What Is Capital Gains Tax: How Short-term and Long-term Gains Are Taxed in India and the US

By Tapabrata Biswas · Published May 24, 2026 · 10 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of capital gains tax in India (as administered by the Income Tax Department under the Income Tax Act, 1961) and the United States (as administered by the Internal Revenue Service under the Internal Revenue Code). This post is not tax planning or investment advice. Capital gains tax computations depend on asset class, holding period, indexation choices, applicable exemptions under Sections 54/54EC/54F (India) or Section 121 / 1031 exchanges (US), and individual circumstances that only a qualified Chartered Accountant (India) or Certified Public Accountant (US) familiar with your situation can correctly assess. Consult the appropriate professional before any decision involving capital gains tax.

Capital gains tax is structurally one of the most consequential taxes affecting Indian and US households because almost every investment decision — selling mutual funds, exiting equity positions, selling property, switching mutual fund schemes — triggers a capital gains event. India's Budget 2024 made significant changes to the structure (rates raised, indexation removed in most cases, holding periods unified) that took effect from July 23, 2024 and continue under FY 2025-26. The US structure has been more stable, with the preferential long-term rates of 0%/15%/20% remaining unchanged in recent years.

This post covers what capital gains tax actually is, the holding-period distinction that drives the short-vs-long classification, India's current post-Budget-2024 rates and rules, the US structure and 0/15/20% bracket system, worked examples for both countries, and the main exemption provisions in each.

What capital gains tax actually is

Capital gains tax is the tax on the profit from selling a capital asset.

The three definitional components:

-

Capital asset — broadly, any asset held for investment rather than for routine business use. Shares, mutual fund units, bonds, real estate (other than primary residence in some jurisdictions), gold, antique items, intellectual property rights, and similar assets all qualify. In India, the term is defined in Section 2(14) of the Income Tax Act with specific inclusions and exclusions.

-

Capital gain — the profit calculated as (sale price) minus (purchase price) minus (allowable expenses). Allowable expenses typically include brokerage charges, stamp duty, registration fees for real estate, and similar transaction costs. In some asset classes and jurisdictions, indexation (adjusting purchase price for inflation) is applied to reduce the taxable gain.

-

Tax rate — the percentage applied to the gain. The rate depends on holding period (short-term vs long-term) and asset class.

The structural rationale for differential rates: governments use lower long-term rates to incentivise long-term investment behaviour. Short-term gains, often associated with trading and speculative activity, get higher rates to discourage rapid in-out behaviour and improve tax revenue stability.

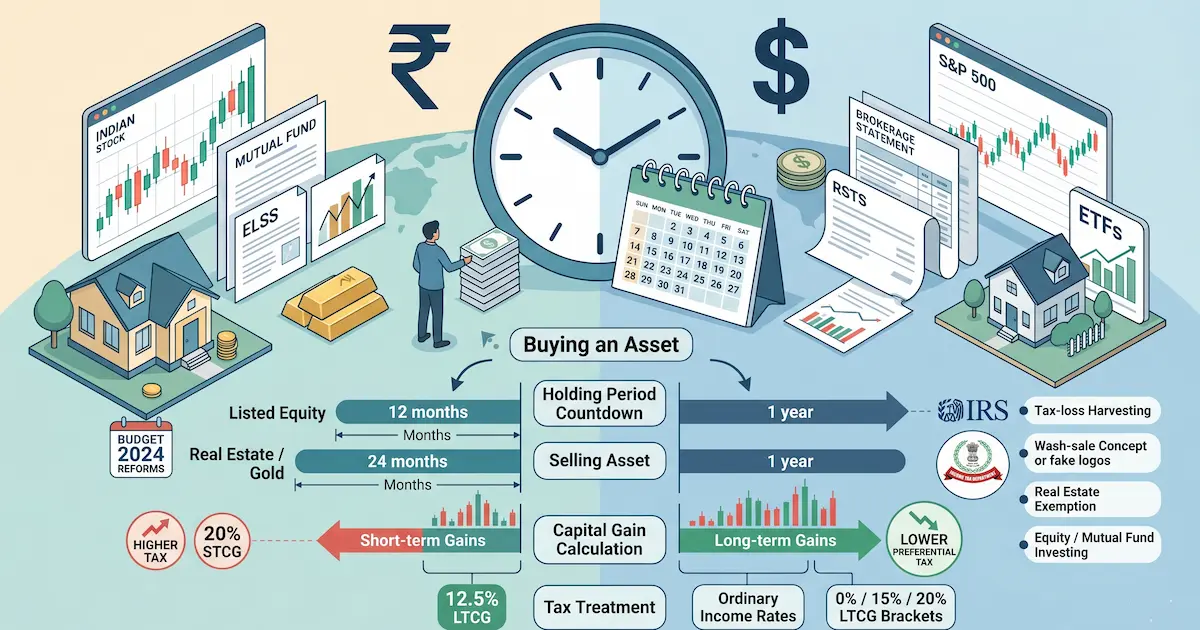

India's current capital gains tax structure (post-Budget 2024)

