HRA Exemption 2025-26: Formula, Limit & Rules (India)

By Tapabrata Biswas · Updated July 8, 2026 · 13 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of the House Rent Allowance (HRA) exemption under Section 10(13A) of the Indian Income Tax Act, 1961, as administered by the Income Tax Department. This post is not tax planning advice. HRA exemption interacts with your specific salary structure, city of residence, actual rent paid, landlord documentation, and regime choice, so the application to your situation needs a Chartered Accountant. Consult a CA before claiming HRA on your ITR or making rental-arrangement decisions with tax implications.

HRA is one of the most-claimed exemptions on Indian salary returns because it can genuinely cut taxable income for renters, sometimes by Rs 2 to 3 lakh a year for senior employees with a high HRA component and high actual rent. The catch is that it runs on a specific three-part formula, needs a documented rent trail, and vanishes entirely under the new tax regime. This post walks through the formula, the metro rules (including a change that starts in FY 2026-27), a fresh worked example, the "is there a limit" question, the documentation, the home-loan and rent-to-parents cases, and where Section 80GG picks up for people who get no HRA.

What is HRA and who can claim it?

House Rent Allowance is a salary component your employer pays specifically to help cover rent, part of which Section 10(13A) lets you exempt from tax if you actually pay rent and do not own the home you live in. It shows up as a line on your salary slip, usually a fixed monthly figure or a percentage of basic pay. Being paid HRA is not the same as getting the exemption. The exemption is a separate calculation under Section 10(13A) and Rule 2A of the Income Tax Rules, 1962, and it only applies when three conditions hold:

- You are salaried and receive an HRA component (the self-employed and salaried people with no HRA use Section 80GG instead, covered below).

- You actually pay rent for the home you live in.

- You do not own that home.

Miss any one and the exemption is zero, even if HRA sits on your payslip. Meet all three and the exempt figure comes out of the Rule 2A formula; whatever it produces is removed from taxable salary and the rest of your HRA is taxed normally.

How is HRA exemption calculated?

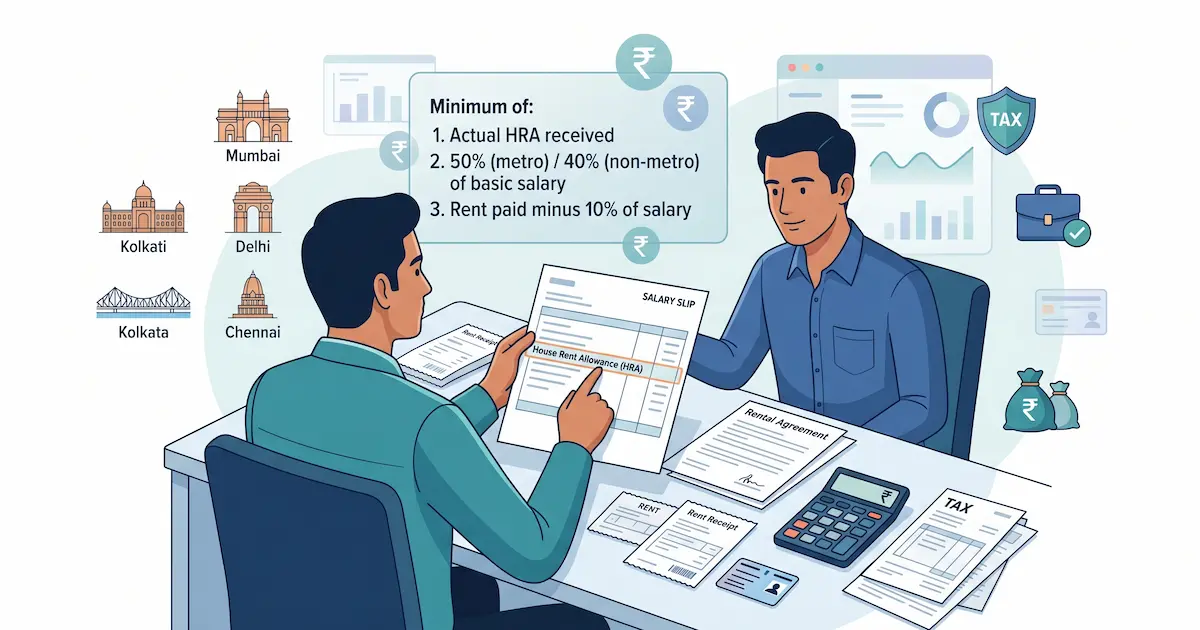

Your exempt HRA is the least of three amounts, defined by Rule 2A. It is not a single percentage or a flat cap; it is whichever of these three works out smallest:

| Component | What it is |

|---|---|

| A | Actual HRA received in the year (the HRA line on your slip times 12) |

| B | 50% of salary if you live in a metro city, or 40% of salary if non-metro |

| C | Actual rent paid in the year minus 10% of salary |

Exempt HRA = the smallest of A, B, and C. Each of the three caps the exemption from a different angle: A stops you exempting more HRA than you were paid, B ties it to a share of salary scaled to city rent norms, and C reflects that rent below 10% of salary is treated as basic living cost rather than a housing burden.

