What Is Form 16 in India: The TDS Certificate Your Employer Issues for ITR Filing

By Tapabrata Biswas · Published May 24, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of Form 16 as administered by the Income Tax Department under Section 203 of the Income Tax Act, 1961. This post is not tax filing advice. Reconciling Form 16 with Form 26AS, choosing the correct ITR form, and handling discrepancies depends on individual circumstances that only a qualified Chartered Accountant familiar with your situation can correctly assess. Consult a CA before filing your ITR.

Form 16 is the document salaried Indians collect from their employer between April and June every year — and the document that confuses millions of taxpayers because nobody ever explained what its two parts mean, where each comes from, or what to do when Part A from TRACES doesn't match the employer-prepared Part B. The structural mechanic is straightforward once decoded: Part A is the system-generated proof that TDS was deposited with the government; Part B is the employer's calculation showing how the TDS amount was arrived at.

This post covers what Form 16 actually is, the difference between Part A (TRACES-generated) and Part B (employer-prepared), the related Form 16A for non-salary TDS, the June 15 issuance deadline, how Form 16 supports ITR filing, and how to reconcile Form 16 against Form 26AS.

What Form 16 actually is

Form 16 is the TDS certificate that an Indian employer issues to every salaried employee whose salary attracted Tax Deducted at Source during the financial year. It is issued under Section 203 of the Income Tax Act, 1961 and is one of the most important documents in the Indian salaried-taxpayer's annual filing cycle.

The form documents three things:

- The gross salary paid to the employee across the financial year

- The exemptions and deductions the employer allowed while computing TDS (HRA exemption, standard deduction, Section 80C investments declared, etc.)

- The total TDS deducted from salary and deposited with the Central Government on the employee's behalf

For details on how the underlying TDS mechanism works, see what is TDS (tax deducted at source). For the slab structure that determines how much TDS was deducted, see income tax slab India explained.

The employer must issue Form 16 by 15 June of the assessment year following the financial year in question. For FY 2025-26 salary, the deadline is 15 June 2026 — meaning by the time most salaried Indians sit down to file their ITR in July-August, Form 16 should already be in hand.

The form is used as supporting documentation when filing the annual ITR-1 or ITR-2 (depending on income complexity). The taxpayer transcribes the salary figures and TDS credit from Form 16 into the ITR and claims credit for the TDS already deposited.

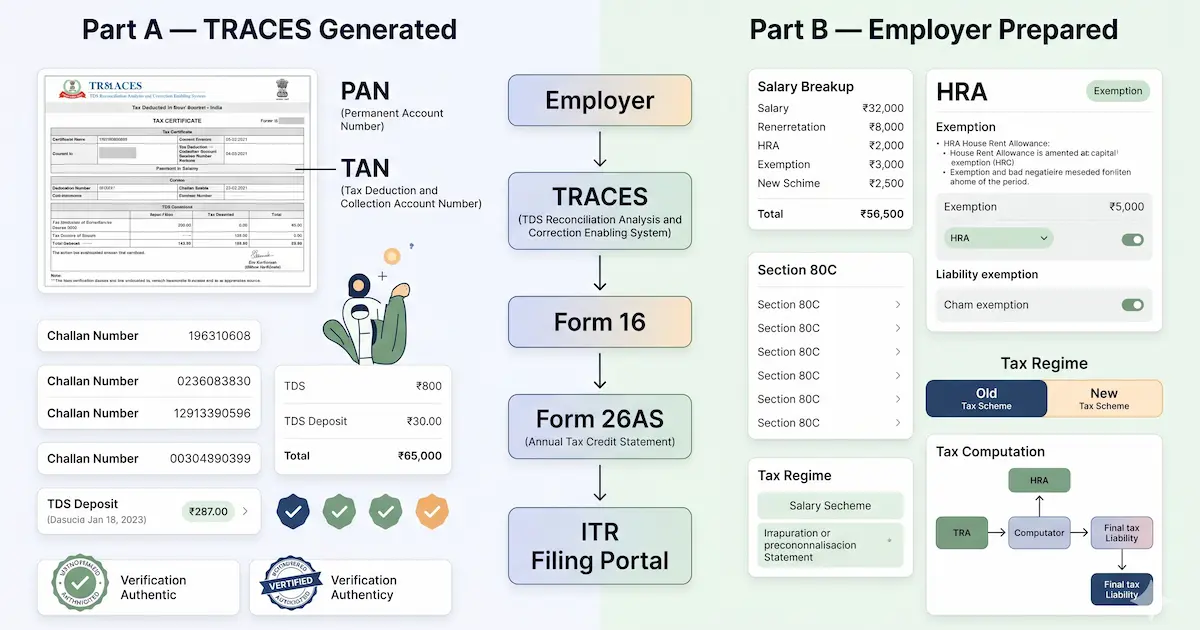

Form 16 has two parts — Part A vs Part B

This is the structural distinction most taxpayers miss. Form 16 is actually a composite of two separately-sourced documents bound together.

