Financial Literacy: What the Data Says, and Where to Start

By Tapabrata Biswas · Updated July 20, 2026 · 17 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

India's official financial literacy rate is 27.18%. That figure comes from fieldwork that finished in October 2019.

Seven years. The survey behind it runs on a five-yearly cadence, so a new wave was due around 2024 and none has appeared. The national strategy that promised one expired at the end of 2025 without a successor. And when a member of the Rajya Sabha asked for the rate in March 2025, the written reply declined to state a percentage at all and referred to the survey as a 2017 exercise.

That absence is the most interesting fact in Indian financial-literacy data, and no page we read mentions it. Of thirteen pages ranking for these terms, none gives an India figure of any kind.

The US side has a different problem. The current measurement was published in June 2026, and none of the thirteen pages carries it either. They're running on the previous year's wave, or on statistics from 2017 and 2018 under a 2025 update stamp.

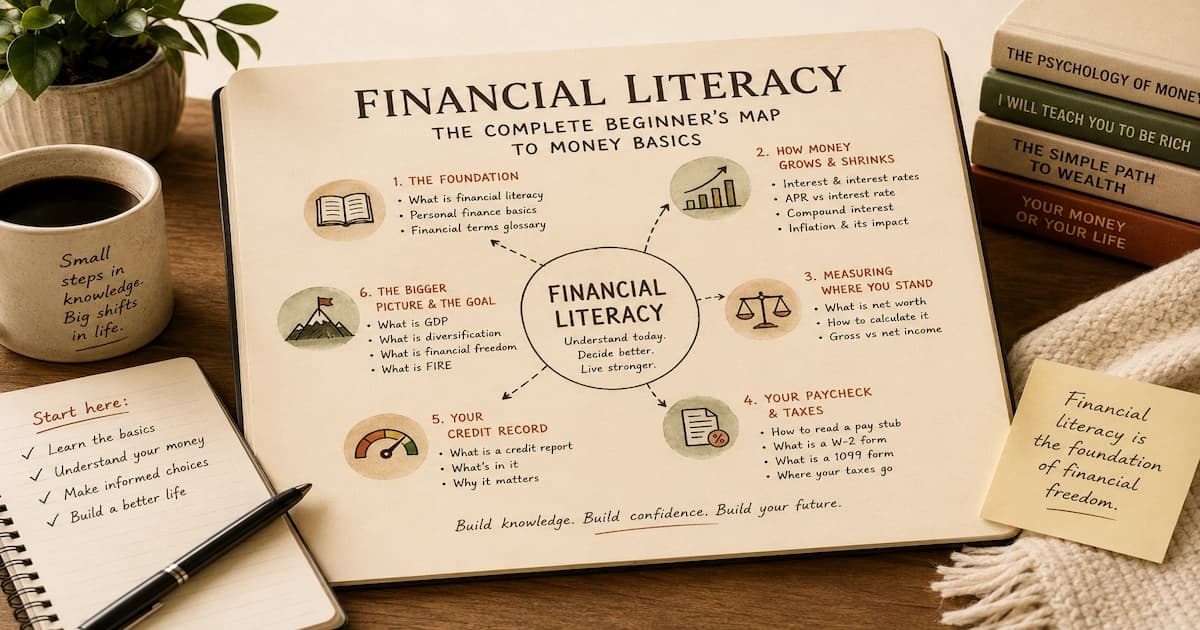

So this page does two things. It states what the evidence actually says, with the fieldwork year attached to every number, and it routes to the explainers underneath. For what financial literacy means as a concept, our definition explainer owns that ground. For the full beginner sequence, what to do first and in what order, our complete personal finance guide for beginners lays out the whole roadmap.

How financially literate are people, actually?

No single current global figure exists, and the numbers that circulate as though one does are mostly a decade old. Here's what each live measurement says, with the year the data was collected, which is often not the year it was published.

| Measurement | Fieldwork | Published | Finding |

|---|---|---|---|

| TIAA Institute-GFLEC P-Fin Index | 2026 | Jun 2026 | US adults answered 47% of questions correctly |

| FINRA National Financial Capability Study | 2024 | Jul 2025 | 27% of US adults got at least 5 of 7 right |

| NCFE Financial Literacy and Inclusion Survey (India) | Jun 2018 to Oct 2019 | 2020 | 27.18% financially literate |

| OECD/INFE Adult Financial Literacy | Aug to Dec 2023 | Dec 2023 | 60 out of 100 across all participating economies |

| PISA financial literacy (15-year-olds) | 2022 | Jun 2024 | 18% below baseline proficiency |

| S&P Global FinLit Survey | 2014 | Nov 2015 | 33% of adults worldwide, 57% US, 24% India |

Two things stand out from that table.

The US number has barely moved in a decade. The P-Fin Index has run ten annual waves and reports that the figure has never exceeded 52%. A decade of financial-education initiatives, and the needle sits where it sat.