Two precision points that half the popular guides get loose on. First, the "salary" in conditions B and C is basic pay, plus dearness allowance only where it counts toward retirement benefits, plus any commission fixed as a percentage of turnover. Bonus, special allowances, perquisites, and reimbursements are excluded. Second, condition C subtracts 10% of that full salary figure, not 10% of basic alone, though many calculators write it loosely as "10% of basic."

Which cities count as metro for the 50% rate?

For FY 2025-26, the return you file in 2026, only four cities are treated as metro and give the 50% rate: Delhi, Mumbai, Kolkata, and Chennai. Every other city is non-metro at 40%, including several with rents as high as the official four:

- Metro (50% of salary): Delhi, Mumbai, Kolkata, Chennai

- Non-metro (40% of salary): everywhere else, including Bengaluru, Hyderabad, Pune, Ahmedabad, Gurugram, and Noida

The part almost no ranking calculator states cleanly is what happens next year. From FY 2026-27 (income earned on or after 1 April 2026), the government has moved to widen the 50% list to eight cities by adding Bengaluru, Hyderabad, Pune, and Ahmedabad, under the Income-tax Rules 2026 that operationalise the new Income-tax Act, 2025. That change does not touch the return you file in 2026: for FY 2025-26 those four added cities are still non-metro at 40%. Since the exact final-notified position on the eight-city rule was still settling as this was written, treat it as forward guidance and confirm it with a CA before relying on it for FY 2026-27.

One more rule people trip on: the classification follows where you live and work, not your employer's head office. A Chennai-based employee of a Bengaluru company gets the 50% rate for FY 2025-26; a Bengaluru-based employee of a Chennai company gets 40%.

A worked example: Bengaluru, and what changes next year

Meet Rohan, salaried in Bengaluru, renting, with this FY 2025-26 structure:

- Basic salary: Rs 7,20,000 a year (Rs 60,000/month)

- HRA received: Rs 3,60,000 a year (Rs 30,000/month)

- Rent paid: Rs 40,000/month, so Rs 4,80,000 a year

Bengaluru is non-metro for FY 2025-26, so condition B uses 40%:

- A (actual HRA) = Rs 3,60,000

- B (40% of salary) = Rs 2,88,000

- C (rent minus 10% of salary) = 4,80,000 minus 72,000 = Rs 4,08,000

The smallest is B, Rs 2,88,000, so that is Rohan's exempt HRA. The remaining Rs 72,000 of his HRA (3,60,000 minus 2,88,000) is taxable salary.

Now run the same numbers for FY 2026-27, when Bengaluru is set to join the 50% list:

- A = Rs 3,60,000

- B (50% of salary) = Rs 3,60,000

- C = Rs 4,08,000

The smallest is now Rs 3,60,000, so his entire HRA becomes exempt and the taxable portion drops to zero. The city reclassification lifts Rohan's exempt HRA by Rs 72,000, and the actual tax that saves him depends on his slab (roughly Rs 15,000 at a 20% slab, or about Rs 22,000 at 30%). This is exactly why the four-versus-eight-city timing matters, and why running the formula for your own city and year beats trusting a calculator that has hard-coded one list. You can plug your own numbers into our HRA exemption calculator, which shows which of the three conditions caps your exemption. The precise computation for your salary is the kind of calculation a CA runs during ITR preparation.

Is there a maximum HRA exemption limit?

No. There is no fixed rupee ceiling on HRA exemption. People search for "maximum HRA exemption" expecting a single number, and there isn't one. The cap is whichever of the three formula amounts is smallest, which moves with your salary, your rent, and your city. A higher basic lifts condition B, higher rent lifts condition C, but the exemption can never exceed the HRA you actually received (condition A). So the honest answer to "what is the most I can exempt" is: the least of A, B, and C, computed on your own figures.

Can I claim HRA and a home loan together?