Part A — TRACES-generated, system-issued

Part A is generated by the Income Tax Department's TRACES portal (TDS Reconciliation Analysis and Correction Enabling System) — not by the employer. The employer files quarterly TDS returns (Form 24Q for salary TDS) with the IT Department. TRACES processes these returns and generates Part A as a downloadable PDF that the employer then includes in the Form 16 package.

What Part A contains:

- Employer name and TAN (Tax Deduction and Collection Account Number)

- Employee name and PAN

- Period of employment in the relevant financial year

- Quarter-by-quarter breakdown of salary paid and TDS deducted and deposited

- BSR codes, challan numbers, and dates of TDS deposits

- A unique TRACES certificate number for verification

Part A is tamper-resistant — once generated by TRACES, the data cannot be edited by the employer. If the employer made errors when filing the TDS return, the only way to correct Part A is to file a revised TDS return, after which TRACES regenerates a corrected Part A.

Part B — Employer-prepared, narrative section

Part B is prepared by the employer's payroll team and shows the detailed working from gross salary to TDS deducted. It is essentially the employer's tax calculation worksheet for the employee.

What Part B contains:

- Detailed salary breakup: Basic, HRA, special allowances, bonus, perquisites

- Exemptions claimed: HRA exemption (per Section 10(13A)), transport allowance, LTA, etc.

- Allowable deductions under Chapter VI-A: Section 80C investments, 80CCD NPS contributions, 80D health insurance, 80E education loan interest, etc.

- Tax regime under which the employee filed (old or new)

- Standard deduction (₹75,000 new regime / ₹50,000 old regime)

- Taxable income after all exemptions and deductions

- Income tax payable based on applicable slab rates

- Health and Education Cess (4%) added on top

- Total TDS to be deducted for the year — which should match Part A's total

Part B is the document that reflects the choices the employee made during their Investment Declaration (Form 12BB) submission at the start of the financial year. If the employee claimed full ₹1.5 lakh under Section 80C, that claim appears in Part B as a deduction subtracted from gross salary. The employee's EPF contribution is typically the largest single Section 80C entry in Part B — the 12% of basic salary deduction shows up automatically without the employee having to declare it separately.

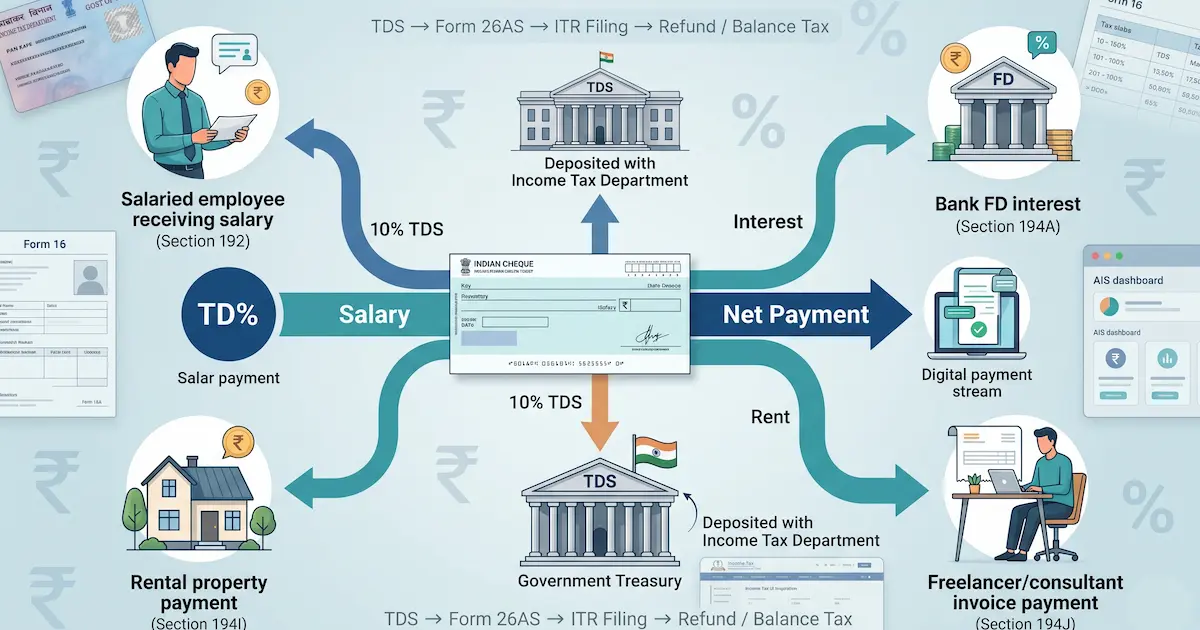

How Form 16 differs from Form 16A

Different forms for different income types:

| Form | Income type | Issued by | Frequency |

|---|---|---|---|

| Form 16 | Salary income (TDS under Section 192) | Employer | Annually, by 15 June |

| Form 16A | Non-salary TDS (Sections 194A, 194I, 194J, 194C, 194, etc.) | Bank, client, tenant, company, any deductor | Quarterly, within 15 days of quarter-end |

