PMJJBY vs PMSBY: Rs 436 Life vs Rs 20 Accident Cover

By Tapabrata Biswas · Updated July 9, 2026 · 14 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

PMJJBY and PMSBY are the two cheapest insurance products in India: Rs 436 a year for Rs 2 lakh of life cover, and Rs 20 a year for Rs 2 lakh of accident cover. Hold both and you pay Rs 456 a year for up to Rs 4 lakh of protection, roughly a tenth of what an equivalent private life-plus-accident bundle costs. The government launched them together on 9 May 2015 under the Pradhan Mantri Jan Suraksha Yojana, aimed at the crores of Indians who never had access to insurance through a job.

This walks through what each scheme is, who can join, the exact premiums and where the money goes, the 30-day lien that trips up new joiners, how claims work, the tax angle, and how the two fit together. It is educational, not insurance advice; for cover matched to your own family and finances, an IRDAI-registered adviser is the right person to ask.

What is the difference between PMJJBY and PMSBY?

PMJJBY is life insurance that pays on death from any cause, while PMSBY is accident insurance that pays only when death or disability is caused by an accident. That single split explains everything else about the two schemes, including why one costs Rs 436 and the other just Rs 20.

| Scheme | Full name | What it covers | Annual premium |

|---|---|---|---|

| PMJJBY | Pradhan Mantri Jeevan Jyoti Bima Yojana | Life cover, Rs 2 lakh on death from any cause | Rs 436 |

| PMSBY | Pradhan Mantri Suraksha Bima Yojana | Accident cover, Rs 2 lakh accidental death or disability | Rs 20 |

The reason PMSBY is so much cheaper is simple: accidental death is far rarer than death from all causes combined, so the insurer's expected payout per member is tiny. PMJJBY, which pays whether you die in a crash or from a heart attack at 54, carries far more risk and prices it at Rs 436. Both are one-year covers with no maturity value: if you live through the year, the premium is spent and nothing comes back, exactly like any term policy.

What is PMJJBY?

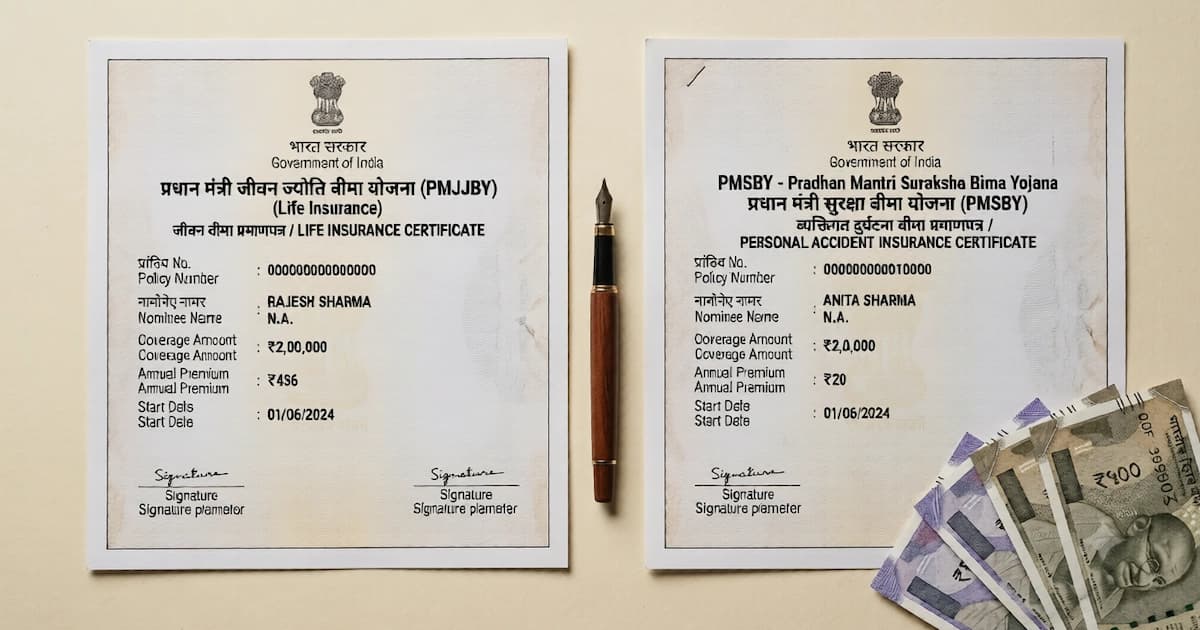

PMJJBY (Pradhan Mantri Jeevan Jyoti Bima Yojana) is a government-backed term life scheme that pays your nominee Rs 2 lakh if you die from any cause, for a premium of Rs 436 a year. It runs through LIC and other life insurers tied up with banks and post offices.