Yes, in the old regime you can claim HRA and home-loan tax benefits at the same time, because they run under separate sections. The clean case is common for people who move cities for work: you own a home in one city, claiming interest under Section 24(b) and principal under Section 80C on it, while genuinely renting in your work city and claiming HRA on that rent. Nothing in the law forces you to pick one.

Claiming both in the same city is allowed too, but it invites questions, so you need a genuine reason your owned home is not where you live: it is let out, still under construction, or too far from your workplace to be practical. Keep documentation for that reason. As with everything here, both benefits exist only in the old regime; the new regime disallows HRA and caps the home-loan interest benefit differently.

What documents do you need to claim HRA?

The Income Tax Department expects a paper trail that survives scrutiny years later. Three things:

Rent receipts. Receipts from the landlord showing name, address, rent, property, date, and signature. Receipts are not required where HRA is small (monthly rent up to Rs 3,000 is exempt from the receipt requirement), but above that they are, and payroll teams collect them during the Form 12BB investment-declaration cycle each January to March.

A rent agreement. Not strictly mandatory, but strongly advised, because a claim without one is easier to challenge at assessment. (Note a separate rule people confuse with this: once monthly rent crosses Rs 50,000, the tenant must deduct 2% TDS under Section 194-IB. That is a TDS duty, not a rent-agreement trigger.)

The landlord's PAN, if rent is high enough. Where annual rent to a landlord exceeds Rs 1 lakh, you must report that landlord's PAN (CBDT Circular 8/2013), submitted through Form 12BB, after which it appears on your Form 16. A useful nuance most guides miss: the Rs 1 lakh test is per landlord, not aggregate, so Rs 80,000 to one and Rs 70,000 to another needs neither PAN. If a landlord has no PAN, you file a landlord declaration plus Form 60 instead. Paying rent to parents is allowed if the arrangement is genuine (paid by bank transfer, declared as their rental income), and from FY 2026-27 the rules tighten the disclosure of a family-landlord relationship, so keep it clean and documented.

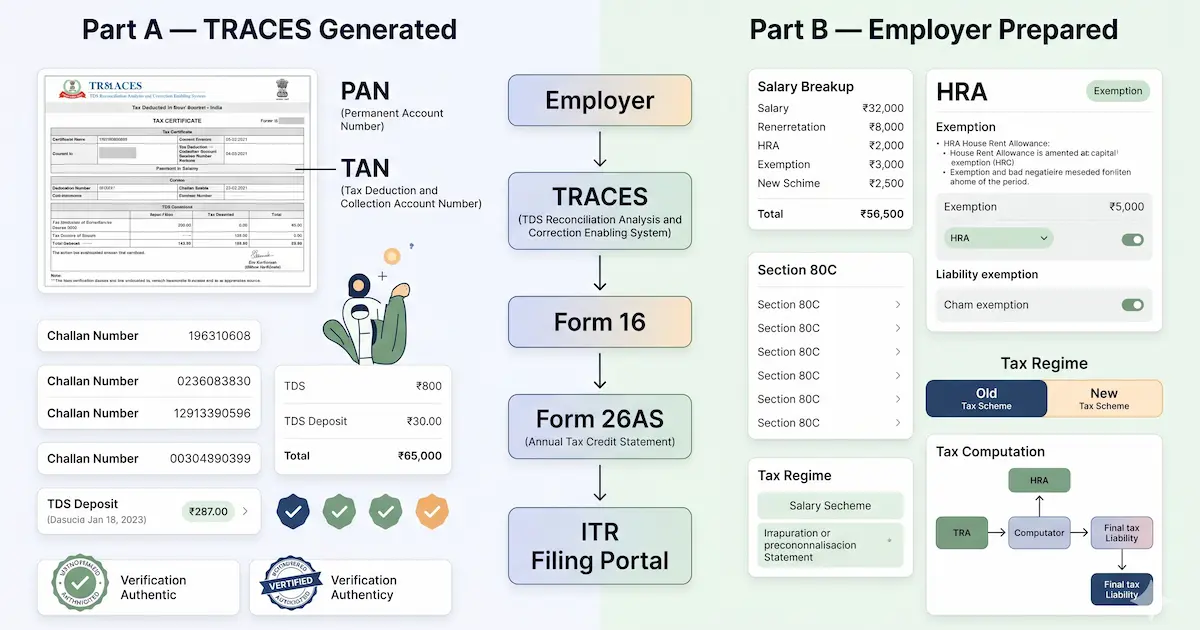

Where your HRA lands on your salary documents, and how the exemption lowers the TDS your employer deducts, is covered in what Form 16 shows and how TDS on salary works.