A salaried person with bank FD interest above ₹50,000/year would typically receive:

- One Form 16 from their employer covering salary TDS under Section 192

- One or more Form 16As from their bank(s) covering interest TDS under Section 194A

- Possibly additional Form 16As from any other source of TDS-able income (freelance clients, rental income above ₹2.4 lakh, dividend income above ₹10,000, etc.)

All of these flow into the same Form 26AS under the taxpayer's PAN, and the taxpayer claims credit for the combined total TDS when filing ITR.

Form 16A has only one part (equivalent to Form 16's Part A — TRACES-generated). There is no Part B for Form 16A because the deductor isn't computing tax on the recipient's behalf, just deducting a flat statutory rate per the relevant TDS section.

How Form 16 supports ITR filing

The annual ITR filing for a salaried taxpayer typically follows this sequence:

Step 1 — Collect Form 16 from employer. By 15 June following the end of the financial year. Verify both Part A and Part B are present.

Step 2 — Download Form 26AS from the Income Tax e-filing portal. Compare against Form 16 Part A. The total TDS in Form 26AS for the employer should match the total in Part A. If there's a mismatch, raise with the employer's payroll team before proceeding (see "What to do about mismatches" below).

Step 3 — Choose the appropriate ITR form. ITR-1 (Sahaj) for salary + one house property + interest income; ITR-2 for capital gains, multiple house properties, foreign income, or other complications.

Step 4 — Transcribe salary and deduction data from Form 16 Part B into the ITR. The salary figure, exemptions, deductions, and tax liability calculation all flow from Part B.

Step 5 — Claim TDS credit per Form 26AS. The total TDS credit claim in the ITR should match the Form 26AS total — including TDS from employer (Section 192), bank interest (Section 194A), and any other source.

Step 6 — Compute final tax liability. If TDS already paid (per Form 26AS) exceeds the computed tax liability, the difference is refundable. If TDS is less than liability, the balance must be paid as self-assessment tax before filing.

Step 7 — File ITR online via the e-filing portal and e-verify. Filing without e-verification (via Aadhaar OTP, net banking, or other methods) renders the ITR invalid.

For the complete salaried filing flow that begins with Form 16 — regime choice, deductions, capital gains, and e-verification — see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

What to do about Form 16 vs Form 26AS mismatches

A common scenario: Form 16 Part A from the employer shows ₹97,500 of TDS deducted; Form 26AS shows only ₹75,000 under the same employer's TAN. The ₹22,500 gap means the employer reported it but possibly didn't deposit it correctly, or the TDS return had errors.

The reconciliation sequence:

- Compare Part A line-by-line with Form 26AS. Identify exactly which quarter and which challan(s) are mismatched.

- Raise the issue with the employer's payroll/HR team. Request that they review the TDS return (Form 24Q) for the relevant quarter and file a correction (revised return) if needed.

- Wait for TRACES to update. Once the corrected return is filed, TRACES updates Form 26AS within a few weeks. The employer's Part A may also regenerate.

- If unresolved before the ITR deadline, consult a Chartered Accountant on the safest filing approach. Options include filing per Form 16 with explanatory notes, filing per Form 26AS (lower TDS credit, higher self-assessment tax), or requesting an extension.

Mismatches are not the employee's fault, but the employee bears the consequence — TDS credit claimed must match Form 26AS, otherwise the ITR is treated as defective. Always reconcile before filing, and bring in a CA for any meaningful gap.

What this post deliberately does not cover

Three out-of-scope topics:

1. "Can I file ITR without Form 16?" — Technically yes, if you can compute your salary and TDS independently from monthly payslips, but it's discouraged because Form 16 is the authoritative employer-issued document the IT Department expects. Discuss with a CA if your employer is non-responsive about issuing Form 16.

2. "How do I file a revised return if I made errors?" — Revised return mechanics under Section 139(5) have specific procedural requirements and time limits that warrant CA guidance.

3. "What's the correct ITR form for my situation?" — ITR-1 vs ITR-2 vs ITR-3 vs ITR-4 selection depends on income sources (salary, business, capital gains, foreign income, etc.) and is the kind of selection that benefits from professional guidance, particularly for taxpayers with multiple income streams.

