Tax Deductions vs Credits + Standard vs Itemized Deduction: How US Tax Structure Reduces Liability

By Tapabrata Biswas · Published May 25, 2026 · 10 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

This is a research-led definitional explainer of the US tax structure for deductions vs credits and standard vs itemized deductions, with brief comparison to the Indian equivalent provisions. This post is not tax filing advice. US tax computation, the choice between standard and itemized deduction, and the eligibility for specific credits all depend on individual circumstances that only a qualified Certified Public Accountant (CPA) or IRS Enrolled Agent (EA) familiar with your situation can correctly assess. Consult a CPA before filing your US tax return or making tax-relevant decisions.

US tax law has four mechanisms for reducing your tax bill, and they work in distinctly different ways. Two of them — deductions and credits — sit at different points in the tax computation and have very different value. Two more — standard and itemized deductions — are mutually exclusive choices most taxpayers make once per year. Understanding the structural distinction between all four is the prerequisite for any meaningful tax-related decision-making in the US, whether evaluating a mortgage decision, a charitable contribution, an EV purchase, or which retirement-account contribution to make.

This post covers what each mechanism actually is, the math difference between deductions and credits, current TY 2025 standard deduction amounts, the main itemizable expense categories with their current limits, the structural decision of standard vs itemized, and a brief India comparison highlighting Chapter VI-A and the Section 87A rebate as the parallel structures.

Tax deductions vs credits — the math difference

The fundamental distinction:

| Mechanism | What it reduces | When applied | Value formula |

|---|---|---|---|

| Deduction | Taxable income | Before tax rate is applied | Deduction amount × your marginal rate |

| Credit | Tax owed | After tax has been computed | Dollar-for-dollar |

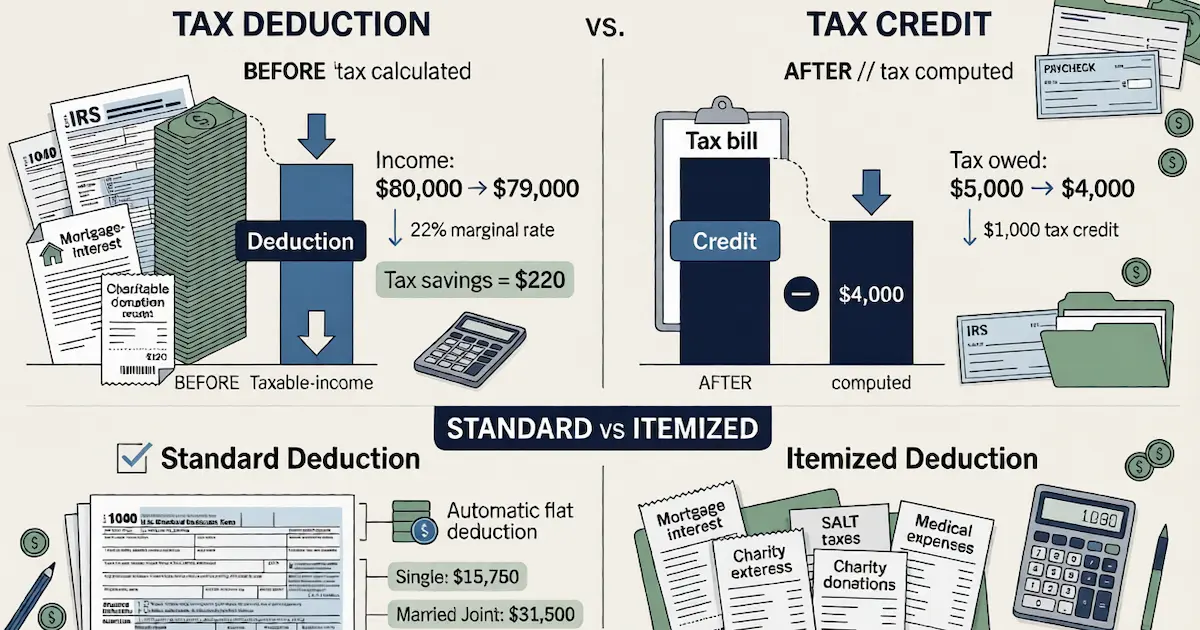

A worked comparison on a single $1,000:

A US taxpayer in the 22% marginal federal bracket has $80,000 taxable income before any consideration of the $1,000.

| Scenario | Computation | Tax savings |

|---|---|---|

| $1,000 deduction | Taxable income reduced to $79,000; tax recomputed at slab rates; tax decreases by $1,000 × 22% | $220 |

| $1,000 credit | Tax computed on $80,000; credit subtracted from final tax | $1,000 |

The credit is worth roughly 4.5× the deduction in this case (or more, depending on bracket). The reason is structural: a deduction subtracts at the top of your income (gets your marginal rate × the deduction); a credit subtracts at the bottom of your tax (dollar-for-dollar against tax owed).

