail) and Part B (employer-prepared, salary breakup + exemptions + deductions + tax calculation). Includes the Form 16A distinction (non-salary TDS), the seven-step ITR filing flow using Form 16, and the reconciliation procedure for Part A vs Form 26AS mismatches via Form 24Q correction.

6. What Is Capital Gains Tax — Short vs Long Term

The tax on profits from selling capital assets, with rates dependent on holding period. Covers India's post-Budget-2024 structure effective 23 July 2024 (LTCG equity 12.5% above ₹1.25L, STCG equity 20%, all non-equity LTCG unified at 12.5% without indexation, holding periods unified to 12-month listed / 24-month other), the US structure (0%/15%/20% LTCG brackets, STCG taxed as ordinary income, wash-sale rules, 3.8% NIIT above income thresholds), and Section 54/54EC/54F (India) + Section 121/1031 (US) exemption provisions noted with explicit consult-CA/CPA caveats.

→ What Is Capital Gains Tax — Short vs Long Term

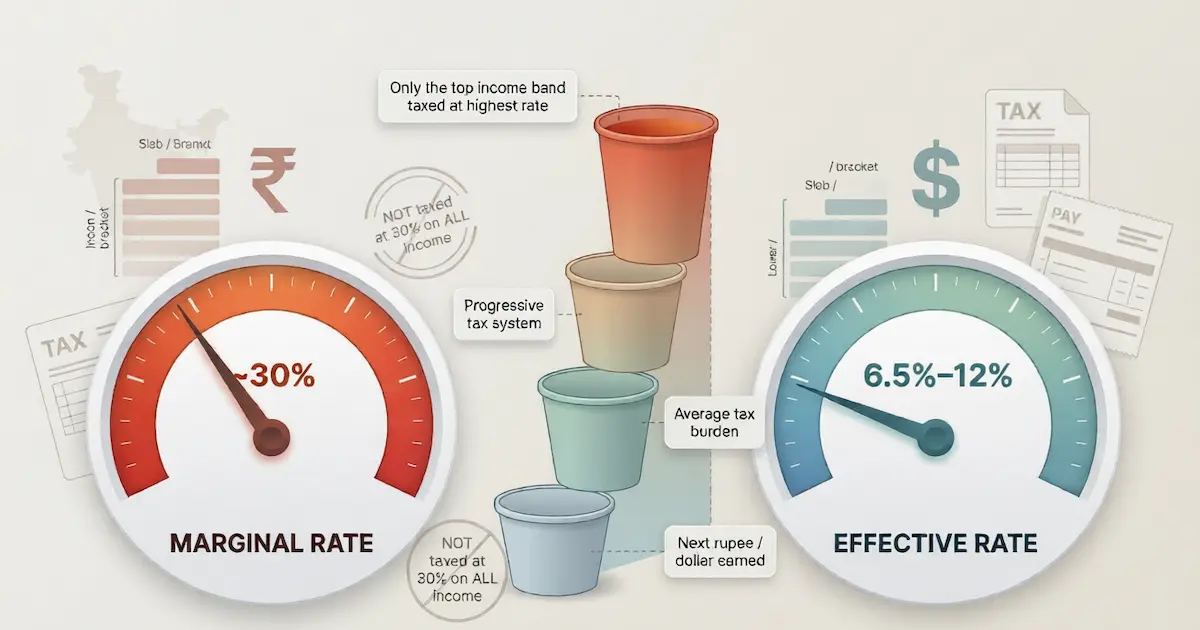

7. Marginal vs Effective Tax Rate Explained

The two related but distinct rates that everyone in a progressive tax system needs to understand. Marginal rate = the rate on the next rupee/dollar earned (the "bracket" rate). Effective rate = total tax / total income (the "average" rate). The structural gap between them (always: effective < marginal) and the common "tax bracket" misconception that drives bad income decisions. Worked examples for India (₹15L: 15% marginal / 6.5% effective) and US ($90K single TY 2025: 22% marginal / 12.5% effective). Decision matrix showing when to use marginal (raise evaluation, deduction value) vs effective (budget planning, total burden).

