What Is TDS: How Tax Deducted at Source Works in India Across Salary, Interest, Rent, and Professional Fees

By Tapabrata Biswas · Published May 24, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of Tax Deducted at Source (TDS) as administered by the Income Tax Department under Chapter XVII-B of the Income Tax Act, 1961. This post is not tax filing advice. TDS rates, thresholds, and applicable sections change frequently with each Union Budget; the right TDS treatment for any specific payment depends on the income type, recipient status, PAN availability, and several other variables that only a qualified Chartered Accountant familiar with the situation can correctly assess. Consult a CA for any TDS-related decision affecting your specific tax position.

TDS appears on every salaried Indian's payslip and on every bank-interest credit above ₹50,000 per year — yet the underlying mechanism is poorly understood by most taxpayers. The structural confusion: TDS feels like an extra tax, but it is actually an advance payment of the tax you would owe anyway, deposited with the government on your behalf by the payer. When you file your ITR, you claim credit for TDS already paid and pay only the balance (or receive a refund if TDS exceeded your liability).

This post covers what TDS actually is, the major TDS sections relevant to individuals, the current FY 2025-26 rates and thresholds as notified by the CBDT, the PAN requirement under Section 206AA, Form 26AS reconciliation, and the structural mechanic of how TDS interacts with ITR filing.

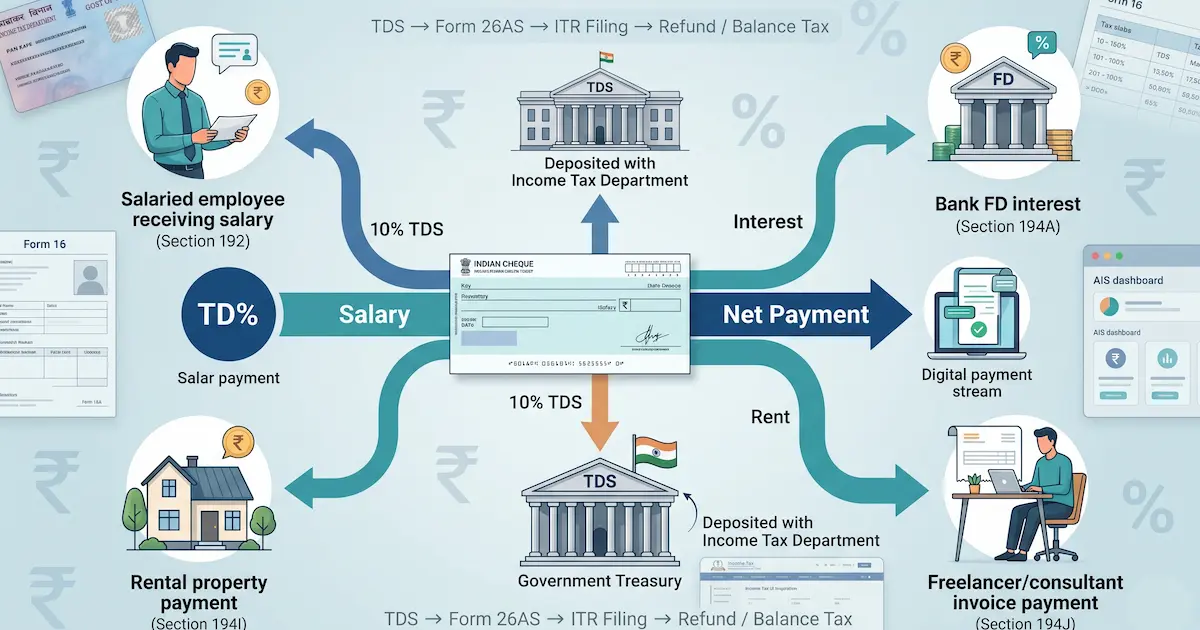

What TDS actually is

Tax Deducted at Source (TDS) is the mechanism where the person paying certain categories of income deducts a specified percentage of the payment as tax before sending the remainder to the recipient, and deposits the deducted amount with the Central Government on the recipient's behalf.