This is why, when comparing tax provisions, credits are generally more valuable than deductions of the same dollar amount. A "$1,000 tax credit" headline almost always represents more tax savings than a "$1,000 tax deduction" headline.

Refundable vs non-refundable credits

Credits divide further into two categories:

Refundable credits — if the credit exceeds tax owed, the IRS pays out the difference as a refund. Examples: the Earned Income Tax Credit (EITC), the refundable portion of the Child Tax Credit, the Premium Tax Credit for ACA marketplace insurance.

Non-refundable credits — can reduce tax owed to zero, but cannot generate a refund. If you have $500 of tax owed and a $1,000 non-refundable credit, you get $500 of value (not $1,000). Examples: the Lifetime Learning Credit, the Child and Dependent Care Credit, the Saver's Credit, the EV Tax Credit (mostly non-refundable except in the transferred-credit scenario).

The distinction matters significantly for low-income taxpayers who may not have enough tax owed to fully use a non-refundable credit. A refundable credit delivers full value regardless; a non-refundable one is capped at the tax owed.

US standard deduction — the no-questions-asked baseline

The standard deduction is the flat dollar amount the IRS allows every taxpayer to subtract from their adjusted gross income (AGI) before computing taxable income. It's automatic — no receipts, no documentation, no per-expense itemization. Every taxpayer who doesn't itemize takes it.

Standard deduction amounts for Tax Year 2025 (filed in early 2026):

| Filing status | Standard deduction |

|---|---|

| Single | $15,750 |

| Married filing jointly | $31,500 |

| Head of household | $23,625 |

| Married filing separately | $15,750 |

These figures are inflation-adjusted annually under Section 63(c) of the Internal Revenue Code. The standard deduction is additional for taxpayers aged 65+ ($2,000 single / $1,600 per spouse in married joint, approximately) and for blind taxpayers — these are added to the base standard amount.

The Tax Cuts and Jobs Act of 2017 (TCJA) roughly doubled the standard deduction (raised from approximately $6,350 single / $12,700 married joint in TY 2017 to $12,000 / $24,000 in TY 2018). The TCJA changes are scheduled to sunset after TY 2025 unless Congress extends them, which would significantly affect this calculation for TY 2026 onwards. Always confirm current standard deduction against the IRS's published amount for your filing year.

The TCJA standard-deduction expansion is why approximately 90% of US taxpayers now claim the standard deduction rather than itemizing — most households' specific deductible expenses don't add up to more than the standard amount, so the standard is the simpler and larger deduction.

Itemized deduction — when summing specifics beats the standard

Itemized deduction is the alternative: instead of taking the flat standard amount, sum specific eligible expenses from a defined list and subtract that total. You must choose one or the other for any given tax year — you cannot do both.

Major itemizable expense categories (TY 2025):

| Category | What's deductible | Limits |

|---|---|---|

| State and Local Tax (SALT) | State income tax + property tax + sales tax | $10,000 household cap (TCJA 2017) |

| Home mortgage interest | Interest on primary + second home | Limited to $750,000 of mortgage principal (post-TCJA loans) |

| Charitable contributions | Donations to qualifying 501(c)(3) organisations | 60% of AGI for cash, 30% for appreciated assets |

| Medical expenses | Out-of-pocket medical costs | Only the portion exceeding 7.5% of AGI |

| Casualty and theft losses | Federally declared disaster losses | Subject to deductible thresholds |

| Investment interest expense | Interest on margin loans for investments | Limited to net investment income |

(Source: Internal Revenue Code, Sections 161-224, as administered by the IRS.)

The SALT cap of $10,000 introduced by the TCJA is the single most impactful itemization change in recent decades. Households in high-tax states (California, New York, New Jersey, Connecticut, Massachusetts) with property tax + state income tax exceeding $10,000 cannot deduct the excess. This cap is the primary reason itemization became less attractive for many middle-and-upper-middle-income households after 2017.

