What Is a Recession? Definition, and Who Declares It

By Tapabrata Biswas · Updated July 14, 2026 · 15 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

"Recession" is one of those words that gets used long before it's official. By the time a committee of economists formally confirms one, it has usually been underway for months, and sometimes it's already over. Stranger still, people can't even agree on what the word means: in 2022 a dispute over the definition got heated enough that Wikipedia had to lock its recession page. That gap between the felt experience and the formal label is the source of most of the confusion around the term.

This explains what a recession actually is, why the popular "two quarters of shrinking GDP" line isn't the official US definition, who declares one and how late, how it differs from a depression, what tends to happen during one, and India's own recession history. It explains the concept. It doesn't forecast any economy's next downturn, and it isn't advice on what to do with your money if one arrives.

What is a recession?

A recession is a significant, broad-based decline in economic activity that lasts more than a few months, visible across real GDP, employment, income, and spending all at once. The key words are "broad-based" and "lasts more than a few months." A bad quarter in one industry isn't a recession. A downturn that spreads across the whole economy and persists is.

That breadth is what separates a recession from an ordinary wobble. Output slows, but so does hiring, and household income, and consumer spending, each feeding the others. Because the decline shows up in several measures at once, economists treat a recession as a turning point in the business cycle, the recurring pattern of expansion and contraction every economy moves through. The opposite phase, an expansion, is when those same measures rise together.

A recession is also a normal, recurring feature of how economies work. It isn't a one-off catastrophe. The US has had more than a dozen since World War II. Each ends, an expansion follows, and the cycle continues. One quick disambiguation, since the word has a life outside economics: the "recession" that means gum or gum-line recession, or a receding hairline, is an unrelated use. This page is entirely about the economic sense.

Is a recession two quarters of negative GDP?

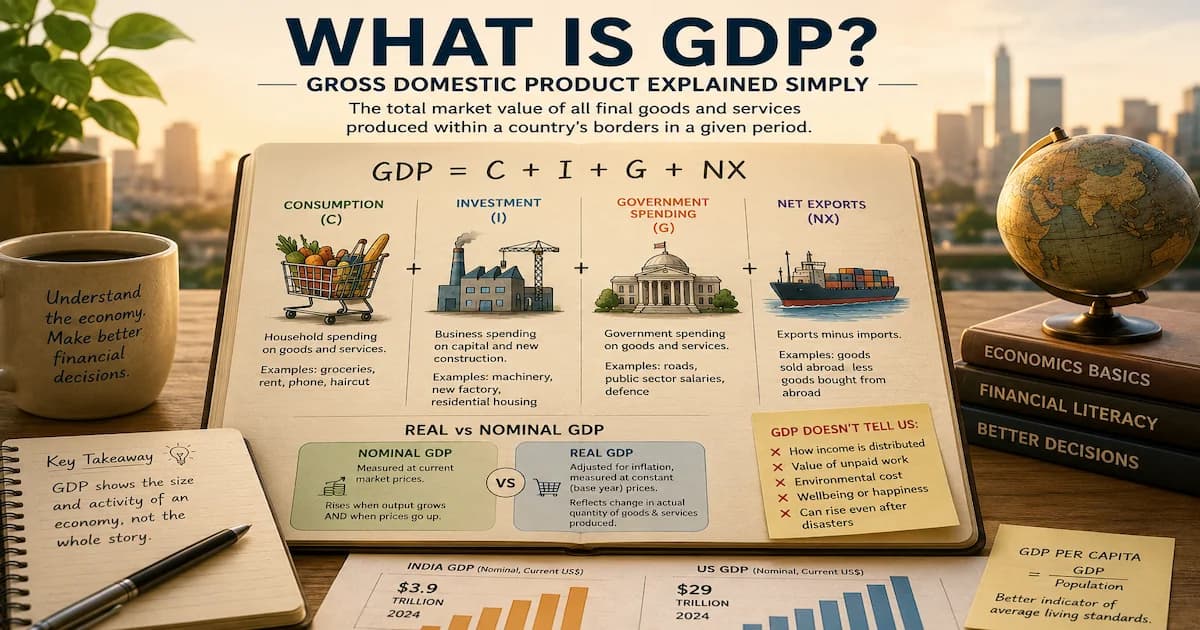

Two consecutive quarters of falling real GDP is a rule of thumb, not the official US definition of a recession. You'll hear the two-quarters line constantly, and it's a useful shorthand, but in the US it carries no official weight.