Budget 2024, presented by Finance Minister Nirmala Sitharaman on 23 July 2024, made the most significant changes to India's capital gains tax structure in over a decade. The changes took effect from that date and continue to apply in FY 2025-26.

Current India structure (FY 2025-26):

| Asset class | Holding period | STCG rate | LTCG rate | Annual exemption |

|---|---|---|---|---|

| Listed equity / equity mutual funds | 12 months | 20% | 12.5% | ₹1.25 lakh |

| Unlisted shares | 24 months | Slab rate | 12.5% | None |

| Real estate (residential / commercial) | 24 months | Slab rate | 12.5% (no indexation) | None |

| Gold (physical / ETF) | 24 months | Slab rate | 12.5% | None |

| Debt mutual funds (held after 1 Apr 2023) | N/A | Slab rate | Slab rate | None |

| Bonds, debentures | 24 months | Slab rate | 12.5% | None |

(Source: Income Tax Act, 1961 as amended by Finance (No. 2) Act, 2024)

Four key changes Budget 2024 introduced:

- LTCG on listed equity raised from 10% to 12.5%, exemption threshold raised from ₹1 lakh to ₹1.25 lakh annually

- STCG on listed equity raised from 15% to 20%

- LTCG on all non-equity assets unified at 12.5%, but indexation benefit removed for most cases (a major change for real estate and gold)

- Holding periods simplified to 12 months for listed securities and 24 months for all other assets

The indexation removal is the most consequential change for property holders. Previously, real estate LTCG was taxed at 20% with indexation, which often produced a lower effective tax than 12.5% without indexation. Budget 2024 made the new 12.5%-no-indexation regime the default, with a transitional grandfathering provision for properties purchased before 23 July 2024 (taxpayers can choose the lower of old 20%-with-indexation or new 12.5%-without).

The US capital gains tax structure

The US uses a similar short-vs-long distinction but with different specifics.

Current US structure (Tax Year 2025):

| Holding period | Classification | Rate |

|---|---|---|

| 1 year or less | Short-term capital gain | Ordinary income marginal rate (10-37% federally + state) |

| Over 1 year | Long-term capital gain | 0%, 15%, or 20% federally (bracket-dependent) |

(Source: Internal Revenue Code, Section 1(h))

The long-term rate bracket structure for individuals (Tax Year 2025, single filer):

| Taxable income | LTCG rate |

|---|---|

| Up to $48,350 | 0% |

| $48,351 – $533,400 | 15% |

| Above $533,400 | 20% |

(Brackets are wider for married joint filers.)

Most middle-income US households fall in the 15% LTCG bracket. The 0% bracket is significant — households with low taxable income (retirees living on Social Security, students, transitional periods) can realize substantial long-term gains without any federal tax, though state taxes may still apply.

Two notable structural differences from India:

1. No annual exemption. Unlike India's ₹1.25 lakh equity LTCG exemption, every dollar of US capital gain is taxable — just at preferential rates for long-term.

2. Wash-sale rules. Section 1091 of the IRC disallows a capital loss deduction if a "substantially identical" security is purchased within 30 days before or after the loss sale. The rule prevents taxpayers from selling at a loss to harvest tax savings while maintaining the same investment exposure. India has no equivalent wash-sale provision, making tax-loss harvesting structurally easier in India.

3. Net Investment Income Tax (NIIT). High-income US households (above $200,000 single / $250,000 joint MAGI) pay an additional 3.8% NIIT on capital gains under Section 1411. This effectively pushes the top federal LTCG rate to 23.8% for these taxpayers.

