What Is Buy Now, Pay Later (BNPL)? How It Works and What It Costs

By Tapabrata Biswas · Published June 15, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

That "pay in 4, interest-free" button at online checkout has quietly become one of the most common ways people borrow — often without thinking of it as borrowing at all. This explains what Buy Now, Pay Later actually is, how the model makes money, what it really costs when something goes wrong, and how it stacks up against a credit card. It's educational, not a recommendation to use or avoid BNPL — the providers named below appear only as examples of how the model works, never as endorsements.

BNPL is credit, even when it's free. Understanding the mechanics — especially what happens the moment a payment is late — is the difference between a convenient tool and an expensive habit.

What buy now, pay later actually is

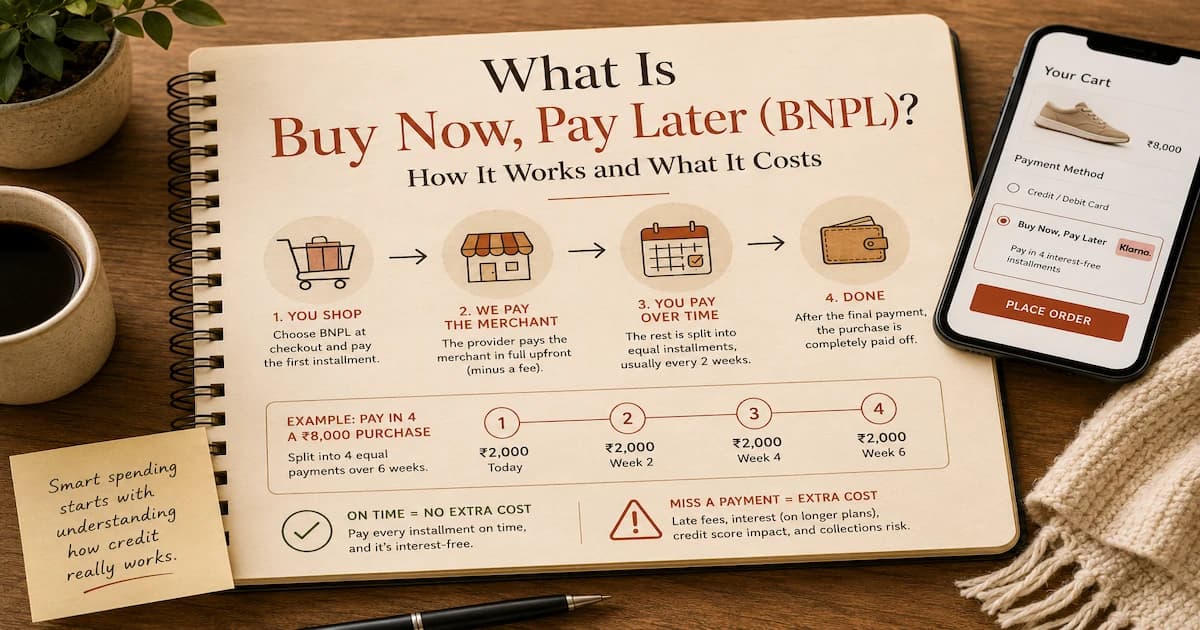

Buy Now, Pay Later (BNPL) is a short-term financing arrangement that splits a purchase into a few equal installments — most commonly four payments over six weeks — with the provider paying the merchant in full upfront and collecting from you over time. You take the item home (or it ships) immediately, having paid only the first installment, and the rest is auto-debited on a fixed schedule.

The best-known providers — Klarna, Affirm, and Afterpay in the US, and "pay later" options built into apps and checkouts in India — all run versions of this model. To the shopper it feels like a discount on timing; structurally, it's a loan with a fixed repayment plan. That distinction matters, because every protection and risk that comes with borrowing applies here too.

How the "pay in 4" model works

The mechanics are consistent across providers:

- At checkout, you choose BNPL instead of paying in full and split, say, a ₹8,000 or $200 purchase into four parts.

- You pay the first installment (a quarter of the total) immediately.

- The provider pays the merchant the full amount right away, minus a fee the merchant agreed to.

- The remaining installments auto-debit from your card or bank account every two weeks until the balance is clear.

The merchant accepts a smaller cut in exchange for higher conversion — shoppers spend more when payment is spread out. That merchant fee, not interest, is how the "interest-free" short plans make most of their money. It's the same reason a card network charges merchants: the cost is built into the price you pay, whether you use BNPL or not.

Approval is the other half of the appeal. Most short plans run only a soft credit check or none at all, and the decision is instant — no application, no waiting, often no visible interest rate. That frictionlessness is the product: the easier it is to split a payment, the more people spend. It's also why BNPL can slip past the mental brakes that a formal loan application would normally trigger, which is the single biggest behavioural risk it carries.

What it costs — fees, interest, and late charges

The annual percentage rate (APR) is the all-in yearly cost of borrowing, and for a "pay in 4" plan paid on time, it's effectively zero. The cost appears only when you fall behind, or when you choose a longer financed plan.

A worked example shows how a "free" plan stops being free:

A $200 jacket, split into four $50 payments over six weeks, costs exactly $200 if every payment lands on time. Miss the third $50 payment and a typical late fee of around $7 applies — and some providers add a second fee if it stays unpaid, or convert the balance to an interest-bearing loan. That turns a $50 installment into $57 or more: a ~14% surcharge on that single payment, plus a possible mark on your credit file.

