What Is National Pension System (NPS): How It Works, Asset Choices, and Tax Benefits

By Tapabrata Biswas · Published May 20, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

The National Pension System lets a single subscriber legally reduce taxable income by up to ₹2 lakh per year — ₹1.5 lakh under Section 80C plus an additional ₹50,000 under Section 80CCD(1B) that no other instrument provides. Layered on top of that, employer contributions to corporate NPS are deductible from the employee's taxable income up to 10% of basic salary (14% for central government employees) with no upper cap. The combination of these three deductions, plus market-linked returns averaging 9-13% historically for equity-heavy schemes, makes NPS one of the most tax-efficient retirement vehicles available to Indian salaried professionals and self-employed earners alike.

This post covers what NPS actually is, the Tier I vs Tier II distinction, the asset allocation choices (Active vs Auto), the three layered tax deductions, the partial-withdrawal rules during the working years, and the 60%-lump-sum + 40%-annuity structure at maturity.

What NPS actually is

The National Pension System is a voluntary defined-contribution retirement scheme launched in 2004 for new government employees and opened to all Indian citizens in 2009. It is regulated by the Pension Fund Regulatory and Development Authority (PFRDA) under the PFRDA Act 2013.

Three structural features distinguish NPS from the other retirement schemes covered in this pillar:

Market-linked returns, not guaranteed. Unlike PPF (7.1% government-fixed) or EPF (8.25% EPFO-declared), NPS returns depend on the performance of the underlying assets — equities, corporate debt, government securities, and alternative investments. Long-term returns have historically beaten fixed-rate small-savings instruments, but with year-to-year volatility.

Lowest cost retirement product in India. PFRDA caps fund management fees at 0.09% per year — among the lowest worldwide for a regulated retirement product. By comparison, a typical Indian equity mutual fund charges 1.5-2.25% per year in expense ratio.

Unique additional ₹50,000 tax deduction. Section 80CCD(1B) provides a deduction exclusively for NPS contributions — over and above the universal ₹1.5 lakh Section 80C limit. This makes NPS the only instrument in Indian taxation that can reduce taxable income beyond the 80C cap on its own.

Eligibility and account types

NPS accepts any Indian citizen aged 18-70 (extended from 60 in 2017 and 65 in 2021). NRIs can subscribe as well. Two account types are available:

| Account | Lock-in | Tax benefit | Purpose |

|---|---|---|---|

| Tier I | Until age 60 (limited partial withdrawals before) | Yes — 80CCD(1), 80CCD(1B), 80CCD(2) | Primary retirement corpus |

| Tier II | None — withdraw anytime | None for non-government subscribers | Voluntary investment account |

Most NPS subscribers use only Tier I. Tier II is rarely used because it offers no tax benefits for the general population (only central government employees with a 3-year lock-in get an 80C deduction on Tier II).

A subscriber receives a unique Permanent Retirement Account Number (PRAN) at registration. The PRAN is portable across jobs, cities, and pension fund managers — similar in concept to the EPF Universal Account Number (UAN).