A worked example — Indian equity LTCG

An Indian investor sold ₹5 lakh of listed equity mutual fund units in March 2026 (FY 2025-26). The units were purchased in January 2024 for ₹3 lakh. Holding period: 26 months — qualifies as long-term.

| Component | Amount |

|---|---|

| Sale value | ₹5,00,000 |

| Less: Purchase value | −₹3,00,000 |

| Capital gain | ₹2,00,000 |

| Less: Annual LTCG exemption | −₹1,25,000 |

| Taxable LTCG | ₹75,000 |

| LTCG tax @ 12.5% | ₹9,375 |

| Plus: 4% Health and Education Cess | +₹375 |

| Total tax on this gain | ₹9,750 |

Effective tax rate on the ₹2 lakh gross gain: 4.9% (because most of the gain falls under the ₹1.25 lakh exemption).

If the same investor had also sold ₹2 lakh of equity within 12 months (STCG), that gain would be taxed at 20% — meaning ₹40,000 tax (plus cess) — on the same ₹2 lakh of profit. The structural punishment for short-term selling is significant.

A worked example — US long-term capital gain

A US investor in the 15% LTCG bracket sold $50,000 of stocks held for 18 months. Cost basis was $30,000.

| Component | Amount |

|---|---|

| Sale proceeds | $50,000 |

| Less: Cost basis | −$30,000 |

| Capital gain | $20,000 |

| LTCG tax @ 15% federal | $3,000 |

Plus state tax depending on residence (California: ~9.3% on capital gains as ordinary income, ~$1,860; Texas/Florida: $0 — no state income tax).

Total federal + state tax on the $20,000 gain ranges from $3,000 to roughly $4,860 depending on state.

If the same gain had been short-term (held under 1 year), it would be taxed at the investor's ordinary federal marginal rate (e.g., 22% for $90K-$200K range) plus state — easily double the long-term tax.

Main exemption provisions

Both countries have specific statutory provisions to reduce or defer capital gains tax in defined scenarios. Each provision has specific eligibility rules and procedural requirements that warrant case-by-case CA/CPA advice.

India — primary individual-level provisions:

- Section 54 — Reinvest LTCG from sale of residential property into another residential property within specified time limits (1 year before to 2 years after for purchase; 3 years for construction). Exemption capped at ₹10 crore from FY 2023-24.

- Section 54EC — Invest LTCG (from any capital asset) in specified bonds (NHAI, REC) within 6 months. Maximum investment ₹50 lakh per financial year. 5-year lock-in.

- Section 54F — Reinvest LTCG from any capital asset (except residential property) into a new residential property. Subject to conditions about owning other residential properties.

US — primary individual-level provisions:

- Section 121 — Primary Residence Exclusion — Exclude up to $250,000 ($500,000 for married joint) of capital gain from sale of primary residence if owned and used as primary home for 2 of the last 5 years.

- Section 1031 — Like-kind Exchanges — Defer capital gain on commercial real estate by exchanging for like-kind property within strict timelines (45-day identification, 180-day closing). Not available for personal-use property.

- Section 1411 NIIT exemption thresholds — High-income surcharge only applies above MAGI thresholds.

Both countries allow capital losses to offset capital gains within specified limits ($3,000/year ordinary income offset cap in US; ₹2 lakh / variable in India depending on asset class).

For how capital gains slot into a salaried person's return — including when they push you from ITR-1 to ITR-2 — see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

What this post deliberately does not cover

Four out-of-scope topics:

1. "Should I sell now or hold for long-term?" — Holding-period planning is investment advice combined with tax planning, both requiring personalized inputs. Consult a SEBI-registered investment adviser or financial planner (India) or fiduciary advisor (US).

2. "How do I claim Section 54 exemption?" — Procedural specifics (Capital Gains Account Scheme, time-limit compliance, eligible property types, joint ownership scenarios) need a CA's case-specific guidance.

3. "Is tax-loss harvesting worth it?" — Tax-loss harvesting is a planning strategy with regulatory nuances (wash-sale in US, dividend-stripping rules in India) and requires understanding of your full portfolio and tax bracket trajectory. Consult a CA/CPA.

4. "How does capital gains tax interact with my regime choice?" — In India, capital gains are taxed at their own statutory rates (12.5% / 20% / 12.5%) regardless of old vs new regime — the regime only affects salary and certain other income types. This interaction can affect overall tax planning and warrants CA input.

The structural takeaway: capital gains tax exists in both India and the US, both use a short-vs-long holding-period distinction, India's rates rose significantly in Budget 2024 with indexation largely removed, US rates remain at the 0%/15%/20% preferential structure with wash-sale and NIIT complications. Your specific computation, exemption strategy, and timing decisions all require professional advice — never make a capital gains decision based on general content.

