What Is PPF (Public Provident Fund)? 7.1% Rate, EEE Tax

By Tapabrata Biswas · Updated July 9, 2026 · 13 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

The Public Provident Fund pays 7.1% a year for the July to September 2026 quarter, a rate the Ministry of Finance has now held unchanged since 1 April 2020, across nine straight quarters. At the maximum Rs 1.5 lakh a year for the full 15-year lock-in, a single PPF account compounds to about Rs 40.68 lakh at maturity, and every rupee of it is tax-free under the EEE treatment. A sovereign-guaranteed return, no tax on the interest or the maturity, and a partial-withdrawal window that opens in year 7: that mix is why PPF is one of India's most-used long-term savings accounts.

This covers what PPF is, the current rate and the deposit-timing quirk that quietly changes your interest, how to open an account, the withdrawal and loan rules, the EEE tax treatment, what happens at the 15-year mark, and a worked example of how Rs 1.5 lakh a year compounds. It is educational, not investment advice; whether PPF suits your goals and tax regime is a call a fee-only adviser or CA can run on your own numbers.

What is PPF?

The Public Provident Fund is a long-term, government-backed savings scheme, introduced in India in 1968, that pays a fixed quarterly-set interest rate with full tax exemption and a 15-year lock-in. It runs under the National Savings Institute, is administered by the Ministry of Finance's Department of Economic Affairs, and is operated through India Post and most banks (SBI, ICICI, HDFC, PNB, Bank of Baroda, Axis, Kotak, and others).

Three features set it apart from an ordinary savings account or fixed deposit. First, the return is a government-guaranteed rate set quarterly by the Ministry of Finance, not by any bank or market. Second, the 15-year lock-in commits your money for the long haul, which rules it out as an emergency fund (that job belongs to a liquid account, covered in what is an emergency fund) but is exactly what lets the compounding stack up. Third, its EEE tax status exempts the money going in, the interest growing inside, and the amount coming out, a triple exemption only a handful of Indian instruments get.

PPF has no exact US equivalent. Its EEE treatment is actually more generous than a Roth IRA, which is funded with already-taxed money, or a 401(k), which is taxed on the way out. PPF is the rare account taxed at none of the three stages.

Who can open a PPF account?

Only a resident Indian individual can open a PPF account, one per person, and neither NRIs nor Hindu Undivided Families can open a new one.

| Eligible | Not eligible |

|---|---|

| Resident Indian individuals | Non-Resident Indians (cannot open new) |

| A guardian, on behalf of a minor child | Hindu Undivided Families (HUFs) |

| One account per person across all banks and post offices | Joint accounts |

Two nuances the rankers often blur. A parent or guardian can open an account for a minor, but the combined deposit across your own account and the minor's cannot cross Rs 1.5 lakh in a year. And on NRIs: if you opened a PPF while resident and later moved abroad, the account can run to its 15-year maturity with deposits allowed, though it cannot be extended past 15 years. The February 2018 proposal to force NRIs to close early was placed in abeyance, so despite what some pages still claim, existing accounts are not being shut at the old 4% Post Office Savings rate.

What is the current PPF interest rate?

PPF pays 7.1% per year for the July to September 2026 quarter (Q2 FY 2026-27), which the Ministry of Finance retained in its notification dated 30 June 2026. The rate is reviewed every quarter and has sat at 7.1% since 1 April 2020, nine consecutive quarters unchanged and one of the steadiest runs the scheme has seen. Historically it ran much higher, touching 12% in the late 1980s, and has drifted down as government bond yields fell.

Interest is calculated monthly but credited once a year, in March, on the lowest balance in the account between the 5th and the last day of each month. That rule creates a deposit-timing quirk seasoned PPF holders use deliberately:

Put money in before the 5th of the month and it earns interest for that whole month. Put the same money in on the 6th and that month earns nothing. On a Rs 1.5 lakh lump sum the gap is about Rs 888 of interest for a single year (roughly one month's interest at 7.1% on Rs 1.5 lakh). Small in one year, but a saver who always deposits by 5 April instead of late April captures an extra month of compounding every year for 15 years. The clean move is a single lump sum in the first week of April.

Interest compounds annually, not quarterly like a bank savings account, so each year's interest joins the principal and the next year is figured on the larger base. The mechanics are in what is compound interest.

