What Is Section 80C? ₹1.5 Lakh Deduction List (2026)

By Tapabrata Biswas · Updated July 8, 2026 · 13 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of Section 80C of the Indian Income Tax Act, 1961, as administered by the Income Tax Department. This post is not tax planning advice. Section 80C interacts with regime choice, total income, other available deductions, and individual investment goals, and the application to your specific situation requires a Chartered Accountant. For investment-product selection within 80C-eligible instruments, consult a SEBI-registered investment adviser.

Most Section 80C guides bury the part that matters most in 2026: as of FY 2025-26 (AY 2026-27), the new tax regime is the default, and Section 80C does not exist under it. You can claim the famous ₹1.5 lakh only if you actively choose the old regime, which a growing share of taxpayers no longer do. So before treating 80C as a box to max out, it is worth knowing what it actually is, what qualifies, and whether the old regime it lives in is still the better deal for you in 2026.

This post covers what Section 80C is, whether you can use it in the new regime, the full eligible-investment list with the ₹1.5 lakh limit, how much tax it really saves, the extra ₹50,000 via 80CCD(1B), and how to claim it when you file.

What is Section 80C?

Section 80C of the Income Tax Act, 1961 is a deduction that lets an individual or Hindu Undivided Family reduce taxable income by up to ₹1.5 lakh in a financial year by putting money into instruments the Act specifies. It is the most-discussed provision in Indian personal tax, because that ₹1.5 lakh is available to almost every salaried filer who opts for the old regime.

A deduction is not the same as a rebate. A deduction cuts the income you are taxed on, so the money you save equals the amount claimed times your slab rate. A rebate, like Section 87A, cuts the tax itself. Because 80C is a deduction, its value rises with your slab: the same ₹1.5 lakh is worth far more at 30% than at 5%.

The cap is combined, not per instrument. If you put ₹1 lakh in PPF, ₹50,000 in ELSS, and ₹40,000 into a life-insurance premium in the same year, you still claim only ₹1.5 lakh, not ₹1.9 lakh. And only individuals and HUFs qualify, never companies or firms. The ₹1.5 lakh figure has been frozen since FY 2014-15, when it was raised from ₹1 lakh.

