What Is Employee Provident Fund (EPF): How Contributions, Interest, and Withdrawals Work

By Tapabrata Biswas · Updated May 27, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

EPFO declared 8.25% as the EPF interest rate for FY 2024-25 — the highest among India's government-backed small-savings instruments, edging out even Sukanya Samriddhi Yojana's 8.2% and well above PPF's 7.1%. For a salaried employee in the formal sector earning ₹60,000 basic salary, the combined 24% monthly contribution (12% employee + 12% employer) sends roughly ₹14,400 into the retirement system every month — about ₹9,400 to EPF proper and ₹5,000 to the linked Employees' Pension Scheme. Compounded over a 35-year career at 8.25%, that monthly contribution builds a corpus of approximately ₹4.2 crore at retirement.

This post covers what EPF actually is, how the employee and employer contributions are structured and split between EPF and EPS, the partial-withdrawal rules for specific life events, and the EEE tax treatment that requires 5 years of continuous service.

What EPF actually is

EPF full form: Employees' Provident Fund (commonly written as Employee Provident Fund). It is a retirement savings scheme established under the Employees' Provident Funds and Miscellaneous Provisions Act of 1952 and administered by the Employees' Provident Fund Organisation (EPFO), a statutory body under the Ministry of Labour & Employment, Government of India. The 'PF' line item that appears on Indian salary pay stubs refers to this scheme.

Structurally, EPF is India's primary payroll-deducted retirement contribution — analogous to the US FICA tax (Social Security + Medicare) but with a critical difference: FICA funds defined-benefit national pensions (employee never sees a personal account balance), while EPF accumulates as an individual account that the employee owns and can withdraw at retirement.

Three structural features distinguish EPF from PPF and other voluntary small-savings instruments:

Mandatory for covered employees. Every establishment employing 20 or more workers is required to enroll its employees in EPF. Employees earning a monthly basic salary up to ₹15,000 are mandatorily covered. Higher-earning employees can opt in (and most do, since the employer contribution and tax treatment are highly favourable). This is different from PPF, which is purely voluntary.

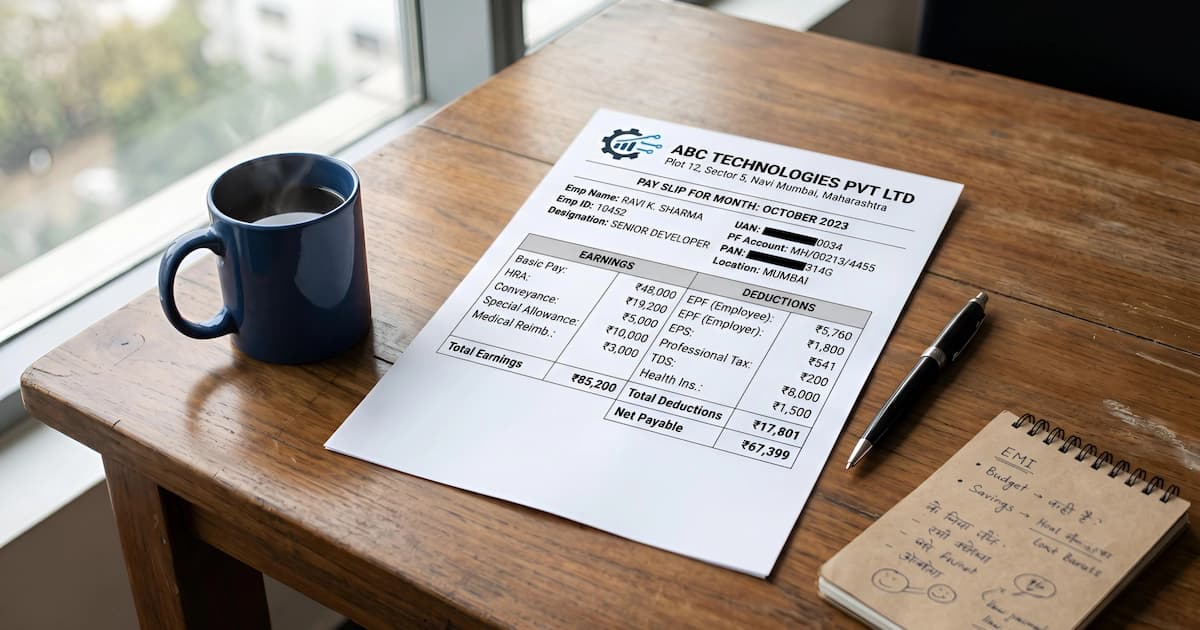

Dual contribution from employee and employer. Both contribute 12% of basic salary plus dearness allowance every month. The combined 24% deduction is one of the largest single forced-savings mechanisms in Indian personal finance — and the employer's portion is genuinely additional compensation that employees don't always realise they're earning.