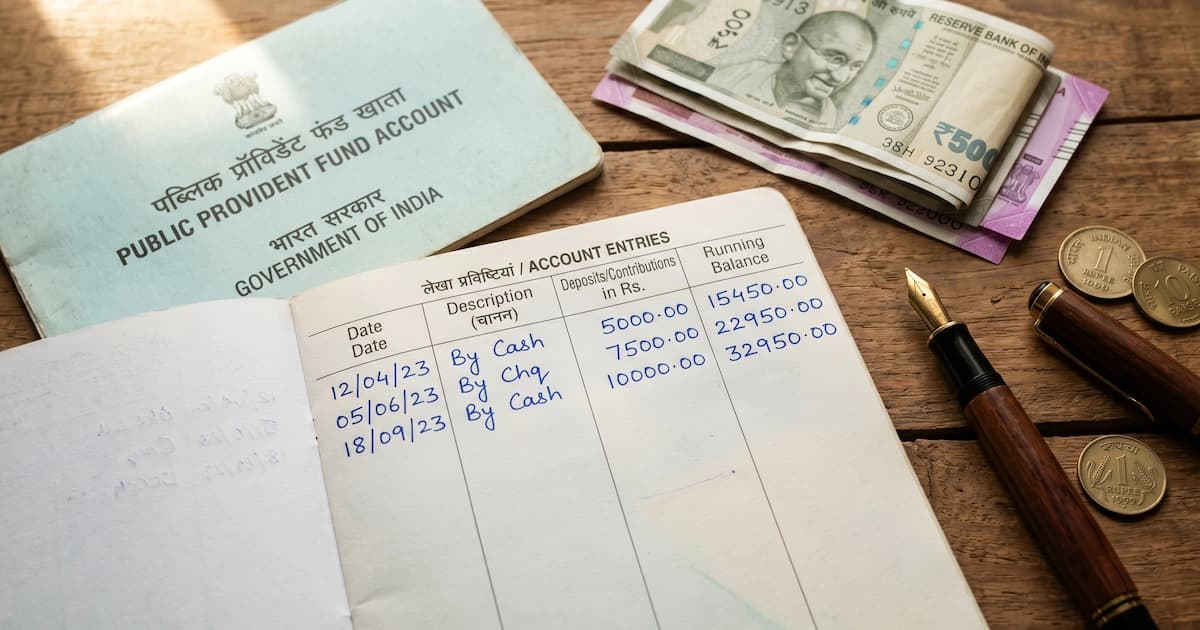

A worked example: Rs 1.5 lakh a year for 15 years

Deposit the maximum Rs 1.5 lakh every year for 15 years at 7.1%, and the account matures at about Rs 40.68 lakh, fully tax-free. Here is how the balance builds:

| Year | Annual deposit | Year-end balance |

|---|---|---|

| 1 | Rs 1,50,000 | Rs 1,60,650 |

| 5 | Rs 1,50,000 | Rs 9,28,470 |

| 10 | Rs 1,50,000 | Rs 22,32,440 |

| 15 (maturity) | Rs 1,50,000 | Rs 40,68,209 |

You put in Rs 22.5 lakh over the 15 years and the interest adds about Rs 18.18 lakh, roughly 81% of what you contributed, none of it taxed. That gap is compounding: in year 1 the 7.1% is figured on Rs 1.5 lakh, and by year 15 it is figured on a balance that has been growing the entire time.

Scale it down and the multiplier holds. Rs 50,000 a year for 15 years at 7.1% totals Rs 7.5 lakh of deposits and matures near Rs 13.56 lakh, about Rs 6 lakh of it tax-free interest. To run your own figures, including 20-year or 25-year extensions, use our PPF Maturity Calculator.

How do I open a PPF account?

You can open a PPF account at any post office or most banks, and increasingly online through your bank's net banking, with just PAN, Aadhaar, a photo, and Rs 500 to activate it.

The three routes:

- At a bank. If you have a savings account with net banking at SBI, HDFC, ICICI, Axis, and similar, you can usually open a PPF entirely online in a few minutes under the investments or small-savings menu. Otherwise, a branch visit with the form does it.

- At a post office. You can download and fill Form A online, but the post office generally needs you to visit once to open the account. After that, deposits go in through the India Post Payment Bank (IPPB) app.