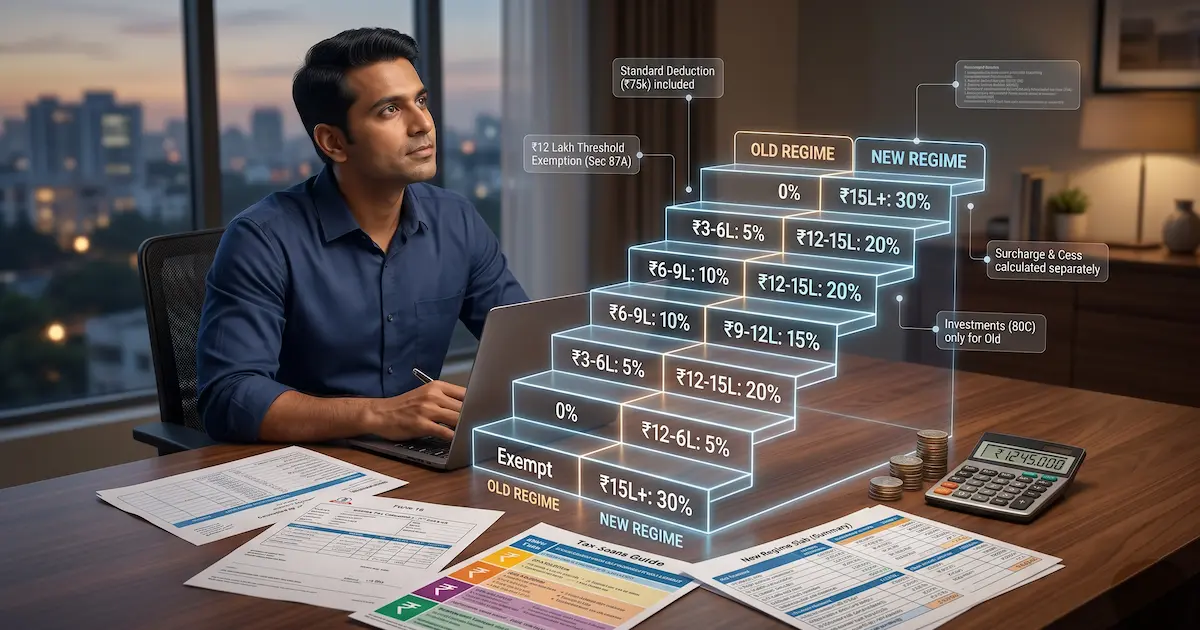

Can you claim Section 80C under the new tax regime?

No. Section 80C is unavailable under the new tax regime, so you can claim it only if you opt for the old regime. The Income Tax Department states that under the new regime (Section 115BAC), Chapter VI-A deductions cannot be claimed except 80CCD(2), 80CCH, and 80JJAA. That rules out 80C, along with HRA, home-loan interest, and most other familiar deductions.

The new regime has been the default since FY 2023-24, which means the switch is on you: if you do nothing, you are taxed under the new regime and your 80C investments earn no deduction. To use 80C, a salaried filer selects the old regime inside the ITR by the due date, while anyone with business or professional income must file Form 10-IEA first. Whether that switch is worth it is a slab-level question, and we work it through in how the old and new regime slabs compare.

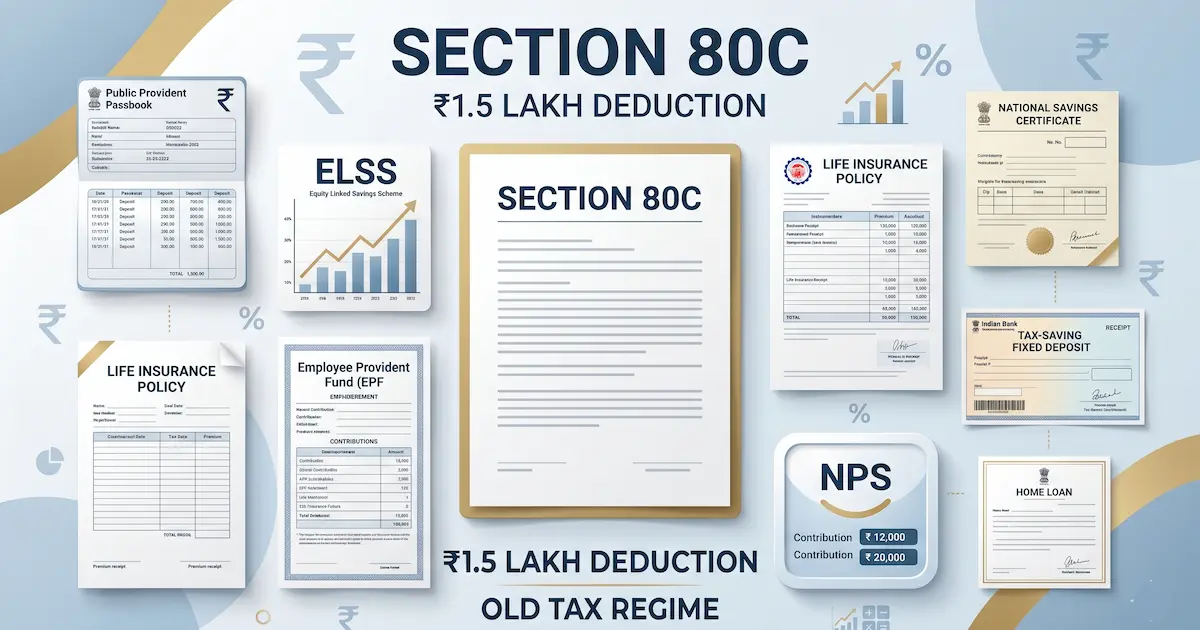

What investments and expenses qualify for Section 80C?