Linked to EPS (pension) and EDLI (life insurance). The employer's 12% contribution is actually split: 8.33% goes to the Employees' Pension Scheme (capped at ₹15,000 basic salary), and 3.67% goes to EPF. The Employees' Deposit-Linked Insurance Scheme (EDLI) adds another 0.5% from the employer for a small life insurance benefit. EPF, EPS, and EDLI together form a packaged social-security framework.

How EPF contributions are structured

The 24% combined monthly contribution breaks down like this:

| Component | Source | Percentage | Goes to |

|---|---|---|---|

| Employee EPF contribution | Employee salary | 12% of basic + DA | EPF account |

| Employer EPF contribution | Employer | 3.67% of basic + DA | EPF account |

| Employer EPS contribution | Employer | 8.33% of basic + DA, capped at ₹1,250/month | EPS pension fund |

| EDLI (insurance) | Employer | 0.5% of basic + DA, capped at ₹75/month | Insurance benefit |

| EPF admin charges | Employer | 0.5% of basic + DA | EPFO administration |

A worked example. An employee with basic + DA of ₹50,000/month:

- Employee EPF: ₹6,000/month (12%) → into EPF account

- Employer EPF: ₹1,835/month (3.67%) → into EPF account

- Employer EPS: ₹1,250/month (8.33% of ₹15,000 cap) → into EPS pension

- Total monthly EPF contribution: ₹7,835 plus ₹1,250 to pension

- Total annual EPF contribution: ₹94,020 plus ₹15,000 EPS

For employees earning above ₹15,000 basic, the EPS contribution is capped at ₹1,250/month. The "excess" employer contribution (which would have been 8.33% of higher basic) instead flows into the EPF account. This is why higher-earners actually see a larger proportion of their employer contribution in EPF.

For the underlying mechanics of how this affects the take-home pay, see gross vs net income and how to read a pay stub — both Pillar 6 explainers that map directly to where EPF shows up on monthly compensation.

The Voluntary Provident Fund (VPF) option

Beyond the mandatory 12% employee contribution, employees can contribute additional amounts to EPF voluntarily — known as Voluntary Provident Fund (VPF). The VPF contribution earns the same EPF interest rate (currently 8.25%) and receives the same tax treatment as the regular EPF contribution.

There is no employer matching on VPF — the additional contribution is entirely from the employee's salary. There is also no statutory limit on VPF — employees can contribute up to 100% of their basic + DA as VPF, on top of the mandatory 12%.

VPF is one of the highest-yielding fixed-income options available to salaried Indians: 8.25% guaranteed, government-backed, EEE tax treatment, and the convenience of being a payroll deduction. Many salaried professionals use VPF as a higher-yielding alternative to bank fixed deposits for long-term saving.

How EPF interest works

EPF interest is declared annually by the EPFO Central Board of Trustees and notified by the Ministry of Labour after Ministry of Finance concurrence. The rate for FY 2024-25 was 8.25%.

The interest calculation has a specific mechanic worth understanding:

- The interest is calculated monthly on the running balance

- It is credited annually at the end of the financial year (March 31)

- Withdrawals or transfers during the year stop interest accrual on the withdrawn portion from the month of withdrawal

Historical EPF rates have ranged from 8.10% (FY 2022-23) to 8.75% (FY 2014-15 onwards) over the past decade. The trend has been a gradual decline matching the broader fall in Indian government bond yields, but EPF has consistently remained the highest-yielding small-savings option — historically because the larger contribution base allows EPFO to invest the corpus across equities, government securities, and corporate bonds with somewhat higher returns than a pure government-securities-backed scheme.

EPF withdrawal rules

EPF is not a fully locked instrument — partial withdrawals are permitted for specific life events, with each having its own eligibility window:

| Purpose | Minimum service | Withdrawal cap |

|---|---|---|

| Marriage (self / children / siblings) | 7 years | Up to 50% of employee's share + interest |

| Higher education (self / children) | 7 years | Up to 50% of employee's share + interest |

| Purchase of plot for house | 5 years | Up to 24 months of basic + DA, or actual plot cost, whichever is lower |

| Purchase / construction of house | 5 years | Up to 36 months of basic + DA, or actual cost, whichever is lower |

| Home loan repayment | 10 years | Up to 36 months of basic + DA |

| Renovation of existing house | 10 years (after 5 years of house ownership) | Up to 12 months of basic + DA |

| Medical emergency | None | 6 months of basic + DA or employee's share, whichever lower |

| Pre-retirement (age 54+) | None | Up to 90% of total EPF balance |

| Unemployment | 2 months of joblessness | Up to 75% initially, balance after 2 more months |

Full withdrawal is permitted at retirement (age 58) or after 2 months of being out of EPF-covered employment without joining another covered employer.