- For a minor. A parent or guardian opens and runs it, and you will need the child's age proof (birth certificate or Aadhaar) alongside your own KYC.

The documents are the standard set: PAN, Aadhaar as identity and address proof, a passport-size photo, and the account-opening form. If your Aadhaar is linked to your mobile, e-KYC can skip the paperwork. Fund it with at least Rs 500 to start, and keep at least Rs 500 going in each financial year to keep it active.

Can I withdraw from PPF before 15 years?

PPF is locked for 15 years, but it allows one partial withdrawal a year from the 7th financial year, a loan from years 3 to 6, and full premature closure only in three specific situations. This is the part most guides get slightly wrong, so here is the precise version.

Partial withdrawal, from year 7. Starting in the 7th financial year, you can make one withdrawal per year, capped at the lower of two figures: 50% of the balance at the end of the 4th preceding financial year, or 50% of the balance at the end of the immediately preceding year. Most competitor pages quote only the second half of that rule; the "whichever is lower" condition is the accurate one. For an account opened in FY 2020-21, the first eligible year is FY 2027-28. If the balance was Rs 6 lakh at the end of FY 2023-24 and Rs 15 lakh at the end of FY 2026-27, the cap is Rs 3 lakh (50% of the lower Rs 6 lakh). You file Form C to withdraw.

Loan against the balance, years 3 to 6. Between the 3rd and 6th financial years you can borrow up to 25% of the balance at the end of the second preceding year. The loan costs 1% above the prevailing PPF rate, so 8.1% at today's 7.1%, and must be repaid within 36 months. Miss that window and the penal rate jumps to 6% above the PPF rate on the unpaid amount, a detail most loan explainers leave out.

Premature closure, after 5 years. Full early closure is allowed only for a serious medical emergency of the holder or a dependent, higher education of the holder or a child, or a change to NRI status. Even then it carries a 1% penalty: the account is repaid at 1% below every rate it earned since opening.

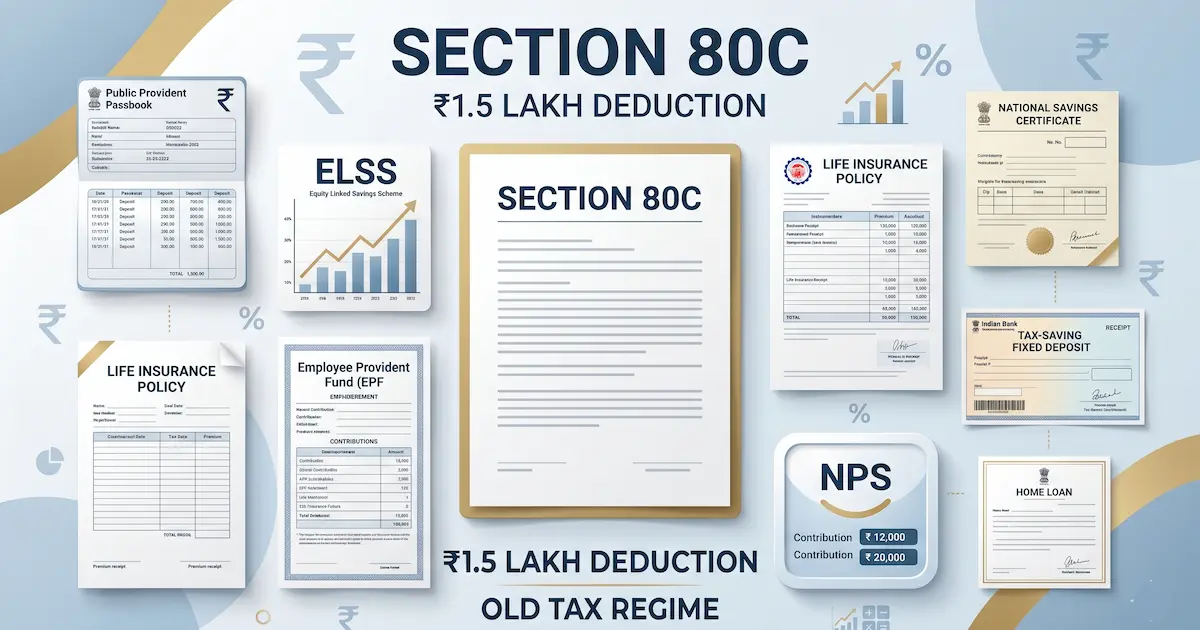

What are the PPF tax benefits?