| Parameter | PMJJBY rule |

|---|---|

| Cover amount | Rs 2,00,000 on death from any cause |

| Annual premium | Rs 436 (raised from Rs 330 on 1 June 2022) |

| Entry age | 18 to 50 years |

| Cover continues to | Age 55, with unbroken annual renewal |

| Waiting (lien) period | 30 days for new joiners (accidental death covered from day 1) |

| Cover period | 1 June to 31 May, auto-debit by 31 May |

| Insurers | LIC and empanelled life insurers |

Where does the Rs 436 actually go? Of it, Rs 395 is the insurer's premium, Rs 30 is a commission to the bank correspondent (charged on new enrolments only), and Rs 11 is the bank's administrative fee. There's a small saver's trick here: enrol yourself online through net banking and the Rs 30 correspondent commission is dropped and passed back to you as a lower premium.

Joining mid-year costs less, on a pro-rata basis: the full Rs 436 for a June-to-August start, about Rs 342 for September to November, Rs 228 for December to February, and Rs 114 for March to May.

The 30-day lien is the rule new joiners miss most. For anyone enrolling for the first time, death from any cause other than an accident is not payable in the first 30 days. Accidental death is covered from day one. The lien exists to stop someone enrolling right after a terminal diagnosis, and it resets if you lapse and rejoin later.

A quick example makes it concrete. Say a 35-year-old enrols on 15 March 2026. The 30-day lien runs to 14 April 2026. Die in a road accident on 10 April and the Rs 2 lakh is paid; die of a heart attack on the same day and no claim is admissible. From 15 April onward, both causes are covered.

What is PMSBY?

PMSBY (Pradhan Mantri Suraksha Bima Yojana) is a government-backed personal accident scheme that pays up to Rs 2 lakh for accidental death or disability, for a premium of Rs 20 a year. It is run through public-sector and private general insurers.

| Parameter | PMSBY rule |

|---|---|

| Accidental death or total permanent disability | Rs 2,00,000 |

| Partial permanent disability | Rs 1,00,000 |

| Annual premium | Rs 20 (raised from Rs 12 on 1 June 2022) |

| Entry age | 18 to 70 years |

| Cover period | 1 June to 31 May, auto-debit by 31 May |

| Waiting period | None |

| Insurers | Public-sector and private general insurers |

That Rs 20 buys Rs 2 lakh of accidental-death cover, which is about as cheap as insurance gets anywhere. The full Rs 2 lakh also applies to total permanent disability: irrecoverable loss of both eyes, both hands or feet, or one eye plus one limb. The Rs 1 lakh partial-disability payout covers the loss of one eye, or the use of one hand or foot.

PMSBY does not pay for everything, though. It excludes self-inflicted injury and suicide, war and civil unrest, and death or disability while mountaineering, racing, hunting, or doing hazardous adventure sports, along with incidents under the influence of alcohol or non-prescribed drugs. Ordinary accidents, the road crash, the fall, the drowning, the workplace injury, the fire, are covered, which is the risk most working adults actually face.

Can I hold both PMJJBY and PMSBY together?

Yes, and holding both is the point: for Rs 456 a year the two schemes stack to pay up to Rs 4 lakh on an accidental death. They cover different risks, so their payouts add up.

| Event | Pays out | Amount |

|---|---|---|

| Death by illness or natural cause | PMJJBY | Rs 2,00,000 |

| Death by accident | PMJJBY plus PMSBY | Rs 4,00,000 |

| Total permanent disability (accident) | PMSBY | Rs 2,00,000 |

| Partial disability (accident) | PMSBY | Rs 1,00,000 |

The accidental-death case is where the two combine: PMJJBY pays because a death occurred, PMSBY pays because it was an accident, and the nominee receives Rs 4 lakh. For scale, a Rs 4 lakh term policy from a private insurer for a healthy 35-year-old typically runs Rs 2,000 to Rs 4,000 a year, so the Rs 456 pair is close to a tenth of the cost for the same accidental-death figure. The trade-off, of course, is that Rs 2 lakh is a modest sum today; these schemes are a floor, not a full financial plan.