Job transfers don't trigger withdrawal. When changing jobs, the EPF balance can be transferred to the new employer's EPF account through the Universal Account Number (UAN) framework. Transferring (rather than withdrawing) preserves the continuous-service clock used for tax purposes.

EEE tax treatment — conditional on 5 years of service

EPF qualifies for EEE treatment but only if the employee has completed 5 years of continuous service:

| Stage | Treatment when 5+ years service | Treatment under 5 years service |

|---|---|---|

| Contribution | Section 80C deduction up to ₹1.5 lakh/year (shared with other 80C) | Same deduction available; lost if withdrawn early |

| Interest accrual | Tax-free during holding period | Becomes taxable when withdrawn |

| Withdrawal | Fully tax-free | Employer share taxed as salary; employee share loses 80C; interest taxed |

The EPF deduction is the largest single component of most salaried Indians' Section 80C usage — ₹6,000/month × 12 = ₹72,000/year for an employee with ₹50,000 basic salary fills nearly half the ₹1.5 lakh 80C cap before any voluntary instruments (PPF, ELSS, life insurance premiums, etc.) are added. The deduction reduces taxable income, which then flows through the Indian income tax slab structure — old regime takes the 80C deduction, new regime does not. Both employee and employer EPF contributions appear in Part B of the annual Form 16 under "Deductions u/s 80C" and "Salary as per provisions of Section 17(1)" respectively.

The "5 years of continuous service" rule has a specific definition: the 5 years can span multiple employers IF the EPF balance has been transferred (not withdrawn) at each job change. This is why transferring EPF when switching jobs — rather than withdrawing — is generally the better choice for anyone who might end up with under 5 years at a single employer.

A specific exception: if employment ends due to ill-health, employer business closure, or any reason beyond the employee's control, EPF withdrawal is tax-free regardless of years of service.

For voluntary employee contributions exceeding ₹2.5 lakh per year (introduced in Budget 2021), the interest on the excess portion is taxable. This affects high-earners using VPF aggressively but not the typical salaried employee.

EPF vs PPF — the practical comparison

Most salaried Indians have EPF mandatorily AND can voluntarily open a PPF. The two run in parallel and serve different needs:

| Factor | EPF | PPF |

|---|---|---|

| Current rate (Q1 2026) | 8.25% (FY 24-25) | 7.1% |

| Eligibility | Salaried employees in covered firms | Any Indian resident |

| Contribution | Mandatory 12% of basic + DA | Voluntary, ₹500 to ₹1.5 lakh/year |

| Employer matching | Yes — 12% match | No |

| Tax deduction | Section 80C (employee share) | Section 80C |

| Tax treatment | EEE (5+ years service) | EEE always |

| Withdrawal flexibility | Multiple life-event triggers | Partial from year 7 only |

| Job change handling | Transferable via UAN | N/A (single account) |

For salaried employees, EPF is the foundation — the rate is higher, the employer contribution adds genuine wealth, and the multiple withdrawal triggers provide more flexibility than PPF's restrictive partial-withdrawal rule. PPF complements EPF as a parallel tax-saving instrument and remains useful for the non-salaried population (freelancers, business owners, homemakers) who don't have EPF access.

What experts say

The EPFO portal is the authoritative source for all EPF rules, member services, UAN registration, and online withdrawal procedures. The Ministry of Labour & Employment publishes the annual EPF rate notifications and policy updates.

The Income Tax Department's Section 10(11) and Rule 8 of Part A of the Fourth Schedule cover the tax treatment of EPF withdrawal. The Pension Fund Regulatory and Development Authority (PFRDA) publishes comparisons between EPS, NPS, and broader retirement-planning frameworks.

For the broader Pillar 8 context covering related government-backed savings, see what is Public Provident Fund (PPF) (the universal voluntary alternative) and what is Sukanya Samriddhi Yojana (the girl-child-specific scheme). For how EPF shows up in your monthly take-home pay, see gross vs net income and how to read a pay stub.

Frequently asked questions

What is the current EPF interest rate in 2026? EPFO declared 8.25% as the EPF interest rate for FY 2024-25, the highest small-savings rate among government schemes. The rate is recommended by the Central Board of Trustees of EPFO and notified by the Ministry of Labour & Employment after concurrence from the Ministry of Finance. Interest is credited to the member's account once per year based on the opening balance plus monthly contributions. EPF rates have ranged from 8.10% to 8.75% over the past decade — historically the highest among small-savings instruments because of the larger contribution base.

How much do I contribute to EPF from my salary? An employee contributes 12% of their basic salary plus dearness allowance (DA) to EPF every month. The employer contributes an equal 12% — but split: 8.33% goes to the Employees' Pension Scheme (EPS) capped at ₹15,000 basic, and the remaining 3.67% goes to EPF. So out of the combined 24% contribution, roughly 15.67% (employee's 12% + employer's 3.67%) lands in the EPF corpus and 8.33% (capped) goes to the pension component. This deduction appears as 'EPF' or 'PF' on monthly pay stubs.