PPF has EEE (Exempt-Exempt-Exempt) tax treatment, one of the most generous in the Indian tax code, exempting the contribution, the interest, and the maturity.

| Stage | Treatment | Reference |

|---|---|---|

| Contribution | Deductible up to Rs 1.5 lakh a year, old regime only | Section 80C |

| Interest | Fully exempt, no upper limit | Section 10(11) |

| Maturity | Principal and all interest tax-free | Section 10(11) |

The one caveat that has become the most important is the regime. The Section 80C deduction works only under the old tax regime. The new regime, now the default from FY 2023-24, does not allow 80C, so a PPF deposit still earns tax-free interest but no longer cuts your taxable income unless you have opted for the old regime. And the Rs 1.5 lakh 80C ceiling is shared across EPF, ELSS, life insurance, home-loan principal, and more, so PPF competes with them for the cap; the full Section 80C deduction list breaks down what shares it.

The exemption is what makes PPF beat a taxable fixed deposit. For someone in the 30% slab, a tax-free 7.1% is roughly a 10.1% pre-tax FD, because the FD's interest is taxed at the slab rate while PPF's is not.

What happens when PPF matures at 15 years?

At maturity you can withdraw the whole tax-free corpus, or extend the account in 5-year blocks, with or without fresh deposits. The three options:

- Close and withdraw everything, the full Rs 40.68 lakh in the worked example, tax-free.

- Extend without fresh contributions. This is the default if you do nothing. The balance keeps earning the prevailing rate, you make no new deposits, and you can withdraw any amount once a year with no 50% cap.

- Extend with fresh contributions. Keep depositing up to Rs 1.5 lakh a year and keep the 80C benefit. Withdrawals here are capped at 60% of the balance that stood at the start of the extension, spread across the whole 5-year block, one a year.

The trap worth flagging: to extend with contributions you must file Form H within one year of the maturity date. Miss that window and keep depositing anyway, and those deposits are treated as irregular and earn no interest at all. It is the most expensive mistake at the 15-year mark. Extensions renew in 5-year blocks with no published limit, which is why many holders treat PPF as a permanent tax-free compounding account.

PPF vs NPS, ELSS, and a tax-saver FD

PPF is the guaranteed, fully-tax-free, 15-year option among the common Section 80C choices; the others trade safety for higher potential returns or shorter lock-ins.

| Scheme | Return | Lock-in | Tax on gains | Risk |

|---|---|---|---|---|

| PPF | 7.1% fixed | 15 years (partial from yr 7) | Fully exempt (EEE) | None (sovereign) |

| NPS | Market-linked | Till age 60 | Extra Rs 50K under 80CCD(1B); annuity taxed | Moderate |

| ELSS | Market equity | 3 years (shortest) | LTCG taxed above the annual exemption | High |

| Tax-saver FD | ~6.5% to 7% | 5 years | Interest fully taxable | None |

There is no single winner; the fit depends on your horizon, risk appetite, and regime. If you want a market-linked retirement corpus with an extra Rs 50,000 deduction and can lock money till 60, the National Pension System (NPS) is the sibling to weigh against PPF. If a 3-year lock-in and equity upside suit you better, ELSS sits at the other end of the same 80C shelf.

What PPF is good for, and what it is not

PPF fits a specific job. It suits long-horizon goals 15 years or more away (a child's higher education, a retirement supplement, or a house down payment when the timeline is long), old-regime taxpayers wanting the cleanest possible tax treatment, and conservative savers who want a risk-free, guaranteed slice inside a wider portfolio.

It does not fit an emergency fund (locked for 15 years; see how to build an emergency fund), goals under 5 years, or an investor chasing higher growth, since equity funds have historically returned around 10% to 14% over the long run against PPF's 7.1%, with far more short-term swing. As a core Section 80C instrument, PPF also appears in the old-regime deduction stack in our Indian Income Tax Guide for salaried employees, FY 2025-26.

What this post does not cover

This explains the PPF scheme and its rules; it is not a recommendation to open one or a comparison verdict on where your Section 80C money should go. It does not model your personal regime choice (old versus new), which decides whether the 80C deduction is even available to you, and it does not cover bank-specific online steps, which vary. For a plan matched to your goals, income, and tax regime, a fee-only investment adviser or a CA is the right person to ask.