The standard-vs-itemized decision — illustrated

The decision is computational: sum your itemizable expenses and compare to the standard deduction for your filing status.

Scenario A — typical middle-income household (likely takes standard):

| Expense | Amount |

|---|---|

| State income tax | $4,500 |

| Property tax | $3,500 |

| Charitable contributions | $1,000 |

| Mortgage interest | $5,000 |

| Medical expenses (above 7.5% AGI threshold) | $0 |

| Total itemized | $14,000 |

Married filing jointly with this expense profile compares $14,000 itemized against $31,500 standard. Standard deduction wins by $17,500.

Scenario B — high-tax-state household with mortgage (might itemize):

| Expense | Amount |

|---|---|

| State income tax | $12,000 (only $10,000 deductible due to SALT cap, combined with property tax) |

| Property tax | $8,000 (capped above with state income tax at total $10K SALT) |

| Charitable contributions | $5,000 |

| Mortgage interest | $18,000 |

| Medical expenses | $0 |

| Total itemized (after SALT cap) | $33,000 |

Married filing jointly comparing $33,000 itemized against $31,500 standard. Itemized deduction wins by $1,500 — but only barely.

The arithmetic depends entirely on your specific expense numbers. The right approach for any taxpayer is for a CPA to run the calculation both ways during return preparation and select whichever produces the lower tax liability. For W-2 employees, the income figure that the standard or itemized deduction reduces comes from Box 1 of the annual W-2 form — that's where the $90K (or whatever the gross taxable wage is) originates before the deduction subtracts.

India equivalent — Chapter VI-A and Section 87A rebate

India's tax system has analogous structures but with different names and a fixed-list architecture:

India's "deduction" parallel — Chapter VI-A

The Income Tax Act's Chapter VI-A contains the deduction provisions: Section 80C (₹1.5 lakh — see what is Section 80C deduction), Section 80CCD(1B) (additional ₹50,000 NPS), Section 80D (health insurance premium), Section 80E (education loan interest, no cap), Section 80G (charitable donations), Section 80EE / 80EEA (home loan interest for first-time buyers), and others. These behave like US deductions — they reduce taxable income before slab rates apply, and tax savings equal the deduction × the taxpayer's marginal slab rate.

Critical: Chapter VI-A deductions are only available under the old regime. The new regime disallows them in exchange for lower slab rates.

India's "standard deduction" parallel

India has a standard deduction for salaried taxpayers — ₹75,000 under the new regime, ₹50,000 under the old regime — applied automatically without itemization. The Indian standard deduction is much smaller in absolute terms than the US version because India has a separate structure of exemptions (HRA, LTA) that don't exist in the US.

India does not have a US-style itemization option. The Indian deduction list is fixed by statute, and taxpayers either qualify for each item or don't — there's no choice between a flat amount and a summed-expense amount.

India's "credit" parallel — Section 87A rebate

The Section 87A rebate functions like a US tax credit. It reduces computed tax owed dollar-for-dollar up to a specified maximum:

- New regime FY 2025-26: up to ₹60,000 rebate (effective zero tax for income up to ₹12 lakh)

- Old regime: up to ₹12,500 rebate (effective zero tax for income up to ₹5 lakh)

The rebate is non-refundable (can reduce tax to zero but cannot generate a refund) and is automatic when income falls below the threshold — no separate claim required.

For more on how 87A interacts with slabs, see income tax slab India explained.

For how the 87A rebate and the regime choice play out for a salaried filer in practice, see our Indian Income Tax Guide for Salaried Employees 2026 (FY 2025-26).

Common confusion patterns

Three structural confusions worth flagging:

1. "A $5,000 deduction saves me $5,000 in tax." Wrong. A deduction saves marginal-rate × deduction. At 22%, a $5,000 deduction saves $1,100 in tax.

2. "Itemizing is always better because I get to claim my mortgage interest." Wrong since TCJA. With the much larger standard deduction post-2018, most households find the standard amount exceeds even mortgage interest + property tax (capped at $10K SALT). Itemizing produces a lower tax outcome only when the sum of itemizable expenses exceeds the standard deduction for the filing status.

3. "A tax credit and a tax deduction are the same thing in different language." Wrong. Credits are dollar-for-dollar; deductions are at your marginal rate. The IRS uses both terms specifically and the math is different — always check which one applies to a specific provision before estimating tax savings.