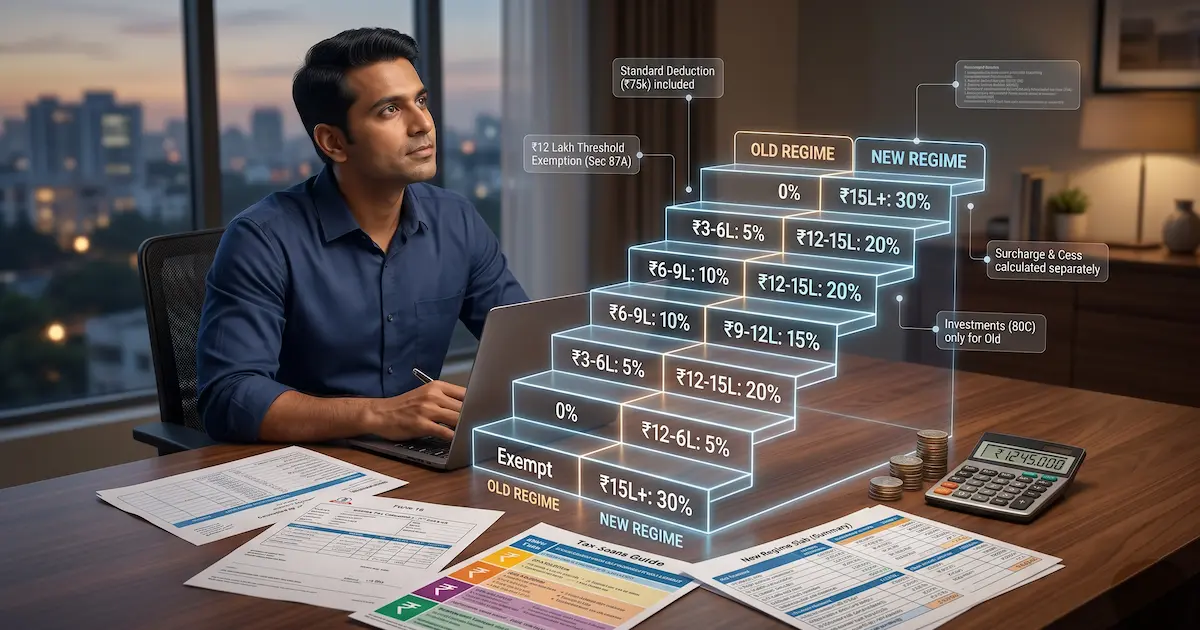

Can you claim HRA under the new tax regime?

No. HRA exemption is an old-regime-only benefit; the new tax regime disallows it. The new regime, default since FY 2023-24, trades away HRA and most other exemptions for lower slab rates, so a renter who wants HRA has to actively choose the old regime when filing. Whether that trade is worth it depends on your full set of deductions, not on HRA alone. We work through the old-versus-new decision with numbers in which tax regime is cheaper for you, and HRA sits alongside other old-regime deductions like Section 80C. The wider salaried-filing walk-through is in our Indian Income Tax Guide for salaried employees, FY 2025-26.

What if your salary has no HRA? Section 80GG

If you pay rent but your salary has no HRA component, or you are self-employed, you cannot use Section 10(13A); you claim rent under Section 80GG instead. The two are mutually exclusive: receive HRA and you are out of 80GG. The 80GG deduction is the least of three amounts: Rs 5,000 a month (Rs 60,000 a year), 25% of your adjusted total income, or rent paid minus 10% of that income. You file Form 10BA to claim it, you must not own a home at your place of work, and, like HRA, it works only in the old regime. Given the search demand around it, Section 80GG deserves its own detailed guide, which is a planned addition; for now, treat this as the pointer for renters who get no HRA.

Common mistakes that get HRA disallowed

Drawing on ITAT (Income Tax Appellate Tribunal) cases over the years, the Department tends to strike down HRA claims for:

- HRA claimed with no provable rent, receipts produced after the fact with no bank-transfer trail

- HRA claimed while living in an owned house, where condition C is zero

- Rent "paid" to family without a genuine transfer trail or matching income declaration by the recipient

- Missing landlord PAN when annual rent to that landlord tops Rs 1 lakh

- Receipts that do not match bank statements, receipts saying Rs 25,000 while only Rs 15,000 a month actually moves

These get flagged by the Department's automated scrutiny selection or during manual review, and the fix when disallowed is back tax plus interest and, in bad cases, a penalty under Section 270A. Claims backed by real bank transfers, valid receipts, landlord PAN above the threshold, and a genuine arrangement carry none of that risk. For anything ambiguous (rent to parents, split rent with a spouse, partial family assistance), confirm the treatment with a CA before you claim.