The most-quoted global statistic is the oldest thing on the list. The S&P survey's "about a third of adults worldwide" gets cited constantly. It was fielded in 2014 and has never been repeated.

And the student measurement is about to go quiet for years. PISA dropped financial literacy from its 2025 cycle, which means the next international measurement of teenagers is PISA 2029, reporting around 2031.

Why is India's number seven years old?

Because the survey that produces it has not been repeated on schedule, and the strategy that promised a successor has expired.

The NCFE Financial Literacy and Inclusion Survey is a serious instrument. Fieldwork ran June 2018 to October 2019 across 75,140 adults aged 18 to 80, covering all 35 states and union territories, with a nationally representative design. Its scoring follows OECD methodology: a person counts as financially literate with a combined score of at least 15 out of 22, subject to minimums of 3 in financial attitude, 6 in financial behaviour and 6 in financial knowledge.

The component breakdown is more useful than the headline:

| Component | Score |

|---|---|

| Financial attitude | 89% |

| Financial behaviour | 53% |

| Financial knowledge | 49% |

Attitude is nearly universal. Knowledge is where the gap sits. That's a different problem from the one "27% are financially literate" suggests on its own, and it points at explanation as the binding constraint, more than motivation.

Regionally the spread was wide: West 37%, North East 33%, North 32%, South 30%, Central 21%, East 20%, with Odisha at 11%, Sikkim 10% and Chhattisgarh 9%.

The previous wave, in 2013-14, measured 20%. So the trajectory was 20% to 27% over roughly five years, and then the measurement stopped.

RBI restates the 27.18% figure in its National Strategy for Financial Education 2020-2025, which is worth knowing for a specific reason: that is RBI republishing NCFE's survey, and not an independent confirmation. There is one measurement here, cited in two places.

What gets mistaken for a financial literacy rate?

Four Indian figures circulate as literacy rates and none of them is one. Each measures something real, and something different.

| Figure | What it actually measures |

|---|---|

| Financial Inclusion Index, 67.0 for March 2025 | Access to financial services, not understanding of them |

| NCFE mid-term evaluation, published 2025 | Not a national rate. 6,000 of its 10,000 respondents were beneficiaries of NCFE's own programmes, which biases it upward |

| SEBI Investor Survey | People who already invest in securities, not the adult population |

| Any OECD score for India | Doesn't exist. The OECD's 2023 adult survey does not include India |

The mid-term evaluation deserves particular care because it publishes a 2019-versus-2024 comparison that looks like a trend. Comparing a 10,000-person sample weighted toward programme beneficiaries against a nationally representative 75,140-person survey isn't a like-for-like measurement, and treating the difference as progress would be a mistake.

The last row catches people out most often. A full-text search of the OECD's 67-page 2023 report returns zero occurrences of "India." Any page attributing an OECD financial literacy score to India has invented it.

What does financial literacy actually cover?

Six areas account for nearly all of ordinary adult financial life, and the concepts inside them are universal even though the documents and institutions differ by country.

The vocabulary. Most people find the terminology is the barrier, more than the arithmetic. Our dual-market glossary pairs the Indian and American terms directly, because CIBIL and FICO, EPF and 401(k), UPI and ACH describe the same machinery under different names.

How money grows. Compound interest is the mechanism that makes time matter more than rate over long horizons, and it runs identically in rupees and dollars.

How money shrinks. Inflation is the other force that changes what money is worth without anyone doing anything, and it's why idle cash loses ground even when the balance doesn't fall.

Where you stand. Net worth is assets minus liabilities, and it's the single number that summarises a financial position at a point in time.

What your income actually is. A pay stub is where gross pay, deductions and take-home separate, and it's the document most people hold without reading.

What lenders see. A credit report is the record behind a credit score, and the distinction between the record and the number matters more than most summaries suggest.

For the practical five-area view of managing money, as against understanding it, personal finance basics covers that ground.

Where should someone start?

With the vocabulary, then the two forces that move money on their own, then the documents. That order reflects what the NCFE component data suggests: knowledge is the binding constraint, not attitude.

If you're starting from zero, the glossary first. Not because definitions are exciting, but because every other explainer assumes them, and the terminology is where most people actually stall.

If you've just started earning, the pay stub and the credit report, in that order. Both are documents you already have, and both turn abstract concepts into your own numbers, which is where understanding tends to stick.

If you're playing a longer game, compound interest and inflation together. They're a matched pair: one is why money left alone can grow, the other is why money left alone can shrink, and holding both at once is what makes a long horizon legible.

What this post deliberately does not cover

This page reports what the measurements say and routes to the explainers. It doesn't tell anyone what to do with their money, and the statistics exist to describe a state of affairs, never to argue for a course of action.