Here's the twist most explainers miss: the rule is a matter of geography. The two-quarter test is the standard or official definition in the UK, Canada, and India, which have no dedicated body to make a broader judgment call. In the US, it isn't. That single difference explains a lot of cross-border confusion, because an American headline and an Indian headline can use the same word to mean two technically different things.

The rule is popular because it's simple and objective. Take real GDP, the inflation-adjusted measure of output explained in what is GDP, and check whether it fell for two quarters running. The weakness is that it looks only at GDP and ignores jobs and income. It can flag a brief technical dip nobody experiences as a recession, and it can miss a genuine one that doesn't line up into two tidy negative quarters. The 2020 US downturn is the clearest case: it was so sharp and so short that it didn't fit the two-quarter pattern, yet almost no one would deny it was a recession.

Who decides when the US is in a recession?

In the US, the National Bureau of Economic Research (NBER) officially identifies and dates recessions, through a group called the Business Cycle Dating Committee. It's a private, non-partisan research organization outside the government, and its dates are the ones economists and historians treat as authoritative.

The committee doesn't lean on a single GDP rule. It weighs three things: the depth of the decline, how widely it diffuses across the economy, and how long it lasts. Its own wording is that extreme readings on one of those can partly offset weaker readings on another. It leans most on monthly indicators such as employment, real personal income, and industrial production, more than on quarterly GDP alone. From these it marks two points, the peak (the last month before activity turned down) and the trough (the low point before recovery began). The span between them is the recession.

The catch is timing. The committee dates recessions in hindsight, once enough revised data has arrived to be confident, so its announcements land well after the fact. The lag has run from as little as 4 months to as long as 21 months. The February 2020 peak was announced in June 2020; the March 1991 trough wasn't announced until December 1992. The practical consequence is worth saying plainly: in the US, a recession is frequently confirmed only after it has already ended. The committee would rather be late and correct than fast and wrong.

Did the definition of a recession change in 2022?

No. The definition did not change in 2022, despite a widely shared claim that it had. The episode is a useful lesson in exactly why the two-quarters rule and the official definition are not the same thing.

In late July 2022, US GDP had fallen for a second straight quarter (the second-quarter reading came in at about minus 0.9% annualized). Ahead of that release, a White House blog post pointed out that two negative quarters is not the official definition and that the NBER is the body that makes the call. Critics said the administration was rewriting the meaning of "recession" to avoid a politically damaging label. Fact-checkers disagreed. PolitiFact rated the "changed the definition" claim false, noting the two-quarter threshold was never the official US designation and the NBER definition long predates the dispute.

The fight spilled onto Wikipedia. Its recession article drew a burst of editing that week, far above its normal volume, as anonymous editors tried to elevate the two-quarters line, and administrators semi-protected the page until August 3, 2022. The lasting takeaway isn't political. It's that "are we in a recession" often has no clean yes-or-no answer in real time, because the official arbiter deliberately waits, and the popular shortcut and the official definition can point in different directions.

Recession vs depression vs stagflation vs slowdown

These four terms describe different economic conditions, and only one of them, a depression, is simply a worse recession. The words get used loosely, so a clean comparison helps.

| Term | What it is | Rough marker |

|---|---|---|

| Recession | Broad decline in activity across the economy | Lasts more than a few months; US avg about 10 to 11 months |

| Depression | A severe, prolonged recession | Informally, GDP down more than ~10% or lasting 3 to 4 years |

| Stagflation | High inflation and weak growth or high unemployment together | No fixed threshold; the 1970s oil-shock era is the reference |

| Slowdown | Growth that is still positive but decelerating | GDP still rising, just more slowly; not a contraction |

A depression has no official numeric threshold, only an informal one that recurs across sources: a GDP fall beyond roughly 10%, or a contraction dragging on for three to four years. The Great Depression of the 1930s is the benchmark, with US output down about a quarter and unemployment near 25% over several years. Set that against the 2008 to 2009 Great Recession, where GDP fell about 4.3% over 18 months. Stagflation is a separate problem again, because it pairs a stagnant economy with rising prices, which is painful precisely because the usual cure for one worsens the other. A slowdown isn't a recession at all: the economy is still growing, just at a slower pace.

What causes a recession?

Recessions are triggered by shocks to demand or supply, and no single cause fits every one. A few patterns recur across the downturns economists have studied.

- A sharp drop in demand, when households and businesses suddenly cut spending. Since US consumer spending is roughly 70% of the economy, a confidence shock spreads fast.

- An asset bubble bursting, when prices in housing or stocks rise faster than fundamentals justify and then collapse.

- Tight monetary policy, when a central bank raises interest rates to fight inflation and higher borrowing costs cool activity more than intended.