The Section 80C eligible list covers a fixed set of investments and expenses, from PPF and ELSS to home-loan principal and children's tuition fees, all sharing the single ₹1.5 lakh ceiling. The interest rates below are for the July to September 2026 quarter and are reset quarterly by the Ministry of Finance, so confirm the current figure before you invest.

| Instrument | Type | Lock-in | Rate / return |

|---|---|---|---|

| Public Provident Fund (PPF) | Government scheme | 15 years | 7.1% tax-free |

| Employees' Provident Fund (EPF), your contribution | Workplace scheme | Until retirement | 8.25% (FY 2024-25) |

| Equity Linked Savings Scheme (ELSS) | Equity mutual fund | 3 years | Market-linked |

| Sukanya Samriddhi Yojana (SSY) | Government, girl child | 21 years | 8.2% tax-free |

| National Savings Certificate (NSC) | Post office | 5 years | 7.7% taxable |

| Tax-saving fixed deposit | Bank FD | 5 years | 6.5% to 7.5% taxable |

| Senior Citizens Savings Scheme (SCSS) | Government, age 60+ | 5 years | 8.2% taxable |

| Life insurance premium | Insurance | Policy term | Varies |

| ULIP | Insurance + investment | 5 years | Market-linked |

| Home-loan principal repayment | Mortgage | Loan tenure | Not applicable |

| Stamp duty and registration | Property purchase | Year of purchase | Not applicable |

| Tuition fees (up to 2 children) | Education | Annual | Not applicable |

| NPS Tier 1, via Section 80CCD(1) | Pension | Until age 60 | Market-linked |

A few catches worth knowing. ELSS has the shortest lock-in of any 80C option at three years and is the only equity route. A life-insurance premium qualifies only up to 10% of the sum assured for policies bought on or after 1 April 2012, so a small policy with a fat premium does not fully count. Only your own EPF contribution counts; the employer's does not. And each government scheme has its own mechanics, covered in our explainers on PPF and EPF.

What is the maximum Section 80C deduction?

The maximum Section 80C deduction is ₹1,50,000 per financial year, combined across 80C, 80CCC, and 80CCD(1) under Section 80CCE. Section 80CCC covers pension-plan premiums and 80CCD(1) covers your own NPS contribution, and all three draw from the same ₹1.5 lakh pool. You cannot stack them to reach ₹4.5 lakh.

That ceiling has not changed since FY 2014-15, more than a decade of frozen limit while incomes and prices rose, which quietly shrinks the real value of the deduction every year. The one legitimate way past ₹1.5 lakh is Section 80CCD(1B), covered below.

How much tax does Section 80C actually save you?

Section 80C saves you tax equal to ₹1.5 lakh times your marginal slab rate, not a flat ₹1.5 lakh, because it lowers taxable income rather than the tax itself. This is the point most people miss, and it is why the deduction is worth wildly different amounts to different earners.

Work a full ₹1.5 lakh claim through the old-regime slabs, adding the 4% health and education cess:

| Your top slab | Tax saved on a full ₹1.5 lakh 80C claim |

|---|---|

| 5% | about ₹7,800 (₹7,500 plus cess) |

| 20% | about ₹31,200 (₹30,000 plus cess) |

| 30% | about ₹46,800 (₹45,000 plus cess) |

So a senior manager in the 30% slab gets roughly six times the benefit a junior colleague in the 5% slab gets from the identical investment. If your income is low enough to sit in the 5% band, locking ₹1.5 lakh into a 15-year PPF to save ₹7,800 is a very different decision from a high earner saving ₹46,800, which is exactly the kind of trade-off worth checking before you commit.