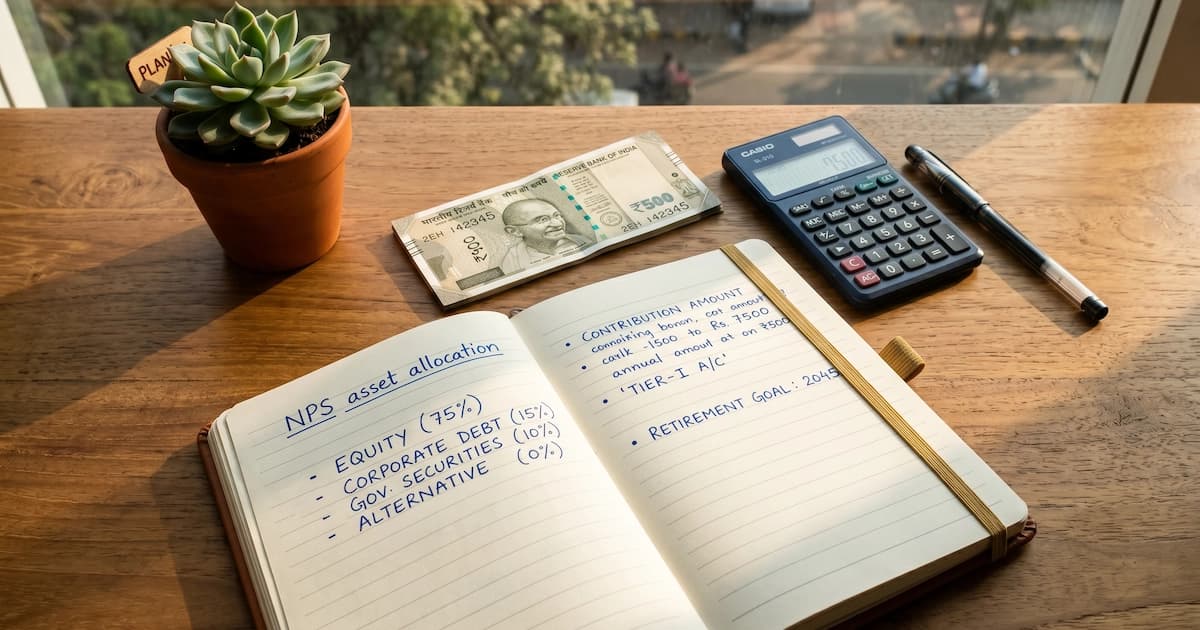

Asset allocation — Active vs Auto Choice

NPS subscribers can choose how their contributions are invested across four asset classes:

| Asset class | What it invests in | PFRDA cap |

|---|---|---|

| E (Equity) | Listed equity, large + mid-cap | 75% maximum for any subscriber |

| C (Corporate Debt) | Corporate bonds, AA-rated or above | Up to 100% |

| G (Government Securities) | Central + state government bonds | Up to 100% |

| A (Alternative Investment Funds) | REITs, InvITs, certain alternatives | 5% maximum |

Two choice modes:

Active Choice. The subscriber sets their own allocation across E, C, G, A subject to the caps above. Reviewing and rebalancing is the subscriber's responsibility. Best for engaged subscribers who want control.

Auto Choice (Lifecycle Fund). PFRDA automatically rebalances the asset allocation based on the subscriber's age. Three lifecycle profiles:

- LC75 (Aggressive): Equity starts at 75% at age 35 or below, declines to 15% by age 55+

- LC50 (Moderate, default): Equity starts at 50% at age 35 or below, declines to 10% by age 55+

- LC25 (Conservative): Equity starts at 25% at age 35 or below, declines to 5% by age 55+

For most subscribers without strong views on investment allocation, the LC50 default is reasonable. LC75 makes sense for younger subscribers with longer time horizons; LC25 for older subscribers approaching retirement.

The three layered tax deductions

NPS is unusual in Indian tax law for offering three separate, stackable deductions:

| Section | Limit | Who it covers |

|---|---|---|

| 80CCD(1) | ₹1,50,000/year — shared with overall 80C basket | Employee contribution (capped at 10% of salary for salaried, 20% of gross income for self-employed) |

| 80CCD(1B) | ₹50,000/year — exclusive to NPS, above the 80C cap | Additional voluntary NPS contribution |

| 80CCD(2) | Up to 10% of basic + DA (14% for central government employees) — no upper cap | Employer contribution to corporate NPS |

A maxed scenario for a corporate employee earning ₹15 lakh basic:

- 80CCD(1): ₹1.5 lakh (shared with PPF, EPF, ELSS, life insurance)

- 80CCD(1B): ₹50,000 (exclusive to NPS)

- 80CCD(2): Up to ₹1.5 lakh (10% of ₹15 lakh basic, no cap)

- Total NPS-related deduction from taxable income: up to ₹3.5 lakh

For self-employed earners, only 80CCD(1) and 80CCD(1B) apply — the employer contribution doesn't exist. Maximum deduction is ₹2 lakh.

This combination is why NPS has become particularly popular among higher-earning salaried professionals and self-employed consultants over the past decade.

The 60% lump sum + 40% annuity rule at maturity

NPS Tier I matures at age 60 (or up to 75 with deferred withdrawal). At maturity, the corpus is split:

| Portion | Treatment | Tax status |

|---|---|---|

| 60% of corpus | Withdrawn as lump sum | Tax-free under Section 10(12A) |

| 40% of corpus | Mandatorily used to purchase an annuity from a PFRDA-approved insurer | Annuity income taxed as salary income |

The annuity purchase is non-negotiable — the 40% must be used to buy a regular monthly pension from one of the PFRDA-empanelled annuity service providers. Common annuity options include:

- Annuity for life only (highest monthly amount, payments stop at death)

- Annuity for life with return of purchase price (lower monthly amount, corpus returned to nominee at death)

- Joint life annuity (continues to spouse after subscriber's death)

- Annuity with 5/10/15/20-year guarantee period

The lump-sum portion of NPS being tax-free is meaningful. Compared to EPF (also tax-free maturity) and PPF (also tax-free maturity), NPS is in the same favourable category at maturity but with a mandatory annuity-purchase obligation that the other two don't have.