Frequently asked questions

What is the current PPF interest rate? The PPF interest rate is 7.1% per year for the July to September 2026 quarter (Q2 FY 2026-27), compounded annually. The Ministry of Finance retained it at that level in its notification dated 30 June 2026, and it has stayed at 7.1% since 1 April 2020, one of the longest stable runs in the scheme's history. Interest is figured on the lowest balance in the account between the 5th and the last day of each month, so depositing before the 5th earns that whole month's interest.

Is PPF interest taxable? No. PPF has EEE (Exempt-Exempt-Exempt) tax status. The interest credited each year is fully exempt under Section 10(11) of the Income Tax Act with no upper limit, the maturity amount is tax-free, and the contribution is deductible under Section 80C up to Rs 1.5 lakh a year. The one catch is that the 80C deduction works only under the old tax regime; the new regime, now the default, does not allow it.

How much can I deposit in PPF per year? The minimum is Rs 500 and the maximum is Rs 1.5 lakh per financial year, counted across all PPF accounts in your name (including any you run for a minor child). Deposits can be a single lump sum or spread through the year in multiples of Rs 50. Anything above Rs 1.5 lakh earns no interest and gets no 80C benefit. Miss the Rs 500 minimum and the account goes dormant; revive it by paying Rs 500 for each missed year plus a Rs 50 penalty per defaulted year.

Can I withdraw from PPF before 15 years? Partly. One partial withdrawal a year is allowed from the 7th financial year, capped at the lower of 50% of the balance at the end of the 4th preceding year or the immediately preceding year. A loan against the balance is available from years 3 to 6. Full premature closure is allowed only after 5 years and only for a serious medical emergency, higher education, or a change to NRI status, and it carries a 1% interest penalty across the account's life.

Can an NRI open a PPF account? No, a Non-Resident Indian cannot open a new PPF account, and neither can a Hindu Undivided Family. But if you opened a PPF while resident and later became an NRI, that account can continue to its 15-year maturity with fresh deposits allowed; it simply cannot be extended beyond 15 years. The February 2018 notice that proposed forcing NRIs to close early was placed in abeyance, so existing accounts run their full term.

The bottom line

PPF is a 15-year, government-backed savings scheme paying 7.1% for the July to September 2026 quarter, with deposits of Rs 500 to Rs 1.5 lakh a year and EEE tax treatment that exempts the contribution (under old-regime Section 80C), the interest, and the maturity. Maxed out for the full term, one account grows to about Rs 40.68 lakh, roughly Rs 18.18 lakh of it tax-free interest.

The 15-year lock-in is the real trade-off, softened by the year-7 partial withdrawal and the year 3-to-6 loan, but PPF is a long-horizon account and no substitute for an emergency fund. One small habit pays off more than most: deposit by the 5th of April each year, and you buy yourself an extra month of tax-free compounding, every year, for 15 years.

For the girl-child version that works like PPF but pays 8.2%, see Sukanya Samriddhi Yojana; for the workplace sibling at 8.25%, see Employee Provident Fund (EPF). For every current scheme rate side by side, see our Indian government savings schemes overview.

Sources

- India Post, Public Provident Fund (PPF), indiapost.gov.in/Financial/Pages/Content/PPF.aspx

- Ministry of Finance, Department of Economic Affairs, Small Savings Schemes quarterly rate notification (Jul-Sep 2026, dated 30 June 2026), dea.gov.in/budget-division/475

- National Savings Institute, PPF scheme and current rate table, nsiindia.gov.in

- Income Tax Department of India, Section 10(11) and Section 80C, incometax.gov.in

- Reserve Bank of India, Master Direction on Small Savings, rbi.org.in

You might also like

What is Sukanya Samriddhi Yojana? The 8.2% interest rate, eligibility (girl child below 10), 15-year contribution + 21-year maturity, partial withdrawal at 18, and EEE tax treatment explained with worked example.

9 min read

What is EPF (Employee Provident Fund)? The 8.25% interest rate, mandatory 12%+12% employee/employer contribution, EPS split, withdrawal rules, and tax treatment explained for salaried Indian workers.

9 min read

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read