→ Marginal vs Effective Tax Rate Explained

8. Tax Deductions vs Credits, Standard vs Itemized

The four mechanisms US tax law uses to reduce your tax bill, plus the parallel India structures. Deduction reduces taxable income (saves marginal-rate × deduction); credit reduces tax owed dollar-for-dollar. Refundable vs non-refundable credits. TY 2025 standard deduction amounts ($15,750 single / $31,500 MFJ). Itemizable expense categories with limits (SALT $10K cap, mortgage interest $750K principal cap, charitable 60% AGI, medical above 7.5% AGI). Two worked scenarios showing when standard wins vs when itemized wins. India parallels — Chapter VI-A deductions, Section 87A rebate as credit equivalent, standard deduction with no US-style itemize option.

→ Tax Deductions vs Credits, Standard vs Itemized

9. What Is GST India Explained

India's unified indirect tax since 1 July 2017 — the 101st Constitutional Amendment that subsumed 17 earlier central and state taxes. Covers the constitutional framework (GST Council with 33 members and 75% weighted vote), the five rate slabs (0%, 5%, 12%, 18%, 28% + Compensation Cess) with examples of goods in each, the CGST + SGST mechanism for intra-state supplies, IGST for inter-state, Input Tax Credit to prevent cascading, registration thresholds (₹40L goods / ₹20L services in most states), and the Composition Scheme rates and trade-offs.

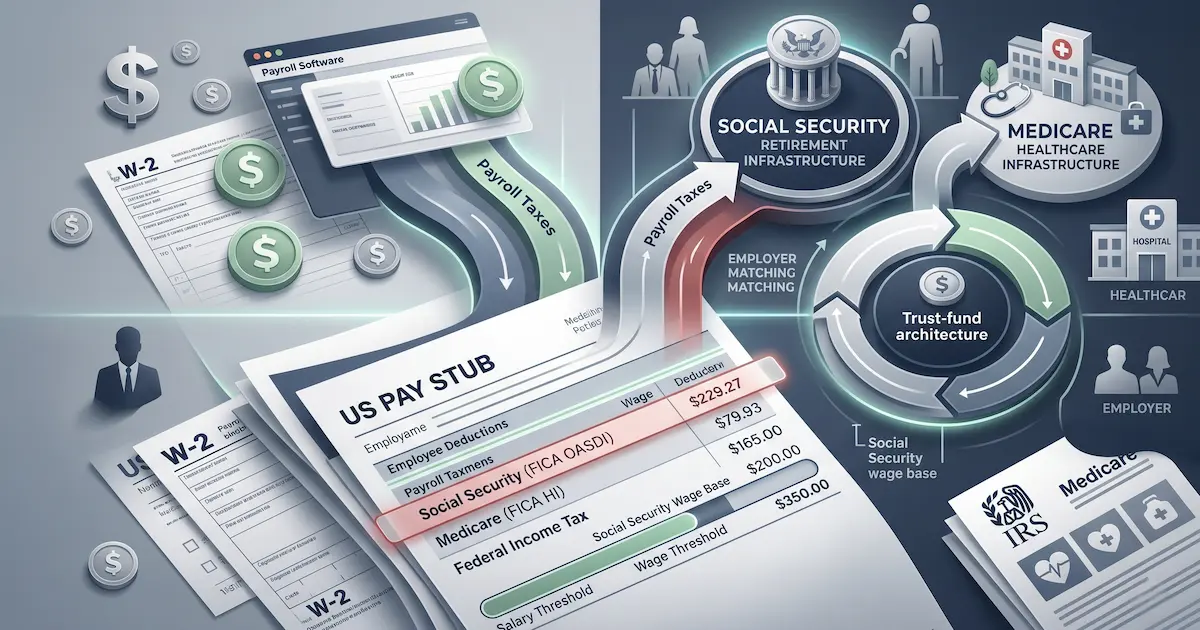

10. What Is FICA Tax Explained

The US payroll tax funding Social Security and Medicare. Covers the two components — Social Security at 6.2% on wages up to the wage base ($176,100 for 2025), Medicare at 1.45% on all wages, plus 0.9% Additional Medicare above income thresholds. The employer match doubling the total burden to 15.3% up to the wage base. SECA treatment for self-employed (both halves on Schedule SE). What the trust funds actually pay for (Social Security retirement/disability/survivors + Medicare Part A hospital insurance). Brief India comparison to EPF (12% + 12% on basic) and ESIC (0.75% + 3.25%) as parallel payroll-based social security.