Partial withdrawal rules during the working years

NPS allows partial withdrawals from Tier I after 3 years of subscription, but only for specific purposes and within strict caps:

| Parameter | Rule |

|---|---|

| Minimum subscription period | 3 years |

| Maximum withdrawal per request | 25% of subscriber's own contributions (not the entire corpus) |

| Total withdrawals allowed in lifetime | 3 |

| Allowed purposes | Children's higher education, children's marriage, house purchase/construction, medical emergency, disability, skill development |

| Tax treatment | Tax-free up to the withdrawal limit |

These restrictions make NPS less flexible than EPF (which allows multiple withdrawal categories with separate caps) and significantly less flexible than PPF (where partial withdrawal from year 7 onwards has no purpose restriction).

Premature exit before age 60

Subscribers can exit NPS before age 60 — but with stricter rules than at-maturity:

| Premature exit (before 60) | Mandatory split |

|---|---|

| Lump sum withdrawal | 20% of corpus |

| Annuity purchase | 80% of corpus |

For very small corpora (under ₹2.5 lakh), the entire amount can be withdrawn as lump sum without the annuity purchase requirement. For corpora above ₹2.5 lakh, the 20%/80% split applies.

This premature-exit penalty is the main reason NPS is positioned strictly as a long-term retirement vehicle — early exit forces a much larger annuity purchase than the standard at-maturity 40%.

NPS vs EPF vs PPF — practical comparison

For salaried Indian employees, NPS sits alongside EPF (mandatory workplace) and PPF (voluntary). The choice isn't usually "which one" but "how much to each":

| Factor | NPS Tier I | EPF | PPF |

|---|---|---|---|

| Eligibility | Any Indian 18-70 | Salaried (mandatory at 20+ employee firms) | Any Indian resident |

| Returns (typical) | 9-13% equity-heavy (market-linked) | 8.25% guaranteed (FY 24-25) | 7.1% guaranteed |

| Lock-in | Until 60 (limited withdrawals after 3 years) | Until retirement (multiple early-withdrawal triggers) | 15 years (extendable; partial from year 7) |

| Tax deduction (contribution) | ₹2 lakh (80C + 80CCD(1B)) for non-corporate | Section 80C (employee share) | Section 80C |

| Tax treatment (maturity) | 60% tax-free lump sum + 40% taxable annuity | Tax-free after 5 years service | Tax-free |

| Cost / fees | 0.09% per year (lowest in India) | None to member | None to member |

| Withdrawal flexibility | Lowest among the three | Highest among the three | Moderate |

A reasonable allocation framework for salaried earners with capacity to fund all three: max EPF mandatorily (12% employee + 12% employer), max PPF to ₹1.5 lakh annually (80C deduction), use NPS for the additional ₹50,000 tax-saving under 80CCD(1B) plus any employer contribution available. For the broader Pillar 8 context on these schemes, see what is Employee Provident Fund (EPF) and what is Public Provident Fund (PPF).

What experts say

The PFRDA portal is the authoritative source for current NPS rules, scheme structure, asset allocation caps, and the list of registered Pension Fund Managers. The NPS Trust website covers subscriber-facing operational details including PRAN registration and online account access.

The Income Tax Department's Section 80CCD documentation covers the layered deduction mechanics including 80CCD(1), 80CCD(1B), and 80CCD(2). The Reserve Bank of India's reports on the Indian pension landscape provide broader context on how NPS fits within the Indian retirement-savings framework.

For the broader Pillar 8 context, see what is Atal Pension Yojana (the smaller-scale pension scheme for unorganized-sector workers) and the EPF/PPF comparisons above.

Frequently asked questions

What's the difference between NPS Tier I and Tier II accounts? Tier I is the primary NPS retirement account — locked until age 60, with limited partial withdrawals for specific purposes (medical, higher education, marriage, house purchase). At maturity, 60% can be withdrawn as a tax-free lump sum and the remaining 40% must be used to purchase an annuity. Tier II is a voluntary investment account with no lock-in, free withdrawal anytime, no tax benefit on contributions (unless government employee), and works essentially like a mutual fund within the NPS framework. Most subscribers use only Tier I; Tier II is rare in practice.