Section 80C vs 80CCD(1B): how to reach ₹2 lakh

Section 80CCD(1B) is a separate ₹50,000 deduction for your own NPS Tier 1 contribution, on top of the ₹1.5 lakh under 80C, which is why the two together allow up to ₹2 lakh under the old regime. The most common mistake in the whole 80C conversation is folding this ₹50,000 inside the ₹1.5 lakh. It is not inside; it is extra.

There is a third piece that behaves differently. Section 80CCD(2), the deduction for your employer's NPS contribution, sits outside the ₹1.5 lakh cap and is the one NPS deduction the new regime keeps. Its limit was widened for FY 2025-26 to 14% of salary (basic plus dearness allowance) for all employees under the new regime, up from the old-regime 10% that applies to private-sector staff. A lot of guides still quote the old 10% figure, so if your employer offers an NPS contribution, this is the rare deduction worth having in either regime. The mechanics of NPS itself are in our NPS explainer.

How to claim Section 80C in your ITR

You claim Section 80C either by declaring your investments to your employer during the year, so it reflects in your Form 16 and your TDS drops, or by entering the total yourself under Chapter VI-A when you file your return. Both routes need the same thing: proof, and the money actually invested inside the financial year.

Two timing rules trip people up. The investment must be made on or before 31 March of the financial year you are claiming for, not before the July filing deadline, so a PPF deposit or ELSS purchase in April counts toward the next year instead. And you must be under the old regime for the claim to register at all, which for salaried filers is a toggle inside the ITR and for business income is Form 10-IEA. Keep the receipts, PPF passbook entries, ELSS statements, insurance premium receipts, and tuition-fee receipts, because while you do not upload them with the return, the department can ask for them later.

Does Section 80C still make sense in 2026?

Honestly, for a lot of salaried people, no longer by default. The new regime now zeroes tax on income up to ₹12 lakh through an enhanced Section 87A rebate, gives a ₹75,000 standard deduction, and charges lower rates, all without asking you to lock money away. For someone who was only investing in 80C to save tax, and who fits inside the new regime's generous band, chasing the old regime just to claim ₹1.5 lakh can leave them worse off overall.

That does not make 80C useless. It still wins for people with large old-regime deductions stacked together, a home-loan interest claim under Section 24, a big HRA exemption, and a full 80C, whose total often beats the new regime's lower rates. The break-even is a genuine calculation on your own numbers, which is why it belongs with the regime comparison in the income tax slab guide and, for your specific case, with a CA. My own view is simply that "max out your 80C" is advice from the old default, and in 2026 that reflex deserves a fresh look.

What this guide does not cover

This guide explains what Section 80C is and how to claim it; it is not personalised tax or investment advice. It does not tell you which regime to pick (that is a slab-level computation on your numbers, covered in the slab guide and best confirmed with a Chartered Accountant), which specific instrument to buy (a product choice for a SEBI-registered adviser), or how to build a whole tax plan. Tax rules change with every Union Budget, and the ₹1.5 lakh limit, stable since 2014, is not guaranteed forever, so always check the Income Tax Department's current notifications before claiming. For how 80C fits the wider system, see our tax concepts overview.

Frequently asked questions

Is Section 80C applicable in the new tax regime? No. Under the new tax regime (Section 115BAC), which has been the default since FY 2023-24, Section 80C is not available, along with most other Chapter VI-A deductions such as HRA and home-loan interest. The Income Tax Department confirms only 80CCD(2), 80CCH, and 80JJAA survive in the new regime. To claim 80C you must actively opt for the old regime, which for salaried filers means selecting it in the ITR, and for those with business income means filing Form 10-IEA by the due date.

What is the maximum deduction under Section 80C? ₹1,50,000 per financial year, and this cap has been unchanged since FY 2014-15. It is a combined ceiling across Section 80C, 80CCC, and 80CCD(1) under Section 80CCE, not ₹1.5 lakh per instrument, so ₹1.5 lakh into PPF alone already exhausts it. You can go higher only through Section 80CCD(1B), which adds a separate ₹50,000 for your own NPS Tier 1 contribution, taking the old-regime personal maximum to ₹2,00,000.