Frequently asked questions

What is capital gains tax in simple terms? Capital gains tax is the tax you pay on the profit from selling a capital asset — shares, mutual fund units, real estate, gold, bonds, and similar investments. The tax applies only to the gain (sale price minus purchase price minus allowable expenses), not to the entire sale amount. The rate depends on how long you held the asset before selling. A shorter holding period gets short-term capital gains tax (STCG) at a higher rate; a longer holding period gets long-term capital gains tax (LTCG) at a lower rate. The exact holding-period thresholds and rates differ by asset class and country. India and the US both use this short-vs-long distinction but with different numbers.

What changed in India's capital gains tax in Budget 2024? Effective from July 23, 2024, Budget 2024 introduced four major changes to India's capital gains tax structure. First, LTCG on listed equity and equity mutual funds rose from 10% to 12.5%, with the annual exemption threshold raised from ₹1 lakh to ₹1.25 lakh. Second, STCG on listed equity and equity mutual funds rose from 15% to 20%. Third, LTCG on all non-equity assets (real estate, gold, debt funds, unlisted shares) was unified at 12.5% but the indexation benefit was removed for most cases. Fourth, holding periods were simplified to 12 months for listed securities and 24 months for all other assets. The Budget 2024 changes made capital gains tax simpler in structure but generally higher in rate for most asset classes — particularly painful for real estate holders who lost indexation.

How does the US capital gains tax structure compare to India's? The US uses a similar short-vs-long distinction but with different thresholds and rates. The holding period for long-term US capital gains is 1 year (anything held 12 months or longer qualifies). Long-term capital gains are taxed at preferential rates of 0%, 15%, or 20% depending on the taxpayer's ordinary income bracket — most middle-income US households pay 15% LTCG. Short-term capital gains (assets held under 1 year) are taxed as ordinary income at the taxpayer's marginal slab rate, which can be as high as 37% federally plus state tax. The US system has no annual exemption equivalent to India's ₹1.25 lakh threshold — every dollar of capital gain is taxable, just at differential rates. The US also has wash-sale rules that disallow tax-loss harvesting if a similar security is bought within 30 days; India has no equivalent wash-sale provision.

Are there exemptions or ways to reduce capital gains tax legally? Yes, several legitimate provisions exist in both countries, but the application to any specific situation depends on the asset type, holding period, intended use of proceeds, and many other variables. In India, Section 54 (reinvestment in another residential property), Section 54EC (investment in specified bonds up to ₹50 lakh), and Section 54F (reinvestment in a new house from any LTCG except property) are the main statutory exemption routes for property and certain other assets. In the US, the primary residence exemption ($250,000 for single filers / $500,000 for married joint filers) under Section 121 of the Internal Revenue Code is the largest individual-level exemption. 1031 like-kind exchanges defer real estate gains in certain commercial scenarios. Both countries also allow capital losses to offset capital gains within specified limits. The eligibility rules and procedural requirements for each provision are complex and warrant case-specific advice from a Chartered Accountant (India) or CPA (US) — never claim a capital gains exemption based on a general explainer.

Sources

- Income Tax Department of India, Section 45 to 55A — Capital Gains Provisions — incometax.gov.in

- Ministry of Finance, Finance (No. 2) Act 2024 — Capital Gains Rate Changes — indiabudget.gov.in

- Central Board of Direct Taxes (CBDT), Capital Gains Tax — Notifications and Circulars — incometaxindia.gov.in

- US Internal Revenue Service, Topic 409 — Capital Gains and Losses — irs.gov/taxtopics/tc409

- US Internal Revenue Service, Section 1(h), Section 121, Section 1031 — Internal Revenue Code — irs.gov

- US Internal Revenue Service, Net Investment Income Tax (NIIT) — irs.gov/individuals/net-investment-income-tax

- Tax Policy Center, How Does the Federal Government Tax Capital Gains? — taxpolicycenter.org

You might also like

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

What is TDS? Tax Deducted at Source, the mechanism where the payer of certain income deducts tax before paying the recipient and deposits it with the government. Covers Section 192 (salary), 194A (interest), 194I (rent), 194J (professional fees), 194C (contractor payments), 194 (dividends), the PAN requirement under Section 206AA, current FY 2025-26 thresholds, and how TDS reconciles against ITR liability via Form 26AS.

9 min read

Loss aversion is feeling losses about twice as intensely as equal gains. The 2.25 ratio, examples, loss vs risk aversion, and how it quietly hurts returns.

14 min read