The structural mechanic in three steps:

- Deductor (the payer — employer, bank, tenant, client) calculates TDS at the applicable rate

- Deductor pays the net amount (gross minus TDS) to the deductee (the recipient — employee, depositor, landlord, professional)

- Deductor deposits the TDS amount with the Income Tax Department within prescribed timelines, and the deductee gets credit for it against their annual tax liability

The deductee receives:

- The net amount as cash flow during the year

- A TDS certificate (Form 16 for salary, Form 16A for other payments) showing the amount deducted

- Credit for the TDS in their Form 26AS, which they claim when filing ITR

TDS exists because the Income Tax Department wants tax collected as income is generated, not at year-end. The mechanism shifts the administrative burden of tax collection from millions of individual taxpayers to a smaller number of organised deductors (employers, banks, large businesses), which improves compliance and cash flow.

The provision is governed by Chapter XVII-B of the Income Tax Act, 1961, with individual sections covering different income types.

The major TDS sections for individuals

The most relevant TDS provisions for everyday salaried and self-employed taxpayers:

Section 192 — TDS on Salary

Who deducts: Employer Rate: Applicable income tax slab rate Threshold: No threshold — TDS applies on the full salary Mechanic: Employer estimates the employee's annual tax based on declared income, expected exemptions/deductions (via Form 12BB), and applicable regime; deducts the estimated tax in monthly instalments throughout the year.

This is the TDS most Indians encounter first — the "tax deducted" line on their monthly salary slip. Section 192 differs from other TDS sections in that the rate is the employee's full slab rate (not a flat 10%), and the calculation is updated as the employee submits investment declarations during the financial year.

Section 194A — TDS on Interest (other than securities)

Who deducts: Bank, post office, NBFC, anyone paying interest above thresholds Rate: 10% (20% if no PAN — see Section 206AA below) Threshold (FY 2025-26): ₹50,000 per financial year for individuals, ₹1,00,000 for senior citizens (60+)

This applies primarily to fixed deposit interest. Banks track interest accrued on all your FDs at the same bank and deduct TDS if the aggregate annual interest crosses the threshold. Bank interest below the threshold is still taxable as income — the lack of TDS doesn't mean the income is tax-free, just that the bank isn't pre-collecting on it.

Section 194 — TDS on Dividends

Who deducts: Company paying the dividend Rate: 10% Threshold (FY 2025-26): ₹10,000 per recipient per year

Reintroduced in FY 2020-21 after dividends became taxable in the recipient's hands (previously, companies paid Dividend Distribution Tax and dividends were tax-free for recipients). Mutual fund dividends (now called Income Distribution cum Capital Withdrawal — IDCW — for regulatory reasons) also fall under similar TDS provisions.

Section 194I — TDS on Rent

Who deducts: Tenant (if business/professional) or any person paying rent above threshold Rate: 10% on rent for land/building/furniture, 2% on rent for plant/machinery Threshold (FY 2025-26): ₹2,40,000 annual rent

Applies primarily to commercial leases and high-value residential leases. Salaried individuals paying rent for their own accommodation typically don't deduct TDS unless rent exceeds ₹50,000 per month — in which case Section 194-IB applies (deducting 2% TDS, paid via Form 26QC). The landlord-PAN requirement under Section 194-IB is separate from the HRA exemption landlord-PAN rule under CBDT Circular 8/2013.

Section 194J — TDS on Professional or Technical Fees

Who deducts: Any person paying professional fees, technical services fees, royalty, non-compete fees Rate: 10% (2% for technical services, royalty, and FTS) Threshold (FY 2025-26): ₹30,000 per financial year per recipient per type

Applies to consultants, freelancers, doctors, lawyers, chartered accountants, and other professionals. The ₹30,000 threshold means small one-off payments don't trigger TDS, but ongoing professional engagements typically cross the threshold within months.

Section 194C — TDS on Contractor Payments

Who deducts: Any person making contractor payments Rate: 1% for individual contractor, 2% for company/firm Threshold (FY 2025-26): ₹30,000 per single payment, OR ₹1,00,000 aggregate per financial year

Covers payments to construction contractors, transporters, catering services, advertising agencies, and similar service providers.

The PAN requirement — Section 206AA

If the recipient (deductee) does not provide their PAN to the deductor, Section 206AA mandates higher TDS rates — the higher of:

- The rate specified by the relevant TDS section

- The rate(s) in force

- 20%

In practice, this means most income types where the deductor cannot verify the PAN get 20% TDS instead of the 10% that would otherwise apply.

The provision was introduced to incentivise PAN compliance and prevent fictitious tax-credit claims. Without PAN, the deductor cannot reliably route the TDS credit to the correct taxpayer, so the higher rate creates a financial disincentive for non-compliance.

NRIs without PAN can sometimes provide Form 60 (a declaration of not having PAN) for certain transactions, but the practical reality is that almost every Indian taxpayer must provide PAN to anyone deducting TDS on their behalf to avoid the 20% rate.