What this post deliberately does not cover

Three planning questions sit outside this explainer on purpose:

Should you restructure your salary to maximise HRA? Basic-versus-HRA-versus-special-allowance proportions affect PF base, gratuity, and more, so that is a personalised decision that reaches well beyond tax.

Is the old regime worth keeping just for HRA? That is the regime-choice question, and it turns on your whole deduction profile, covered in which tax regime is cheaper for you.

Can a spouse and you split rent and both claim? Legally possible, but both returns must align on the split and it draws scrutiny. Confirm the structure with a CA first.

The structural takeaway: HRA exemption is the least of three amounts under Section 10(13A), needs a documented rent trail and (above Rs 1 lakh annual rent to a landlord) that landlord's PAN, exists only in the old regime, and its exact value for you depends on variables a CA reviews at filing.

Frequently asked questions

How is HRA exemption calculated? The exempt HRA is the least of three amounts under Rule 2A: (a) the actual HRA received in the year, (b) 50% of salary if you live in a metro city or 40% if non-metro, and (c) the rent you paid minus 10% of salary. "Salary" here means basic pay plus dearness allowance that counts toward retirement benefits plus any commission fixed as a percentage of turnover. Whichever of the three is smallest is your exempt HRA; the rest of the HRA you received is taxable.

Which cities are metro cities for the 50% HRA rate? For FY 2025-26 (the return you file in 2026), only four cities are metro for HRA and give the 50% rate: Delhi, Mumbai, Kolkata, and Chennai. Every other city, including Bengaluru, Hyderabad, Pune, Gurugram, and Noida, is non-metro at 40%. From FY 2026-27 (income from 1 April 2026), the government has moved to add Bengaluru, Hyderabad, Pune, and Ahmedabad to the 50% list under the Income-tax Rules 2026; confirm the final notified position with a CA before relying on it.

Is there a maximum limit on HRA exemption? No. There is no fixed rupee cap on HRA exemption. The maximum you can exempt is simply the least of the three formula amounts: actual HRA received, 50% (metro) or 40% (non-metro) of salary, and rent paid minus 10% of salary. Whichever of those three is smallest is both your exemption and its ceiling, so the cap changes with your salary, your rent, and your city.

Can I claim HRA in the new tax regime? No. HRA exemption under Section 10(13A) exists only in the old tax regime. The new regime, which is the default from FY 2023-24, disallows HRA along with most other exemptions and deductions in exchange for lower slab rates. Because the new regime is now the default, a renter who wants to claim HRA must actively opt for the old regime when filing. Which regime is cheaper for you depends on your full deduction profile.

Can I claim HRA and a home loan at the same time? Yes, in the old regime. The cleanest case is owning a home in one city (on which you claim home-loan interest under Section 24(b) and principal under Section 80C) while genuinely renting in another city for work and claiming HRA on that rent. Claiming both in the same city is possible but needs a genuine reason your owned home is not your residence (let out, under construction, or too far from work) plus documentation. HRA and the home-loan deductions run under separate sections, so they do not cancel each other.

Sources

- Income Tax Department of India, Section 10(13A) and Rule 2A, House Rent Allowance Exemption, incometax.gov.in

- Central Board of Direct Taxes (CBDT), Circular No. 8/2013, Landlord PAN Requirement, incometaxindia.gov.in

- Ministry of Finance, Income Tax Act, 1961, Section 10(13A) and Section 80GG, incometaxindia.gov.in/Acts

- Income Tax Department, Form 12BB (investment declaration) and Form 10BA (Section 80GG), incometax.gov.in

- Business Standard, HRA relief expands to 8 cities from FY27 (Income-tax Rules 2026), business-standard.com

- Income Tax Appellate Tribunal (ITAT), Reported cases on HRA disallowance, itat.gov.in

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read

What is Form 16? The TDS certificate Indian employers issue to salaried employees under Section 203 of the Income Tax Act, documenting tax deducted from salary across the financial year. Covers Part A (TRACES-generated, TDS quarter-by-quarter) vs Part B (employer-prepared, salary and deduction breakup), the June 15 issuance deadline, Form 16A for non-salary TDS, how to reconcile Form 16 against Form 26AS, and what to do about mismatches.

9 min read