- A supply shock, such as a spike in oil or commodity prices that raises costs across the economy at once.

- A financial crisis or external event, from a banking collapse to a pandemic.

The 2008 recession is the textbook example of two of these at once: a housing bubble inflated by loose lending, followed by a subprime-mortgage collapse that became a full financial crisis. The COVID recession of 2020 was the external-shock case, a sudden stop imposed from outside the normal cycle. Because the causes differ, so do the shapes: some recessions build slowly, others arrive almost overnight.

How do economists spot a recession early?

Economists watch a handful of leading indicators, though none of them predicts a recession with certainty. Two get the most attention, and it's worth understanding both what they signal and how often they cry wolf.

The first is the inverted yield curve. Normally, long-term government bonds pay more than short-term ones. When that flips, so short-term yields exceed long-term yields, the curve is "inverted," and a 10-year-minus-2-year inversion has preceded essentially every US recession since the 1950s. The 10-year-minus-3-month version is the one many Fed researchers favor. The honest caveat is that it isn't infallible: it gave false alarms in the mid-1960s and late 1990s, and the inversion that began in 2022 had not been followed by a recession about two and a half years later.

The second is the Sahm rule, created by economist Claudia Sahm in 2019. It signals that a recession has likely begun when the three-month average of the unemployment rate rises half a percentage point or more above its lowest point in the previous 12 months. It's a confirmation tool more than a forecast, since it triggers near the onset. As of mid-2026 it had not triggered, sitting well below the 0.5-point threshold. Both indicators describe probabilities, not destiny, which is why this page explains them without forecasting anything.

What happens in a recession, and how does it affect you?

A recession is felt through a chain of effects: falling demand leads to job cuts, which lowers income, which cuts spending further. No two recessions are identical, but the loop is consistent, and it's what makes a downturn self-reinforcing until something breaks the cycle.

Several things tend to move together once that loop takes hold:

- Unemployment rises, often sharply. It's a lagging indicator, so it can keep climbing even after the recession has technically ended.

- Consumer and business spending contract, especially on big-ticket and postponable purchases.

- Central banks usually cut interest rates to make borrowing cheaper, the interest-rate lever that tends to move opposite to the direction it takes when inflation is the problem.

- Stock markets frequently fall, though market moves and recessions don't line up neatly, because markets price expectations ahead of the official data.

- Home values and rents can soften as demand weakens, though housing is regional and doesn't always follow the wider cycle.

For an ordinary household, the recession shows up as job risk, slower raises, and less certain income, arriving exactly when fixed costs don't budge. Variable-rate borrowers can catch a small break if rates fall, while anyone relying on savings interest earns less. This is why an emergency fund is the personal-finance buffer most discussed alongside downturns: the mechanics of building one are covered in how to build an emergency fund. The point here is descriptive. A recession raises the odds of income disruption, which is the risk a cash buffer is designed to absorb.

Recent US recessions

The clearest way to ground the definition is with the dates the NBER has actually assigned. Four recent US recessions, with their official peak-to-trough spans:

| Recession | NBER dates | Length | Peak unemployment (BLS) |

|---|---|---|---|

| COVID-19 | Feb 2020 to Apr 2020 | 2 months | 14.7% (April 2020) |

| Great Recession | Dec 2007 to Jun 2009 | 18 months | 10.0% (October 2009) |

| Dot-com | Mar 2001 to Nov 2001 | 8 months | 6.3% (June 2003) |

| Early 1990s | Jul 1990 to Mar 1991 | 8 months | 7.8% (June 1992) |

Two of these stand out. The 2020 recession was the shortest in US records, just two months, yet it drove unemployment to 14.7% in April 2020, the highest rate in the post-war series, per the US Bureau of Labor Statistics. The 2008 to 2009 Great Recession was the deepest since World War II, with real GDP falling about 4.3% from peak to trough and unemployment peaking at 10% in October 2009. The contrast shows why duration and depth are separate questions: a short recession can still be severe, and the official dates capture both.

Has India ever had a recession?

Yes. India entered its first technical recession in its history during the COVID shock, in the first half of FY2020-21. GDP shrank about 24% in the April to June 2020 quarter and about 7.5% in the July to September 2020 quarter, two straight contractions that met the technical-recession test.

The call itself made history. In November 2020, the Reserve Bank of India flagged the downturn in its first-ever published "nowcast," writing that India had entered a technical recession for the first time. That framing matters because of how India measures these things. Official GDP figures are produced by the Ministry of Statistics and Programme Implementation (MoSPI) through the National Statistical Office, and the RBI provides forecasts and nowcasts, but India has no NBER-equivalent committee that formally dates recessions the way the US does. So India defaults to the two-consecutive-quarters convention, which is exactly why the 2020 episode is called a technical recession, with no dating body formally declaring it. In Hindi, the word for recession is मंदी (mandi), literally a slump or slowdown. India's recovery was quick: growth turned positive again in the quarter that followed.