Form 26AS and the AIS — how TDS reconciles to ITR

The Income Tax Department maintains a Form 26AS (and the more recent Annual Information Statement, AIS) under each taxpayer's PAN. This consolidated statement shows:

- All TDS deducted across the financial year from any source

- Tax Collected at Source (TCS) where applicable

- Advance tax and self-assessment tax paid

- Refunds processed

- Specified financial transactions reported by banks and other entities

The taxpayer accesses Form 26AS via the Income Tax e-filing portal under their login. When filing the annual ITR, they claim credit for the TDS shown in Form 26AS against their computed annual tax liability.

The reconciliation arithmetic:

| Scenario | Treatment |

|---|---|

| TDS > computed tax liability | Excess is refunded by the Income Tax Department (typically 30-60 days post ITR processing) |

| TDS = computed tax liability | No additional payment, no refund |

| TDS < computed tax liability | Taxpayer pays the balance + applicable interest under Section 234B and Section 234C as self-assessment tax |

Mismatches between Form 16/16A and Form 26AS are a common source of ITR filing complications — the deductor may have deducted the tax but failed to deposit it correctly, or may have used the wrong PAN. Reconciling such mismatches requires going back to the deductor and is the kind of situation where a Chartered Accountant's help becomes essential.

A worked example — a salaried employee with bank interest

A salaried employee earning ₹15 lakh annual salary in Mumbai, with ₹60,000 of bank FD interest in FY 2025-26. New regime, no other exemptions claimed beyond standard deduction.

Step 1 — TDS deducted by employer (Section 192)

Estimated annual tax under new regime on ₹14,25,000 taxable salary (after ₹75,000 standard deduction): roughly ₹97,500 including cess (per the worked example in income tax slab India explained). Employer deducts this in 12 monthly instalments → roughly ₹8,125/month TDS on salary.

Step 2 — TDS deducted by bank (Section 194A)

Bank FD interest of ₹60,000 exceeds the ₹50,000 threshold. Bank deducts 10% TDS on the entire ₹60,000 → ₹6,000 TDS.

Step 3 — Form 26AS shows

| Source | Section | Amount deducted |

|---|---|---|

| Employer | 192 | ₹97,500 |

| Bank | 194A | ₹6,000 |

| Total TDS | ₹1,03,500 |

Step 4 — ITR filing

Total income: ₹14,25,000 (salary after standard deduction) + ₹60,000 (FD interest) = ₹14,85,000

Approximate tax on ₹14,85,000 under new regime (slab calculation + cess): roughly ₹1,06,000

TDS already paid: ₹1,03,500

Balance payable: ~₹2,500 (paid as self-assessment tax before ITR filing).

This is illustrative. Your actual numbers — and the exact section-by-section TDS treatment for your situation — require individual computation by a qualified CA, particularly if your income includes multiple sources, capital gains, foreign income, or other complications.

For how TDS reconciliation fits the full salaried filing flow — Form 16, regime choice, and the July 31 deadline — see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

What this post deliberately does not cover

Three out-of-scope topics, kept out because they're advisory rather than definitional:

1. "How do I reduce my TDS deduction?" — Submitting Form 15G/15H to avoid bank-interest TDS, deferring income to a lower-slab year, or restructuring how payments are received are tax-planning decisions specific to each taxpayer's situation and warrant a CA's review.

2. "What do I do if my deductor hasn't deposited my TDS?" — Specific compliance situations (employer not depositing salary TDS, mismatched Form 26AS, defective ITR returns from prior years) require case-by-case advice that's outside the scope of a definitional explainer. Consult a CA.

3. "How is TDS treated for NRIs and foreign payments?" — TDS on NRI income (Section 195), royalty payments to non-residents, and similar cross-border TDS scenarios have different rates, treaty benefits under DTAA, and procedural requirements that need specialised tax advice.

The structural takeaway: TDS is an advance-payment mechanism under Chapter XVII-B of the Income Tax Act. Different sections govern different income types with their own rates and thresholds. Form 26AS consolidates everything under your PAN, and the annual ITR reconciles TDS already paid against your total computed liability. For specific situations and edge cases, a Chartered Accountant is the right professional — see also what is Form 16 India for the TDS certificate that documents your salary TDS.