It doesn't define financial literacy at length. That belongs to what financial literacy is, which carries the formal definitions and the concept itself. Repeating that here would split the same ground across two pages.

Three limits on the figures. Every number carries its fieldwork year on purpose, because publication year and collection year differ by up to two years across these surveys and conflating them is the most common error in this material. India's rate is seven years old and we have said so, without presenting it as current. And no forward-looking claim appears about when a new Indian wave might arrive, because no published timetable exists.

Frequently asked questions

What percentage of people are financially literate? It depends entirely on which survey, which country and which year, and the honest answer is that no single global number is current. The TIAA Institute-GFLEC Personal Finance Index, published June 2026, found US adults answered 47% of its questions correctly and states the figure has never exceeded 52% in ten waves. FINRA's National Financial Capability Study, published July 2025 on 2024 fieldwork, found 27% of US adults answered at least five of seven questions correctly. India's most recent national figure is 27.18%, from fieldwork that ended in October 2019. The widely quoted global figure of about a third of adults comes from a one-off 2014 survey that has never been repeated.

What is India's financial literacy rate? 27.18%, and the important part is the date. The figure comes from the National Centre for Financial Education's Financial Literacy and Inclusion Survey, with fieldwork running June 2018 to October 2019 across 75,140 adults aged 18 to 80 in all 35 states and union territories. It uses OECD scoring: a person counts as financially literate with a combined score of at least 15 out of 22, including minimums of 3 in attitude, 6 in behaviour and 6 in knowledge. The component breakdown is revealing, with attitude at 89%, behaviour at 53% and knowledge at 49%. The previous wave measured 20% in 2013-14.

Why is India's financial literacy figure so old? Because the survey that produces it has not been repeated on schedule. NCFE's stated cadence is five-yearly, which would have placed a new wave around 2024, and none has been published. The National Strategy for Financial Education that covered 2020 to 2025 has since expired without a published successor and without the national survey it envisaged. A written reply in the Rajya Sabha on 11 March 2025 declined to state any percentage at all and referred to the survey as a 2017 exercise. So the seven-year-old number is not merely stale; there is currently no official replacement in progress that has been made public.

Which numbers get mistaken for India's financial literacy rate? Four, and each measures something different. The Financial Inclusion Index, which stood at 67.0 for March 2025, measures access to financial services, not understanding of them. NCFE's mid-term evaluation of the national strategy is not a national rate, because 6,000 of its 10,000 respondents were beneficiaries of NCFE's own programmes, which biases it upward. The SEBI Investor Survey covers people who already invest in securities, not the adult population. And any OECD score attributed to India is wrong, because the OECD's 2023 adult financial literacy survey does not include India.

Where should a complete beginner start? With the vocabulary, then the two forces that move money without anyone doing anything. Most people find the terminology is the actual barrier, more than the arithmetic, so a glossary is a more useful first stop than a budgeting method. After that, compound interest and inflation are the two mechanisms that change the value of money over time whether or not you act, which makes them the concepts that make every later decision legible. Documents come third: a pay stub, a credit report and a tax form are where the abstractions turn into your own numbers.

Sources

-

TIAA Institute and GFLEC, Personal Finance Index, published June 2026 (US adults answering 47% of questions correctly, and that the figure has never exceeded 52% across ten waves) gflec.org

-

National Centre for Financial Education, Financial Literacy and Inclusion Survey, executive summary (the 27.18% rate, fieldwork June 2018 to October 2019, n=75,140, the OECD scoring threshold, the attitude, behaviour and knowledge components, and the regional and state breakdowns) ncfe.org.in

-

Reserve Bank of India, National Strategy for Financial Education 2020-2025 (restating the 27.18% figure, and the strategy period that has now expired) rbi.org.in

-

Press Information Bureau, Rajya Sabha written reply on financial literacy, 11 March 2025 (which states no percentage and refers to the survey as a 2017 exercise) pib.gov.in

-

FINRA Investor Education Foundation, National Financial Capability Study, published 16 July 2025 on 2024 fieldwork (27% answering at least five of seven questions correctly) finrafoundation.org

-

OECD, OECD/INFE 2023 International Survey of Adult Financial Literacy (the 60 out of 100 average, and the participating economies, which do not include India) oecd.org

-

Standard & Poor's Ratings Services, Global Financial Literacy Survey, fieldwork 2014, published November 2015 (the 33% global, 57% US and 24% India figures, from a survey never repeated) gflec.org

You might also like

What is financial literacy? A plain-English explanation of the skill that helps people make informed money decisions. No jargon, no advice, just clear research.

8 min read

Personal finance basics explained in plain English: income, saving, debt, credit, and investing, the small set of concepts every adult tends to encounter.

8 min read

What CIBIL, UPI, EMI and TDS mean, and their US equivalents FICO, ACH and withholding. Plain definitions with real numbers, plus the pairs people mix up.

17 min read