What this post deliberately does not cover

Four out-of-scope topics:

1. "Which credits should I claim?" — Eligibility for the Child Tax Credit, EITC, Saver's Credit, EV Tax Credit, education credits, and similar credits depends on individual circumstances (income thresholds, dependents, retirement contributions, vehicle purchase, education enrollment). Your CPA assesses eligibility per return.

2. "Should I bunch my deductions?" — "Bunching" charitable contributions or other expenses into alternating years to itemize one year and take the standard the next is a planning strategy requiring specific facts and circumstances.

3. "How do TCJA sunsets affect my planning?" — The TCJA changes (doubled standard deduction, $10K SALT cap, lower rates) are scheduled to sunset after TY 2025 unless Congress extends them. The interaction with multi-year planning is complex and depends on what Congress does in 2026.

4. "What's the right India regime choice considering all these factors?" — Regime choice between old (with deductions) and new (with lower rates) requires computation both ways with your actual deduction profile, which a CA performs per ITR.

The structural takeaway: deductions reduce taxable income at your marginal rate; credits reduce tax owed dollar-for-dollar. Standard vs itemized is a US-specific choice between a flat amount and a summed-expense amount. India's parallel structures (Chapter VI-A, standard deduction, Section 87A) work similarly but with a fixed-list architecture and regime-dependent availability. For any specific situation, the math is run by the appropriate professional during return preparation.

Frequently asked questions

What is the difference between a tax deduction and a tax credit? A tax deduction reduces your taxable income before the tax rate is applied. The tax savings equal the deduction amount multiplied by your marginal tax rate. A $1,000 deduction at a 22% marginal rate saves $220 in tax. A tax credit reduces your tax owed dollar-for-dollar after the rate has been applied. A $1,000 credit saves $1,000 in tax — period. Credits are generally more valuable than deductions of the same dollar amount because credits don't depend on your marginal rate. The US tax code has many of each: deductions include mortgage interest, charitable contributions, and SALT (state and local tax); credits include the Child Tax Credit, the Earned Income Tax Credit, and the EV Tax Credit. Some credits are refundable (paid out even if they exceed tax owed); some are non-refundable (can reduce tax to zero but not below).

What is the standard deduction in the US, and what amount is it? The standard deduction is a flat dollar amount the IRS allows every taxpayer to subtract from their gross income before computing taxable income — a 'no questions asked' deduction available regardless of actual expenses. For Tax Year 2025 (the year you file in early 2026), the standard deduction is $15,750 for single filers, $31,500 for married filing jointly, $23,625 for head of household. These figures are inflation-adjusted annually under Section 63(c) of the Internal Revenue Code. The standard deduction was significantly raised by the Tax Cuts and Jobs Act of 2017 (doubled, roughly) and is the reason approximately 90% of US taxpayers now claim the standard deduction rather than itemizing — most households' specific deductible expenses don't add up to more than the standard amount, so the standard is the simpler and larger deduction.

When does it make sense to itemize deductions instead of taking the standard deduction? Itemizing is generally beneficial only when your total itemizable expenses exceed the standard deduction. The most common itemizable expenses include: state and local taxes (SALT — property tax + state income tax, capped at $10,000 per household after the TCJA 2017), home mortgage interest on loans up to $750,000 principal, charitable contributions, medical expenses exceeding 7.5% of AGI, and some specific other categories. A married joint-filer household needs to sum these expenses and check whether the total exceeds $31,500 (TY 2025 standard). Households with large mortgages in high-tax states (NY, CA, NJ), high charitable giving, or significant medical expenses sometimes find itemizing produces more deduction than the standard amount. The decision is computational and requires actual expense numbers — your CPA runs the comparison both ways before filing your return.

Does India have a similar deduction-vs-credit and standard-vs-itemized structure? Partially. India has a standard deduction (₹75,000 under the new regime, ₹50,000 under the old, for salaried taxpayers) similar in concept to the US standard. India has many deductions under Chapter VI-A (Section 80C up to ₹1.5 lakh, 80CCD additional NPS, 80D health insurance, 80E education loan interest, 80G charitable donations) but these are only available under the old regime. India's primary credit equivalent is the Section 87A rebate, which reduces tax owed dollar-for-dollar up to a specified amount (₹60,000 under new regime for income up to ₹12 lakh; ₹12,500 under old regime for income up to ₹5 lakh). India does not have an itemizing option in the US sense — the deduction list is fixed by statute and taxpayers either qualify and claim or don't. Each Indian deduction has its own eligibility rules and documentation requirements. Consult a CA for the specific application to your situation.