Frequently asked questions

What is TDS in simple terms? TDS (Tax Deducted at Source) is the mechanism in Indian tax law where the person paying certain types of income — salary, interest, rent, professional fees, contractor payments, dividends, and others — deducts a percentage of the payment as tax before sending the remainder to the recipient, then deposits the deducted amount with the Income Tax Department on the recipient's behalf. The recipient gets credit for this TDS when filing their annual ITR. TDS exists because the government wants to collect tax as income is generated rather than waiting for the year-end ITR filing — it improves cash flow for the government and reduces the risk of unpaid tax. TDS is governed by Chapter XVII-B of the Income Tax Act, 1961 and detailed in Sections 192 through 196D plus Section 206 series.

What are the main TDS sections and their thresholds? The most relevant TDS sections for individual taxpayers are: Section 192 (TDS on salary — deducted by employer at applicable slab rate, no threshold), Section 194A (TDS on interest from banks — 10% above ₹50,000 per financial year for individuals, ₹1 lakh for senior citizens), Section 194 (TDS on dividends — 10% above ₹10,000), Section 194I (TDS on rent — 10% if annual rent above ₹2.4 lakh on land/building), Section 194J (TDS on professional or technical fees — 10% above ₹30,000), and Section 194C (TDS on contractor payments — 1% for individuals, 2% for companies, above ₹30,000 single payment or ₹1 lakh aggregate per year). Each section has its own rates and thresholds, and the rates can change with each Union Budget — always confirm against the Income Tax Department's current notifications.

Why is TDS deducted at 20% if I don't provide my PAN? Section 206AA of the Income Tax Act mandates higher TDS rates when the recipient does not furnish their PAN to the deductor. The higher rate is the higher of (a) the rate specified by the relevant TDS section, (b) the rate or rates in force, or (c) 20%. In practice, this typically means 20% TDS instead of 10% for most income types where the deductor cannot verify the recipient's PAN. The provision exists to incentivise PAN compliance and prevent fictitious tax-credit claims. NRIs and others without PAN can submit Form 60 in specific cases, but the practical effect is that almost all Indian taxpayers should provide PAN to anyone deducting TDS on their behalf to avoid the higher rate.

How do I reconcile TDS deducted against my actual tax liability? Through Form 26AS and the Annual Information Statement (AIS), accessed via the Income Tax e-filing portal. Form 26AS is the consolidated tax statement showing all TDS deducted from your income across the financial year — TDS by employer, banks, tenants, and any other deductors all appear here under your PAN. The AIS provides similar information with additional financial transaction data. When you file your ITR, you claim credit for the TDS shown in Form 26AS against your total computed tax liability. If TDS exceeds your liability, the excess is refunded (typically within 30-60 days of ITR processing). If TDS is less than your liability, you pay the balance plus any applicable interest under Sections 234B and 234C. Mismatches between Form 16/16A and Form 26AS need to be reconciled with the deductor before filing — consult a Chartered Accountant for the specific mechanics.

Sources

- Income Tax Department of India, Chapter XVII-B — Deduction at Source — incometax.gov.in

- Central Board of Direct Taxes (CBDT), TDS Rates and Thresholds for FY 2025-26 — incometaxindia.gov.in

- Income Tax Department, Form 26AS — Annual Tax Statement — incometax.gov.in/iec/foportal

- Income Tax Department, Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) — incometax.gov.in

- Tax Information Network (TIN-NSDL), TDS Operating Procedures and Challan Submission — tin-nsdl.com

- Ministry of Finance, Income Tax Act, 1961 — Sections 192-206 — incometaxindia.gov.in/Acts