The structural takeaway: Form 16 is your employer-issued TDS certificate combining a system-generated Part A (proof of TDS deposit) and an employer-prepared Part B (salary and deduction breakup). It is supporting documentation for ITR filing, not a substitute for filing the ITR itself. For any meaningful complication — mismatches, missing forms, unusual income — a Chartered Accountant is the right professional.

Frequently asked questions

What is Form 16 in simple terms? Form 16 is the TDS (Tax Deducted at Source) certificate that an Indian employer is legally required to issue to every salaried employee whose salary attracted TDS during the financial year. It is issued under Section 203 of the Income Tax Act, 1961 and documents three things: the gross salary paid, the exemptions and deductions allowed by the employer while computing TDS, and the total TDS deducted and deposited with the Income Tax Department. Form 16 is the primary supporting document for filing the annual ITR — it provides the salary income figure, the TDS credit claim, and the basis for the regime/exemption choices the employee made during the year. Employers must issue Form 16 by June 15 of the assessment year (e.g., by June 15, 2026 for FY 2025-26 salary).

What's the difference between Part A and Part B of Form 16? Form 16 has two parts that come from different sources. Part A is generated by the Income Tax Department's TRACES portal (TDS Reconciliation Analysis and Correction Enabling System) from the TDS returns the employer files. It shows the employer's TAN, the employee's PAN, the period of employment, and a quarter-by-quarter breakdown of salary paid and TDS deducted and deposited. Part B is prepared by the employer and shows the detailed salary breakup (basic, HRA, allowances), the exemptions claimed (HRA exemption, transport allowance, LTA, etc.), the deductions claimed under Chapter VI-A (80C, 80CCD, 80D, etc.), and the final taxable income and tax liability calculation. Part A is system-generated and tamper-resistant; Part B is employer-prepared and reflects the employee's investment declaration. Both parts together form the complete Form 16.

What is Form 16A and how is it different from Form 16? Form 16A is the TDS certificate for non-salary income — bank interest, professional fees, rental income, contractor payments, dividends, and any other income where TDS was deducted under sections other than Section 192. The deductor (bank, client, tenant, company) issues Form 16A to the deductee (you). Form 16A has only one part (Part A equivalent — TRACES-generated), unlike Form 16 which has both Part A and Part B. A salaried person with bank FD interest above ₹50,000/year would typically receive a Form 16 from their employer and a Form 16A from their bank — both contribute to the total TDS credit claimed in the ITR. Form 16A issuance deadline is 15 days from the end of each quarter for whichever TDS payments occurred in that quarter.

What do I do if my Form 16 doesn't match Form 26AS? Form 16 (issued by the employer) and Form 26AS (consolidated tax statement from the Income Tax Department) should show identical TDS figures. When they don't match, the mismatch usually arises from one of three reasons: the employer deducted TDS but failed to deposit it correctly with the government, the employer used the wrong PAN when filing the TDS return, or the employer's TDS return was filed late or has errors. The reconciliation process: first, compare Form 16 Part A to Form 26AS line-by-line for any discrepancies. Second, raise the issue with the employer's payroll team and request correction of the TDS return (Form 24Q for salary). Third, if unresolved, the taxpayer can file the ITR claiming credit per Form 16 with a note explaining the mismatch — but this can flag the return for scrutiny. For any meaningful mismatch, consult a Chartered Accountant before filing the ITR — they can guide the correction sequence and the safest filing approach for your situation.

Sources

- Income Tax Department of India, Section 203 — Certificate of Tax Deduction at Source — incometax.gov.in

- Central Board of Direct Taxes (CBDT), Form 16 Issuance Guidelines and Deadlines — incometaxindia.gov.in

- TRACES — TDS Reconciliation Analysis and Correction Enabling System — tdscpc.gov.in

- Income Tax Department, Form 24Q — Employer Quarterly TDS Return — incometax.gov.in

- Income Tax Department, Form 26AS — Annual Tax Statement — incometax.gov.in/iec/foportal

- Tax Information Network (TIN-NSDL), TDS Operating Procedures — tin-nsdl.com

You might also like

What is TDS? Tax Deducted at Source, the mechanism where the payer of certain income deducts tax before paying the recipient and deposits it with the government. Covers Section 192 (salary), 194A (interest), 194I (rent), 194J (professional fees), 194C (contractor payments), 194 (dividends), the PAN requirement under Section 206AA, current FY 2025-26 thresholds, and how TDS reconciles against ITR liability via Form 26AS.

9 min read

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

HRA exemption is the least of three amounts under Section 10(13A). See the FY 2025-26 formula, a worked example, metro cities, the limit, and the claim rules.

13 min read