Authoritative sources cited across the pillar

Every claim in this pillar is sourced to a primary government authority or its equivalent — never to a secondary financial-media source. The hierarchy:

| Authority | Jurisdiction | What they govern |

|---|---|---|

| Income Tax Department of India | India | Direct tax administration (individual + corporate income tax) |

| Central Board of Direct Taxes (CBDT) | India | Policy-setting body for direct taxes; issues notifications and circulars |

| Ministry of Finance, Govt of India | India | Union Budget and Finance Acts |

| GST Council | India | Indirect tax policy (constitutionally mandated centre-state body) |

| Central Board of Indirect Taxes and Customs (CBIC) | India | GST and customs administration |

| Tax Information Network (TIN-NSDL) | India | PAN issuance and TDS infrastructure |

| TRACES | India | TDS Reconciliation Analysis and Correction Enabling System |

| Employees' Provident Fund Organisation (EPFO) | India | EPF administration |

| Reserve Bank of India (RBI) | India | Banking-related tax interactions |

| US Internal Revenue Service (IRS) | US | Federal tax administration |

| US Social Security Administration (SSA) | US | Social Security and the FICA wage base |

| US Treasury | US | Tax policy and Federal regulations |

| US Congress | US | Internal Revenue Code (Title 26 USC) |

| Tax Policy Center | US | Analytical and policy commentary on tax provisions |

The pattern across the cluster: India-primary sources (Income Tax Department, CBDT, Ministry of Finance) for India-specific posts; IRS and SSA for US-specific posts; both for the merged India+US posts (capital gains, marginal-vs-effective, deductions-vs-credits).

Meta-principles synthesized from the cluster

Four structural principles emerge from reading the 10 posts together:

Principle 1 — Tax is statutory and changes annually

Every tax provision in both India and the US is set by legislation that can change yearly. India's Union Budget each February alters slab rates, deduction limits, and capital gains rates (Budget 2024 made the largest capital gains change in over a decade). The US Tax Cuts and Jobs Act of 2017 reshaped standard deductions and SALT caps; the TCJA changes are scheduled to sunset after TY 2025 unless Congress extends them. Never act on tax content without verifying current law against the relevant authority for your filing year. This applies to the posts in this pillar too — they reflect law as of writing in 2026 and should be cross-checked against primary sources before being relied on.

Principle 2 — India and US share concepts but differ structurally

The cluster repeatedly surfaces structural parallels with mechanical differences:

- Both use progressive slabs/brackets, but India has 2 parallel regimes (new + old) while the US has 1 with itemize-vs-standard within it

- Both have deductions and credits, but India's deductions live in a fixed-list Chapter VI-A while US deductions are itemizable expense categories

- Both tax capital gains with short-vs-long distinction, but at very different rates and with different exemption structures

- Both have payroll taxes funding social insurance, but US FICA → defined-benefit Social Security vs India EPF → defined-contribution provident fund

Cross-border readers (NRIs, dual-status taxpayers, US-employed Indians) need to recognise these structural parallels without confusing the mechanics. This is one of the strongest cases for working with a CA who understands both systems if your situation spans both jurisdictions.

Principle 3 — Awareness of concept ≠ ability to file correctly

Reading this pillar gives you the vocabulary to understand what your CA/CPA is doing during ITR/return preparation, what the IT Department is asking when scrutiny questions arrive, what salary structure changes mean for take-home pay, and what regime/itemize/exemption choices imply at a structural level. It does not give you the ability to file correctly. Filing requires:

- Applying current-year rates and rules correctly

- Reconciling all forms (Form 16, 16A, 26AS, AIS / 1099s, W-2)

- Choosing the correct ITR form / 1040 schedules

- Documenting eligibility for claimed deductions/exemptions

- Computing the precise tax liability under your specific situation

These are the activities of a qualified professional, not the activities of a general reader of educational content. The vocabulary in this pillar makes you a better client of that professional; it does not make you the professional.