When can I withdraw my EPF balance? Full EPF withdrawal is permitted at retirement (age 58) or two months after leaving employment without joining another EPF-covered employer. Partial withdrawals are permitted earlier for specific purposes — house purchase or construction (after 5 years of service), marriage of self/children/siblings (after 7 years), higher education of children, medical emergencies, and a few other categories. Each purpose has its own eligibility window, contribution-percentage cap, and required documentation under the EPF Composite Claim Form.

Is EPF withdrawal taxable? EPF qualifies for EEE (Exempt-Exempt-Exempt) treatment if the employee has completed 5 years of continuous service. Contributions are deductible under Section 80C up to ₹1.5 lakh per year (shared with other 80C instruments). Interest credited annually is tax-free during the holding period. Withdrawal after 5 years of service is fully tax-free. Withdrawal before 5 years is taxable — the employer's contribution portion is taxed as salary income, the employee's contribution loses the original 80C deduction, and accumulated interest becomes taxable. Switching jobs and transferring EPF (rather than withdrawing) preserves the continuous-service clock.

What is the full form of EPF? EPF stands for Employees' Provident Fund (sometimes written as Employee Provident Fund). It is a mandatory retirement savings scheme administered by the Employees' Provident Fund Organisation (EPFO) under the Ministry of Labour & Employment, Government of India. The 'PF' you see deducted from your monthly salary on the pay stub refers to this scheme. The scheme was established by the Employees' Provident Funds and Miscellaneous Provisions Act of 1952 and is among the largest social-security frameworks for salaried Indians.

How can I check my EPF balance online?

Four primary ways to check EPF balance: (1) EPFO Member e-SEWA portal at unifiedportal-mem.epfindia.gov.in — log in with your Universal Account Number (UAN) and password to see full passbook, (2) UMANG app (the Government of India's unified mobile app) — register with UAN and view balance and passbook, (3) missed call to 9966044425 from the registered mobile number — EPFO sends an SMS with the latest balance, (4) SMS — send EPFOHO UAN ENG to 7738299899 from the registered mobile (replace ENG with HIN/MAR/PUN/etc. for regional languages). All four methods require the UAN to be activated and linked to the registered mobile number.

In summary

EPF is the mandatory workplace retirement savings scheme for salaried employees in Indian establishments with 20+ workers, paying 8.25% interest (FY 2024-25) with a dual 12% + 12% employee-and-employer contribution. The employer's 12% is split between EPF (3.67%) and the Employees' Pension Scheme (8.33% capped at ₹15,000 basic). For a typical salaried employee, EPF is the largest single source of forced long-term savings — and the EEE tax treatment (after 5 years of continuous service) makes it the highest after-tax return available among fixed-income options for the salaried population.

The Voluntary Provident Fund (VPF) extension allows employees to contribute additional amounts at the same EPF rate, often beating bank fixed deposits significantly after tax. The multiple partial-withdrawal triggers for marriage, education, house purchase, medical emergencies, and pre-retirement provide more flexibility than PPF's restrictive Year 7+ partial-withdrawal rule. The key discipline: when changing jobs, always transfer the EPF balance to the new employer rather than withdrawing — the continuous-service clock for the EEE tax treatment is preserved only through transfers.

The next read in this pillar covers the National Pension System (NPS) — the voluntary retirement product designed to supplement EPF for higher-income workers and provide retirement coverage for non-salaried Indians. For broader Pillar 8 context, see Public Provident Fund (PPF) and Sukanya Samriddhi Yojana.

For how EPF compares with PPF, NPS and every other government scheme at a glance, see our Indian government savings schemes overview.

Sources

- Employees' Provident Fund Organisation (EPFO), Member Services and Scheme Documents — epfindia.gov.in

- Ministry of Labour & Employment, EPF Rate Notifications and Policy — labour.gov.in

- Ministry of Finance, Department of Economic Affairs — dea.gov.in

- Income Tax Department of India, Section 10(11), Rule 8 of Part A of Fourth Schedule — incometax.gov.in

- Pension Fund Regulatory and Development Authority (PFRDA), EPS vs NPS Comparisons — pfrda.org.in

You might also like

PPF pays 7.1% for Jul-Sep 2026, unchanged since 2020. See the Rs 500 to Rs 1.5 lakh limits, EEE tax, 15-year lock-in, withdrawal rules and a maturity example.

13 min read

Difference between gross and net income, in plain English. What gets deducted, why the gap exists, and which number to budget against in real life.

7 min read

How to read a pay stub: a plain-English walkthrough of every line item, from gross pay to deductions to net take-home, plus the year-to-date totals that matter at tax time.

8 min read