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

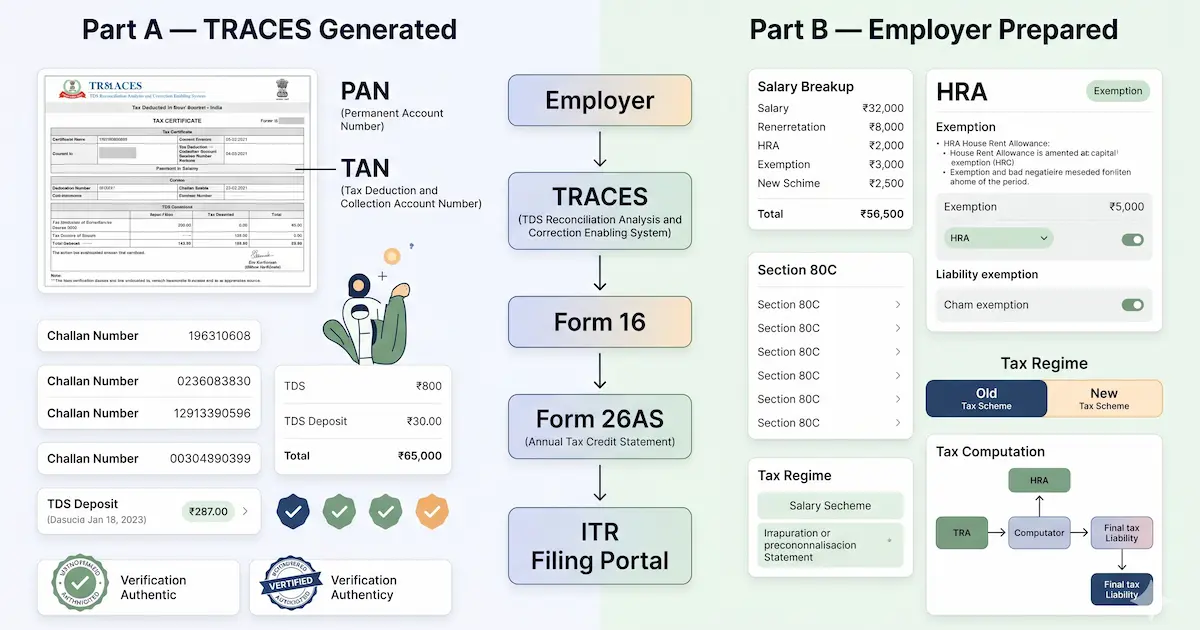

What is Form 16? The TDS certificate Indian employers issue to salaried employees under Section 203 of the Income Tax Act, documenting tax deducted from salary across the financial year. Covers Part A (TRACES-generated, TDS quarter-by-quarter) vs Part B (employer-prepared, salary and deduction breakup), the June 15 issuance deadline, Form 16A for non-salary TDS, how to reconcile Form 16 against Form 26AS, and what to do about mismatches.

9 min read

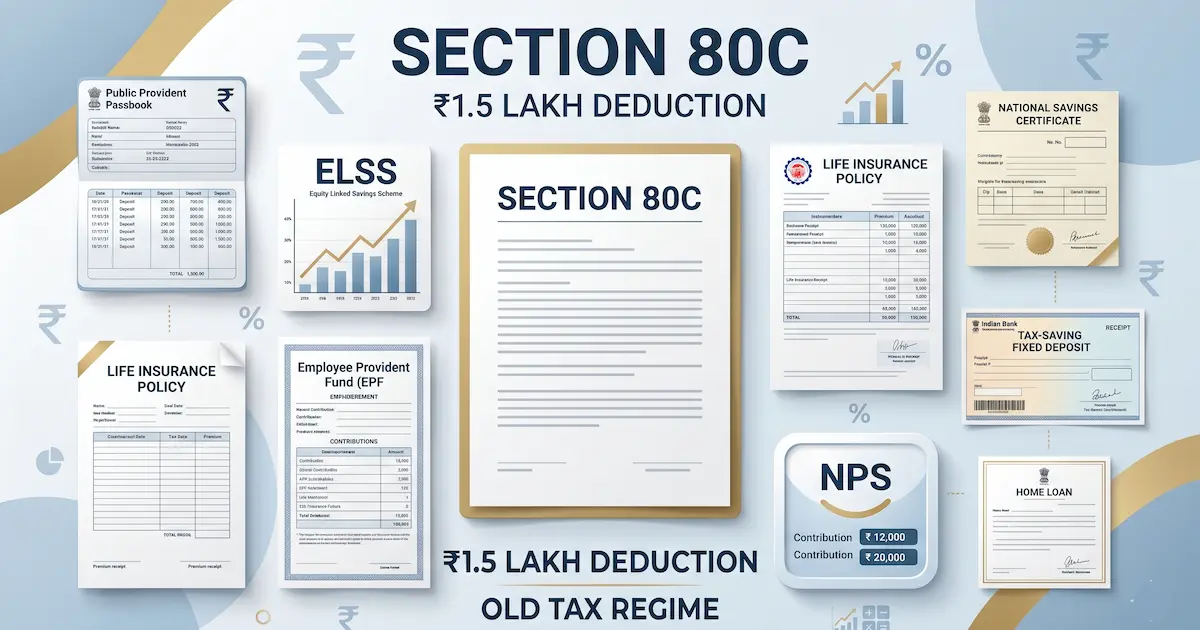

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read