Principle 4 — Tax planning is investment + tax + life decision combined

Multiple posts in the cluster surface the same observation: tax planning is rarely a pure tax question. It is usually tax + investment selection + life-circumstance optimisation:

- Regime choice (India) depends on deduction eligibility, which depends on investment choices, which depend on financial goals

- Itemize vs standard (US) depends on mortgage + state tax + charitable + medical, which depends on housing + state of residence + giving practices

- Capital gains timing depends on holding-period thresholds + asset class + current vs future income brackets

- Retirement-account choices (NPS in India, 401(k)/IRA in US) involve current marginal rate + expected retirement marginal rate + investment risk tolerance

For any of these, the right professional is rarely just a CA/CPA in isolation — it's a CA/CPA working alongside a SEBI-registered investment adviser (India) or fiduciary financial planner (US). The two together cover what either alone misses.

Where to start

The 10 posts are designed to be readable in any order, but four entry sequences make sense depending on your situation:

For Indian salaried taxpayers preparing for ITR season

The classic salaried-Indian sequence:

- Income Tax Slab India Explained — the foundation

- Marginal vs Effective Tax Rate Explained — understand the bracket math

- What Is Section 80C Deduction — the most-used old-regime provision

- What Is HRA Exemption Explained — if you rent in a metro

- What Is TDS (Tax Deducted at Source) — what your employer is doing

- What Is Form 16 India — your ITR-filing supporting document

Skip the US-specific posts unless you have US income.

For US salaried taxpayers

The US-focused sequence:

- Marginal vs Effective Tax Rate Explained — the foundation

- Tax Deductions vs Credits, Standard vs Itemized — the US-specific structure

- What Is FICA Tax Explained — payroll-tax mechanics

- What Is Capital Gains Tax — Short vs Long Term — for any investment activity

For someone evaluating an investment-sale decision

Capital gains decisions cut across both jurisdictions:

- What Is Capital Gains Tax — Short vs Long Term — the structural mechanics

- Marginal vs Effective Tax Rate Explained — for understanding what bracket the gain falls into

- (If Indian) Income Tax Slab India Explained — for understanding regime interaction with capital gains rates

- (If US) Tax Deductions vs Credits, Standard vs Itemized — for understanding loss offsetting

For an Indian small business owner

GST-focused entry:

- What Is GST India Explained — the indirect-tax structure

- What Is TDS (Tax Deducted at Source) — for understanding TDS-on-payments-received and TDS-on-payments-made

- Income Tax Slab India Explained — for understanding business-income taxation

- What Is Section 80C Deduction — if you have personal salaried income alongside business

In all cases, the educational content gives you the vocabulary; the actual filing/planning requires a qualified professional.

The standing recommendation across all 10 posts

Every post in this pillar ends with the same recommendation: consult a qualified Chartered Accountant in India or Certified Public Accountant in the US for your specific situation. This is not boilerplate — it is the genuine load-bearing conclusion of every piece. The structural reason: tax law is uniquely circumstance-dependent, uniquely high-stakes for getting wrong, and uniquely subject to annual change. No volume of general educational content can replace a professional who knows your specific situation and bears responsibility for the advice they give. This pillar exists to make you a better-informed client of that professional, not to replace them.

Tax law also rewards engagement with primary sources directly. The Income Tax Department's e-filing portal, the CBDT notification archives, the IRS publications website, and the GST Council press releases are all freely accessible and authoritative. Combine educational content (like this pillar), professional advice (from a CA/CPA), and primary-source verification (from the authority) for the most reliable picture of any tax situation.

Frequently asked questions

What is the purpose of this Tax Concepts pillar? This pillar provides definitional foundations for the most-discussed tax concepts in India and the United States — what tax slabs are, how deductions differ from credits, what TDS and Form 16 actually contain, how capital gains rates work, what GST and FICA fund, and the structural mechanics of each. It is deliberately definitional rather than prescriptive. The goal is for an Indian or US household to be able to read their pay stub, understand their salary structure, comprehend what a CA or CPA is doing during ITR/return preparation, and follow Budget announcements without needing translations. It is not — and is not intended to be — substitute for tax planning, filing assistance, or advice on specific decisions. Every post in this cluster directs readers to consult a qualified Chartered Accountant in India or Certified Public Accountant in the US for situation-specific advice.