Sources

- US Internal Revenue Service, Tax Topics — Standard Deduction and Itemized Deductions — irs.gov/taxtopics

- US Internal Revenue Service, Publication 17 — Your Federal Income Tax — irs.gov/publications/p17

- US Internal Revenue Service, Tax Credits — Overview — irs.gov/credits-deductions-for-individuals

- US Congress, Tax Cuts and Jobs Act of 2017 — Public Law 115-97 — congress.gov

- Tax Policy Center, Briefing Book — Standard Deduction and Itemized Deductions — taxpolicycenter.org

- Income Tax Department of India, Chapter VI-A Deductions and Section 87A Rebate — incometax.gov.in

- Central Board of Direct Taxes (CBDT), Income Tax Act Deduction Provisions — incometaxindia.gov.in

You might also like

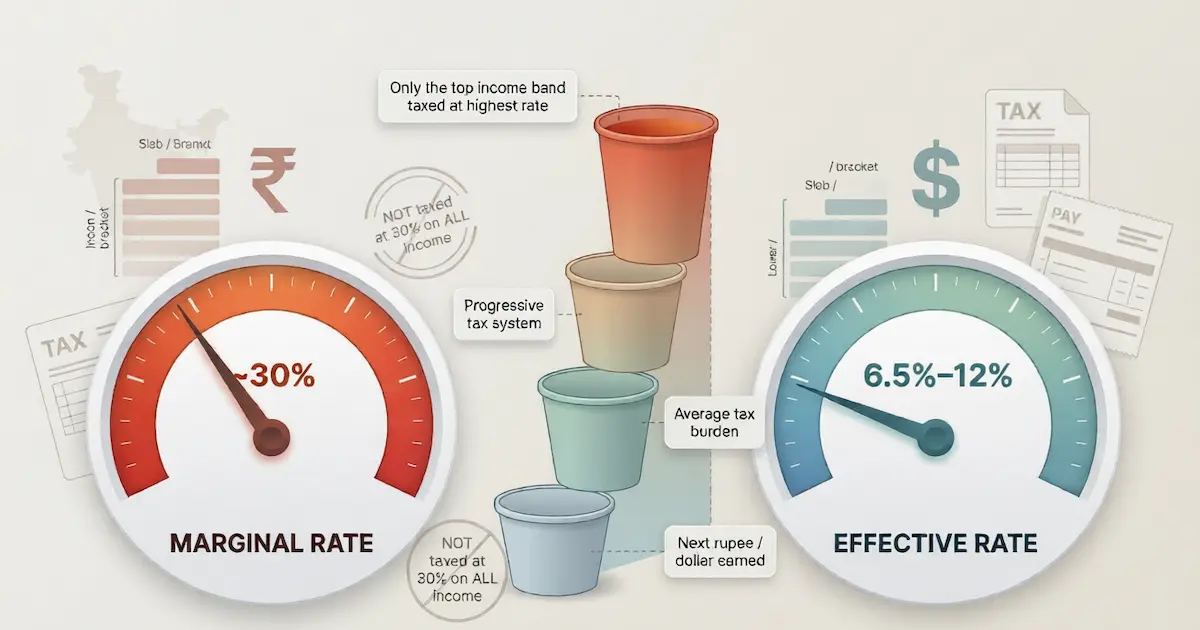

What is the marginal tax rate vs the effective tax rate? Two related but distinct concepts in progressive tax systems. Marginal rate is the percentage applied to your next rupee or dollar of income; effective rate is total tax divided by total income. Covers worked examples for India (new regime ₹15L salary at 15% marginal / 6.5% effective) and the US (federal marginal 22% / effective ~12-14% typical), the most common bracket misconception, and why each rate matters for different decisions.