What this post does not cover

This is a plain-English explainer of what a recession is, how it's defined and dated, and how it has played out in the US and India. It isn't a prediction of whether or when any economy will enter a recession, and it isn't guidance on how to "recession-proof" your finances, position investments, or change jobs ahead of a downturn. It doesn't interpret current economic data or any specific country's live outlook. For decisions that depend on the economic outlook, an economist or a qualified financial professional is the right source.

Frequently asked questions

Is a recession two quarters of negative GDP? Not in the US. Two consecutive quarters of falling real GDP is a popular rule of thumb, but it is not the official US definition. In the US the National Bureau of Economic Research (NBER) defines a recession more broadly as a significant, widespread decline in activity that lasts more than a few months and shows up in employment, income, and spending as well as GDP. The two-quarter test IS the official or standard definition in the UK, Canada, and India, which have no NBER-equivalent body. The 2020 US recession shows the gap: it was too short to produce two straight negative quarters of the usual kind, yet it was unmistakably a recession.

Who decides when a recession starts in the US? The NBER's Business Cycle Dating Committee decides, and it does so in hindsight. The committee weighs the depth, diffusion, and duration of a decline across monthly indicators such as employment, real personal income, and industrial production, then marks the peak (the last month before the decline) and the trough (the low before recovery). Because it waits for revised data, the call usually lands months late. Its announcement lag has ranged from 4 months to 21 months, so a US recession is often confirmed only after it has already ended.

Did the definition of a recession change in 2022? No. In July 2022, after two straight quarters of negative US GDP, a White House blog post noted that two quarters is not the official definition and that the NBER is the arbiter. Critics said the administration had redefined recession, but fact-checkers including PolitiFact rated that false: the two-quarter threshold was never the official US designation, and the NBER definition long predates 2022. Wikipedia's recession page saw such an editing battle that week that editors semi-protected it until August 3, 2022.

What is the difference between a recession and a depression? A depression is a much deeper and longer version of a recession, and there is no official numeric line separating them. An informal benchmark that shows up across sources is a GDP decline of more than about 10% or a downturn lasting three to four years. The reference point is the Great Depression of the 1930s, when US output fell by roughly a quarter and unemployment reached about 25%. By comparison, the 2008 to 2009 Great Recession, the deepest since World War II, saw GDP fall about 4.3% and unemployment peak at 10%.

How long do recessions usually last? Most modern US recessions have been fairly short. The average post-World-War-II recession has lasted roughly 10 to 11 months, according to NBER dating. The 2008 Great Recession ran 18 months, the longest of that era, while the 2020 recession lasted just two months, the shortest on record. Expansions, the growth phases between recessions, tend to last much longer than the recessions that interrupt them.

Has India ever had a recession? Yes, once by the technical measure. India entered its first technical recession in its history in the first half of FY2020-21, during the COVID shock, when GDP shrank about 24% in the April to June 2020 quarter and about 7.5% in July to September 2020. The RBI flagged it in November 2020 in its first-ever published nowcast. India has no NBER-equivalent body that formally dates recessions; official GDP figures come from the Ministry of Statistics (MoSPI / NSO), and India relies on the two-consecutive-quarters test, which is why the 2020 episode is called a technical recession. In Hindi, recession is मंदी (mandi).

Sources

- National Bureau of Economic Research, Business Cycle Dating and dating-procedure FAQ (nber.org)

- US Bureau of Economic Analysis, How is a recession defined? (bea.gov)

- US Bureau of Labor Statistics, Labor Force Statistics (unemployment rate) (bls.gov)

- PolitiFact, No, the White House didn't change the definition of recession (2022) (politifact.com)

- Reserve Bank of India, first-ever nowcast flagging a technical recession (Nov 2020) (business-standard.com)

- Federal Reserve History, The Great Recession of 2007-09 (federalreservehistory.org)

You might also like

India reports GDP growth year-on-year over a fiscal year. The US annualises one quarter. The two headline numbers are built differently and do not compare.

15 min read

What is inflation? A plain-English explanation of how prices rise, how it is measured, and what it actually means for everyday savings, wages, and debt.

9 min read

How to build an emergency fund from scratch, the four-stage path from $0 to a fully-funded six-month buffer, and what to do at each stage when life interrupts.

9 min read