How should I read this pillar — start to end, or pick by topic? Either approach works; the ten posts are designed to be readable in any order. The 'where to start' guide later in this page suggests focused entry sequences depending on whether you're primarily an Indian taxpayer, a US taxpayer, or evaluating capital gains decisions specifically. The foundational pair — income tax slabs and marginal-vs-effective tax rates — gives the conceptual scaffold that the rest of the cluster builds on. Once those two are clear, the others (TDS, Form 16, capital gains, etc.) can be read as needed when the specific situation arises. The pillar page itself synthesizes the meta-principles across all ten posts; reading it after browsing 2-3 specific posts often clarifies the pattern.

Why does every post in this pillar tell me to consult a CA or CPA? Because tax law is uniquely circumstance-dependent and uniquely high-stakes for getting wrong. Tax rules change annually with each Union Budget (India) or each Tax Act (US). The correct application to your specific situation depends on income sources, filing status, deduction eligibility, capital gains holding periods, residential status, and dozens of other variables a definitional explainer cannot incorporate. A misapplied tax claim becomes a defective return — at best a notice and correction, at worst penalty plus interest under Sections 234A/B/C (India) or accuracy penalties (US). Qualified Chartered Accountants in India and Certified Public Accountants in the US exist specifically to assess individual situations, apply current law correctly, and bear professional responsibility for the advice they give. General educational content like this pillar gives you the vocabulary to have an informed conversation with that professional; it does not replace the professional itself.

Does this pillar cover everything important about taxes? No — and that's deliberate. The 10 cluster posts cover the highest-traffic, most-asked tax concepts, but many important topics are intentionally out of scope. We do not cover: ITR filing forms (ITR-1 vs ITR-2 vs ITR-3 selection), specific Section 54/54EC/54F exemption procedures, NRI tax provisions and DTAA treaty benefits, business and corporate tax structure, GST return-filing mechanics (GSTR-1, GSTR-3B, GSTR-9), US partnership and S-Corp taxation, estate and gift tax, alternative minimum tax (AMT), state-specific US tax rules, and many other specialised areas. Each of these requires professional guidance and is better addressed by your CA/CPA than by general content. The pillar covers the foundational vocabulary; the specialised areas require the specialist.

Sources

- Income Tax Department of India — incometax.gov.in

- Central Board of Direct Taxes (CBDT) — incometaxindia.gov.in

- Ministry of Finance, Government of India — indiabudget.gov.in

- GST Council — gstcouncil.gov.in

- Central Board of Indirect Taxes and Customs (CBIC) — cbic.gov.in

- TRACES — tdscpc.gov.in

- Tax Information Network (TIN-NSDL) — tin-nsdl.com

- Employees' Provident Fund Organisation (EPFO) — epfindia.gov.in

- US Internal Revenue Service (IRS) — irs.gov

- US Social Security Administration (SSA) — ssa.gov

- US Treasury — home.treasury.gov

- Tax Policy Center — taxpolicycenter.org

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

What is the marginal tax rate vs the effective tax rate? Two related but distinct concepts in progressive tax systems. Marginal rate is the percentage applied to your next rupee or dollar of income; effective rate is total tax divided by total income. Covers worked examples for India (new regime ₹15L salary at 15% marginal / 6.5% effective) and the US (federal marginal 22% / effective ~12-14% typical), the most common bracket misconception, and why each rate matters for different decisions.

9 min read

What is FICA tax in the US? The Federal Insurance Contributions Act payroll tax funding Social Security (6.2% on wages up to the wage base) and Medicare (1.45% on all wages, plus 0.9% Additional Medicare above income thresholds). Covers the 2025 wage base of $176,100, employer match doubling the total burden to 15.3% up to the wage base, self-employed treatment under SECA (Schedule SE), and brief comparison to India's EPF + ESIC payroll-based social security.

9 min read