9 min read

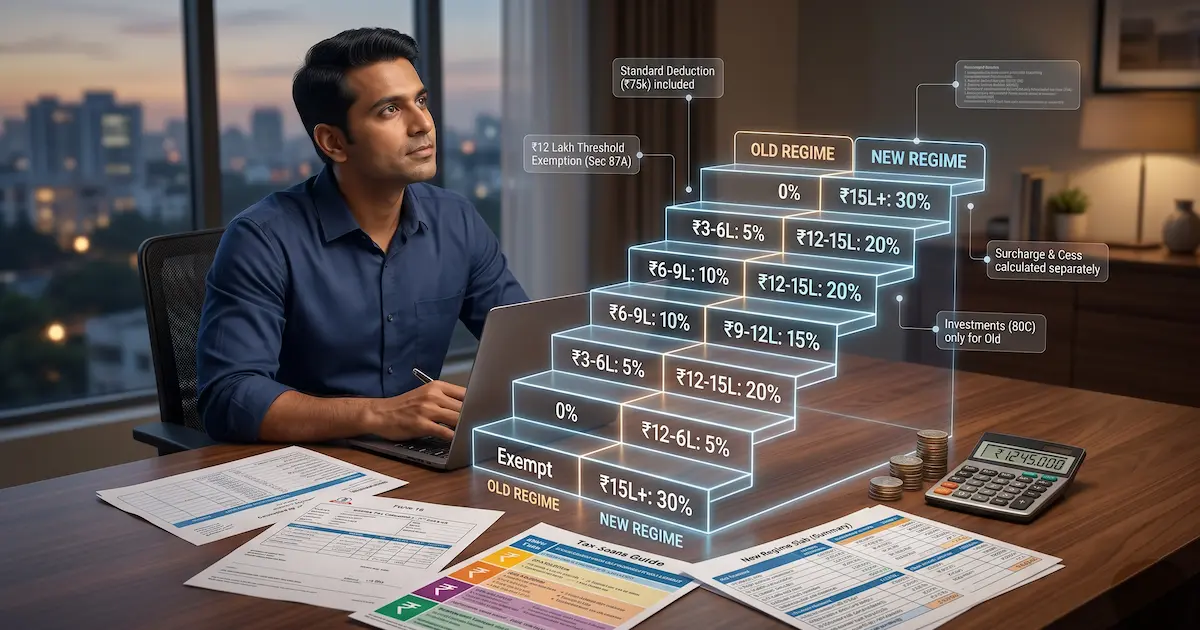

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

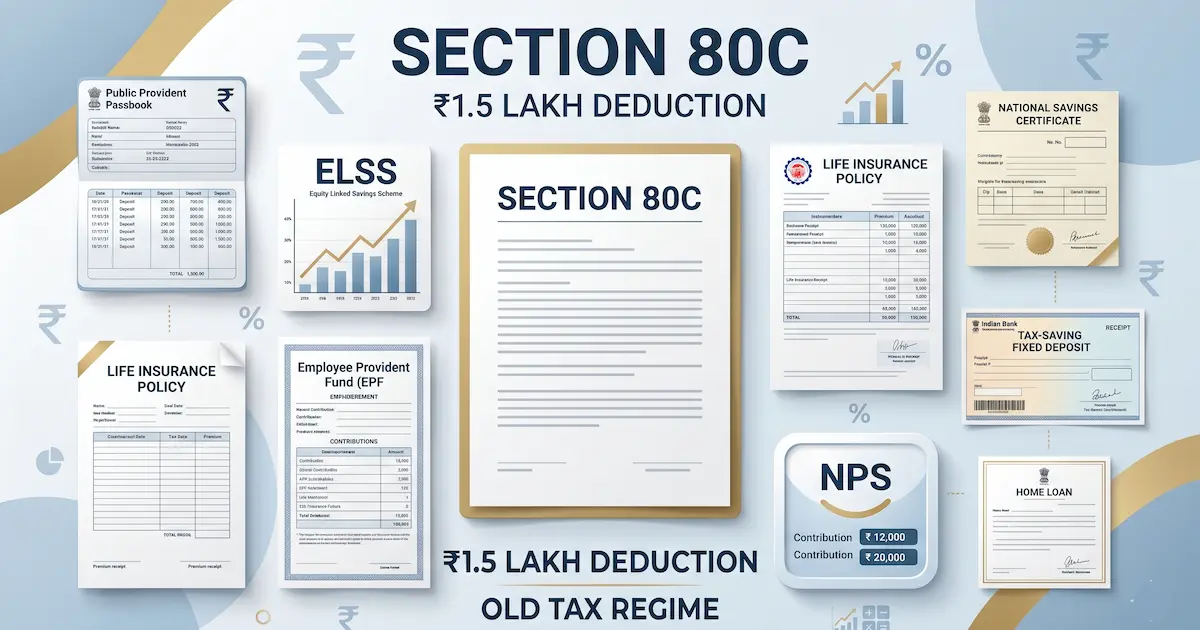

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read