How do I enrol and renew?

You enrol in either scheme through a participating bank or post office by giving one consent form and authorising auto-debit from your savings account. No medical test is needed; an Aadhaar-linked account is the only real requirement.

The steps are short: pick a bank or post office where you hold a savings account, give the enrolment and auto-debit consent (at a branch, through net banking, or via the India Post Payments Bank app), and the annual premium is pulled in one instalment. Cover runs 1 June to 31 May, and the mandate has to be in place by 31 May. Renewal is automatic each year as long as the account has enough balance on the debit date and you are still within the age window.

Two rules catch people out. First, if the balance is short on the debit date, the cover lapses for the year; you can rejoin later by paying the premium, but PMJJBY then treats it as fresh cover with a new 30-day lien. Second, only one PMJJBY and one PMSBY cover pays out per person. Enrol from three different bank accounts and you do not get three payouts: the cover is capped at one Rs 2 lakh sum, and the duplicate premiums are refunded.

How do claims work for each scheme?

A PMJJBY claim needs a death certificate and the claim form; a PMSBY accident claim additionally needs an FIR and either a post-mortem report or a disability certificate. In both cases the nominee starts at the bank that holds the linked account.

For PMJJBY, the nominee submits the claim-cum-discharge form, the original death certificate, and their own KYC and bank details to the bank, which forwards it to the insurer (LIC for most accounts). If no nominee was named, the payout goes to the legal heir on production of a succession certificate.

For PMSBY, an accidental-death claim adds the police FIR or panchnama and the post-mortem report; a disability claim adds a disability certificate from a government civil surgeon. The extra documents exist because the insurer has to establish that an accident, and not illness, caused the loss.

The timeline is the same simple chain for both: file within 30 days of the event, the bank forwards to the insurer within 30 days, and the insurer settles within 30 days of receiving complete papers. Small, standardised payouts are what let these schemes skip the long investigation a large private policy would trigger.

Are PMJJBY and PMSBY premiums tax-deductible?

The PMJJBY premium is a life-insurance premium, so it can generally be claimed as a Section 80C deduction under the old tax regime, and the death benefit is exempt under Section 10(10D). PMSBY's Rs 20 accident premium is too small to matter for most people and its deductibility is less settled.

For the typical subscriber, whose income sits below the taxable threshold, the deduction is beside the point; what matters is that the Rs 2 lakh or Rs 4 lakh reaches the family tax-free. Because the treatment depends on your regime (the new regime, now the default, does not allow 80C) and your specific situation, a Chartered Accountant is the right person to confirm it before you rely on it.

How many people use these schemes?

As of 23 April 2025, PMJJBY had 23.63 crore cumulative enrolments and PMSBY had 51.06 crore, with thousands of crores already paid to families. These are not small pilot programmes; they are among the largest insurance pools in the world by member count.

By the government's ten-year Jan Suraksha review, PMJJBY had paid about Rs 18,398 crore across 9,19,896 claims, and PMSBY had paid about Rs 3,121 crore across 1,57,155 claims (PIB, 2025). The gap between the two enrolment numbers is telling: PMSBY's Rs 20 price pulls in far more sign-ups, while PMJJBY's larger payouts show up in a much bigger total claim figure on fewer claims.

What this post does not cover

This explains the two insurance schemes; it does not tell you whether Rs 2 lakh is enough cover for your family, which is a personal-planning question an IRDAI-registered adviser should answer. It also leaves the third Jan Suraksha scheme, the guaranteed-pension Atal Pension Yojana, to its own guide rather than repeating its contribution slabs here. And it does not track bank-by-bank online enrolment steps, which differ across net-banking apps.

Frequently asked questions

What is the difference between PMJJBY and PMSBY? PMJJBY is a life insurance scheme that pays Rs 2 lakh to your family on death from any cause, for a premium of Rs 436 a year. PMSBY is an accident insurance scheme that pays Rs 2 lakh for accidental death or total permanent disability, and Rs 1 lakh for partial disability, for Rs 20 a year. PMJJBY covers every kind of death after a 30-day waiting period; PMSBY covers only accidents, with no waiting period. The two are meant to be held together for Rs 456 a year.