Two cost structures sit under the same "BNPL" label:

- Short "pay in 4" plans — interest-free if paid on schedule; you only ever pay more through late fees.

- Longer installment plans (3, 6, or 12 months) — these usually do charge interest, sometimes at rates comparable to or above a credit card, the same compounding dynamic explained in how credit card interest works.

In India, the picture shifted after the Reserve Bank of India's 2022 digital-lending guidelines and its bar on loading credit lines onto prepaid wallets — changes that pushed BNPL providers to disclose terms more clearly and route credit through regulated lenders. The mechanics are the same; the disclosure rules are tighter.

BNPL vs credit cards

BNPL is often pitched as a friendlier alternative to credit cards, but they solve different problems and carry different risks:

| Feature | BNPL ("pay in 4") | Credit card |

|---|---|---|

| Structure | One purchase split into fixed installments | Revolving line, reusable up to a limit |

| Interest | Usually 0% if paid on schedule | Interest on any carried balance (often ~18–42%) |

| Credit check | Often a soft check or none | Hard check at application |

| Builds credit | Usually not | Yes — on-time payments are reported |

| Penalty for missing | Flat or capped late fee (sometimes interest) | Late fee + interest + score impact |

| Term | Fixed end date (e.g., six weeks) | Open-ended |

The trade-off is real. A credit card paid in full each month is interest-free and builds your credit history. BNPL is interest-free on the short plan but usually builds nothing — so the "smarter" choice depends entirely on whether you'd otherwise carry a card balance. Because BNPL sits outside your card's reported balance, it also doesn't show up in your credit utilization — which means it can hide how much you've actually committed to repay.

The mechanics point to where each fits. BNPL's interest-free short plan is cheapest for a one-off purchase you'll clear within weeks and would otherwise carry on a credit-card balance. A card paid in full each month wins where the rewards, fraud protection, and credit-building matter — none of which the short BNPL plan usually offers. Neither is free of risk: both are designed to make spending money you don't yet have feel effortless.

What happens if you miss a payment

This is where BNPL's gentle framing falls away. A missed installment typically triggers, in some combination: a late fee, a paused account (no new BNPL purchases until you catch up), a report to a credit bureau, and — for longer plans — the start of interest charges. Several providers now pass persistent misses to debt collectors, the same as any other unpaid loan.

The structural risk is quieter than a single late fee: because BNPL is so frictionless, it's easy to run several plans at once across different providers, each with its own auto-debit date. A shopper juggling four or five concurrent plans can lose track of the total committed — and a single short-paid bank account can trigger missed payments across all of them at once. BNPL doesn't fail loudly the way a maxed-out card does; it fails when the auto-debits quietly stack up. For larger one-time needs, a single personal loan with one fixed EMI is far easier to track than several overlapping BNPL plans.

Frequently asked questions

Does BNPL affect your credit score?

It depends on the provider and plan. Many short "pay in 4" plans don't report on-time payments, so they don't build credit — but missed payments increasingly get reported or sent to collections, which can hurt your score. Longer BNPL loans more often involve a hard check and bureau reporting. The catch is the asymmetry: paying on time often does nothing for your score, while a default can still damage it.

Is BNPL the same as a credit card?

No. A credit card is a reusable revolving line that charges interest on carried balances. BNPL splits one purchase into fixed installments, usually interest-free if paid on schedule, with the provider paying the merchant upfront. BNPL is tied to a single purchase with a fixed end; a card is open-ended.

What happens if you miss a BNPL payment?

Most providers charge a late fee, may pause your account, and increasingly report the miss to a bureau or pass it to a collector. Some longer plans start charging interest once you fall behind. The "interest-free" promise holds only while every payment is on time.

Do BNPL plans charge interest?

The common "pay in 4" plans are interest-free when paid on schedule — providers earn mainly from merchant fees. Longer plans (3, 6, or 12 months) often charge interest, sometimes above credit-card rates. Check which type an offer is before agreeing.

What this post does not cover

This is a definitional explainer of how BNPL works — not a recommendation to use or avoid it, and not a comparison of specific providers' current terms, which change often and vary by country and merchant. It doesn't advise on whether BNPL suits your situation or how much is safe to commit; those depend on your income, existing debt, and discipline with auto-debits. For a borrowing decision with real stakes, read the specific plan's terms in full and, where it matters, speak with a qualified financial professional.

Sources

- Consumer Financial Protection Bureau (CFPB), Buy Now, Pay Later: Market trends and consumer impacts — consumerfinance.gov

- Reserve Bank of India, Guidelines on Digital Lending (2022) — rbi.org.in

- Reserve Bank of India, Loading of credit lines on prepaid payment instruments (PPIs) — rbi.org.in

You might also like

Credit card interest is charged daily on your average daily balance once you carry a balance. The real math, grace periods, and the minimum trap, in ₹ and $.

13 min read

RBI barred pre-payment charges on loans sanctioned from 1 January 2026, but only on floating-rate loans. Most personal loans are fixed, so check which you hold.

14 min read

TransUnion CIBIL calls 30% a healthy ratio but sets no official cut-off, and FICO publishes none either. What the data shows, and why top scores sit under 10%.

13 min read