What tax benefits does NPS offer? NPS Tier I contributions qualify for three separate Section 80C-related deductions. Section 80CCD(1) covers contributions up to ₹1.5 lakh per year as part of the broader Section 80C limit. Section 80CCD(1B) provides an additional ₹50,000 deduction exclusively for NPS — over and above the 80C cap, making NPS one of the few instruments that can reduce taxable income beyond ₹1.5 lakh. Section 80CCD(2) allows employer contributions to corporate NPS up to 10% of basic salary (14% for central government employees) to be deducted from the employee's taxable income with no upper cap. At maturity, the 60% lump sum is tax-free; the 40% annuity income is taxable as salary.

What returns can I expect from NPS? NPS returns are market-linked, not guaranteed. The PFRDA caps equity allocation at 75% for any single subscriber. Historical 10-year annualised returns from NPS funds have ranged roughly 9-13% for equity-heavy schemes, 7-9% for corporate debt, and 7-8% for government securities. The Aggressive Lifecycle Fund (LC75) starts at 75% equity for subscribers under 35 and gradually reduces equity exposure as age increases. The Conservative Lifecycle Fund (LC25) caps equity at 25%. Actual returns depend on chosen scheme, asset allocation, and subscription duration.

Can I withdraw from NPS before retirement? Partial withdrawals from Tier I are permitted after 3 years of subscription, capped at 25% of the subscriber's own contributions (not the entire corpus including employer contribution or returns). Allowed purposes are limited: children's higher education, children's marriage, house purchase or construction, medical emergencies for self or family, disability, and skill development. Maximum 3 partial withdrawals are allowed in a subscriber's lifetime. Premature exit before 60 is permitted but with stricter rules: 80% mandatorily annuity, 20% lump sum, with both portions becoming taxable in some cases.

In summary

NPS is a voluntary defined-contribution retirement scheme regulated by PFRDA, paying market-linked returns (historically 9-13% for equity-heavy schemes) with the lowest fund-management cost (0.09%) among Indian retirement products. Its standout tax feature is Section 80CCD(1B) — an additional ₹50,000 deduction exclusively for NPS, above the universal ₹1.5 lakh 80C cap, making NPS one of the few instruments that can reduce taxable income beyond 80C. For salaried employees with employer contributions, the layered 80CCD(1) + 80CCD(1B) + 80CCD(2) deductions can total ₹3+ lakh in annual taxable-income reduction.

The maturity structure — 60% tax-free lump sum + 40% mandatory annuity purchase — makes NPS structurally different from EPF and PPF (both fully tax-free at withdrawal). The 40% annuity income is taxable, which slightly reduces the post-tax appeal versus alternatives. The lock-in is also significantly stricter than PPF or EPF, with partial withdrawals limited to specific purposes and capped at 25% of own contributions.

The next read in this pillar covers Atal Pension Yojana — the smaller-scale guaranteed-pension scheme for unorganized-sector workers and lower-income earners. For broader Pillar 8 context on the universal retirement schemes, see Employee Provident Fund (EPF) and Public Provident Fund (PPF).

For how NPS compares with the fixed-rate government schemes across the board, see our Indian government savings schemes overview.

Sources

- Pension Fund Regulatory and Development Authority (PFRDA), NPS Scheme Documents — pfrda.org.in

- NPS Trust, Subscriber Services and Asset Allocation Rules — npstrust.org.in

- Income Tax Department of India, Section 80CCD(1), 80CCD(1B), 80CCD(2) — incometax.gov.in

- Ministry of Finance, Department of Financial Services, NPS Framework — financialservices.gov.in

- Reserve Bank of India, Annual Reports on Pension Sector — rbi.org.in

You might also like

What is EPF (Employee Provident Fund)? The 8.25% interest rate, mandatory 12%+12% employee/employer contribution, EPS split, withdrawal rules, and tax treatment explained for salaried Indian workers.

9 min read

PPF pays 7.1% for Jul-Sep 2026, unchanged since 2020. See the Rs 500 to Rs 1.5 lakh limits, EEE tax, 15-year lock-in, withdrawal rules and a maturity example.

13 min read

What is Atal Pension Yojana? The guaranteed monthly pension of ₹1,000-₹5,000 at age 60, eligibility for unorganized-sector workers aged 18-40, monthly contribution table, and how APY differs from NPS.

9 min read