What is the premium and cover for PMJJBY and PMSBY? PMJJBY costs Rs 436 a year for Rs 2 lakh of life cover; PMSBY costs Rs 20 a year for Rs 2 lakh of accidental death or total disability cover (Rs 1 lakh for partial disability). Both premiums were revised on 1 June 2022, PMJJBY up from Rs 330 and PMSBY up from Rs 12. Of the PMJJBY Rs 436, Rs 395 is the insurer's premium, Rs 30 is a bank-correspondent commission on new enrolments, and Rs 11 is the bank's admin fee; enrol yourself online and the Rs 30 is waived.

Can I hold both PMJJBY and PMSBY at the same time? Yes, and most subscribers do. Both are separate schemes linked to the same savings account, so you can enrol in both for a combined Rs 456 a year. Together they pay up to Rs 4 lakh on an accidental death, Rs 2 lakh from PMJJBY (any-cause death) plus Rs 2 lakh from PMSBY (accident). Only one PMJJBY and one PMSBY cover pays out per person, even if the premium is debited from several of your bank accounts.

Is there a waiting period on PMJJBY? Yes. PMJJBY has a 30-day lien period for first-time enrollees during which death from any cause other than an accident is not payable. Accidental death is covered from day one. After the 30 days, death from any cause, including illness and natural causes, is covered. If your cover lapses and you rejoin later, a fresh 30-day lien applies. PMSBY, being accident-only, has no waiting period.

Who can join PMJJBY and PMSBY? PMJJBY is open to holders of a savings bank or post office account aged 18 to 50; once enrolled, cover continues with annual renewal up to age 55, but you cannot first join after 50. PMSBY is open to ages 18 to 70. Both need an Aadhaar-linked savings account and consent to auto-debit the premium by 31 May each year for the 1 June to 31 May cover period.

The bottom line

PMJJBY and PMSBY are complementary: one pays Rs 2 lakh on any death for Rs 436 a year, the other pays Rs 2 lakh on an accidental death or disability for Rs 20 a year, and held together for Rs 456 they stack to Rs 4 lakh on an accidental death. Both run off a savings account with an annual auto-debit, both were repriced on 1 June 2022, and both keep claims simple enough to settle in weeks.

Two facts are worth carrying away, because most write-ups get them wrong. PMJJBY's waiting period is 30 days, not 45, and only accidental death is paid inside it. And enrolling from five bank accounts still gets you one payout, not five, so pick one account per scheme and keep it funded before 31 May.

For the third Jan Suraksha scheme, the guaranteed-pension Atal Pension Yojana, see its own guide. For how these sit among India's other government schemes, see Employee Provident Fund (EPF), Public Provident Fund (PPF), and our Indian government savings schemes overview.

Sources

- Department of Financial Services, Ministry of Finance, Pradhan Mantri Jeevan Jyoti Bima Yojana, financialservices.gov.in/beta/en/pmjjby

- Pradhan Mantri Jan Suraksha Yojana, PMJJBY revised rules (w.e.f. 1.6.2022), jansuraksha.gov.in/Files/PMJJBY/English/Rules.pdf

- Pradhan Mantri Jan Suraksha Yojana, PMSBY rules (w.e.f. 1.6.2022), jansuraksha.gov.in/Files/PMSBY/English/Rules.pdf

- Press Information Bureau, 10 years of Jan Suraksha (enrolment and claims data, 2025), pib.gov.in

- Income Tax Department of India, Section 80C and Section 10(10D), incometax.gov.in

You might also like

What is Atal Pension Yojana? The guaranteed monthly pension of ₹1,000-₹5,000 at age 60, eligibility for unorganized-sector workers aged 18-40, monthly contribution table, and how APY differs from NPS.

9 min read

What is EPF (Employee Provident Fund)? The 8.25% interest rate, mandatory 12%+12% employee/employer contribution, EPS split, withdrawal rules, and tax treatment explained for salaried Indian workers.

9 min read

PPF pays 7.1% for Jul-Sep 2026, unchanged since 2020. See the Rs 500 to Rs 1.5 lakh limits, EEE tax, 15-year lock-in, withdrawal rules and a maturity example.

13 min read