What investments and expenses qualify for Section 80C? The eligible list set by the Income Tax Act includes PPF, EPF (your own contribution), ELSS mutual funds, life insurance premiums, NSC, Sukanya Samriddhi Yojana, 5-year tax-saving bank FDs, SCSS, ULIPs, NPS Tier 1 (via 80CCD(1)), home-loan principal repayment, stamp duty and registration charges, and tuition fees for up to two children. Each carries a different lock-in and return profile, and life-insurance premiums qualify only up to 10% of the sum assured for policies issued on or after 1 April 2012.

What is the difference between Section 80C and 80CCD(1B)? Section 80C is a ₹1.5 lakh umbrella covering many instruments, while Section 80CCD(1B) is a separate ₹50,000 slot exclusively for your own NPS Tier 1 contribution, sitting on top of the ₹1.5 lakh. The common error is folding that ₹50,000 inside the ₹1.5 lakh; it is actually additional, so the two together allow ₹2 lakh under the old regime. Both are old-regime-only.

How much tax does Section 80C actually save? 80C reduces your taxable income by up to ₹1.5 lakh, not your tax by ₹1.5 lakh, so the saving equals ₹1.5 lakh times your marginal slab rate plus 4% cess. A full claim saves roughly ₹7,500 in the 5% slab, ₹30,000 in the 20% slab, and ₹46,800 in the 30% slab. That is why 80C is worth far more to a high earner than to someone near the bottom of the old-regime slabs.

Who can claim Section 80C? Only individuals and Hindu Undivided Families (HUFs) can claim Section 80C. Companies, partnership firms, and LLPs cannot. Within that, a salaried person, a self-employed professional, and an HUF can each claim up to ₹1.5 lakh on their own eligible investments and expenses, provided they file under the old tax regime.

In summary

Section 80C is a ₹1.5 lakh deduction that trims your taxable income through a fixed list of investments and expenses, from PPF and ELSS to home-loan principal and tuition fees, with 80CCD(1B) adding ₹50,000 more for NPS. Its real value is your slab rate times the claim, so ₹46,800 saved at 30% down to ₹7,800 at 5%, and its whole existence now hangs on one prior choice: opting into the old regime.

That choice is the part 2026 changed. With the new regime as the default and zero tax up to ₹12 lakh, 80C is no longer the automatic win it was for a decade. It still pays off for filers stacking large deductions together, but for many the honest move is to run both regimes on their own numbers first, then decide whether 80C is worth the lock-in at all before maxing it out of habit.

Sources

- Income Tax Department of India, New vs Old Tax Regime FAQs (Section 115BAC), incometax.gov.in

- Central Board of Direct Taxes, Income Tax Act, 1961: Sections 80C, 80CCC, 80CCD, 80CCE, incometaxindia.gov.in

- Press Information Bureau, Ministry of Finance, Budget 2025: rebate and new-regime relief up to ₹12 lakh, pib.gov.in

- Pension Fund Regulatory and Development Authority, NPS tax benefits (80CCD), pfrda.org.in

- Income Tax Department, Form 10-IEA (opting for the old regime), incometax.gov.in

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

What is NPS (National Pension System)? Tier I vs Tier II, equity/debt/government asset choices, Section 80CCD(1B) extra ₹50K deduction, and the 60% lump sum + 40% annuity rule at retirement.

9 min read

What are the foundational tax concepts every Indian and US taxpayer should understand? This pillar page synthesizes 10 definitional explainers covering income tax slabs (India new + old regime), Section 80C, HRA exemption, TDS, Form 16, capital gains, marginal vs effective tax rates, deductions vs credits, standard vs itemized deduction, GST, and FICA. Research-led definitions, not tax planning advice. For your specific situation, consult a Chartered Accountant (India) or Certified Public Accountant (US).

12 min read