What Is a Personal Loan? Rates, EMIs and the Prepay Rule

By Tapabrata Biswas · Updated July 21, 2026 · 14 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

RBI barred pre-payment charges on loans sanctioned from 1 January 2026. That much got reported widely.

The sentence that decides whether it reaches you did not. The bar in paragraph 5(i) covers floating rate loans to individuals for purposes other than business, and personal loans in India are commonly written at fixed rates. A fixed-rate personal loan sits outside that paragraph.

The ranking pages that mention the Directions at all tend to report the headline and stop before the word "floating". That leaves a reader holding a fixed-rate loan believing a protection applies to them when it may not.

So this covers what a personal loan is, what it costs once the fees are counted, and the pre-payment rule with the qualifier attached.

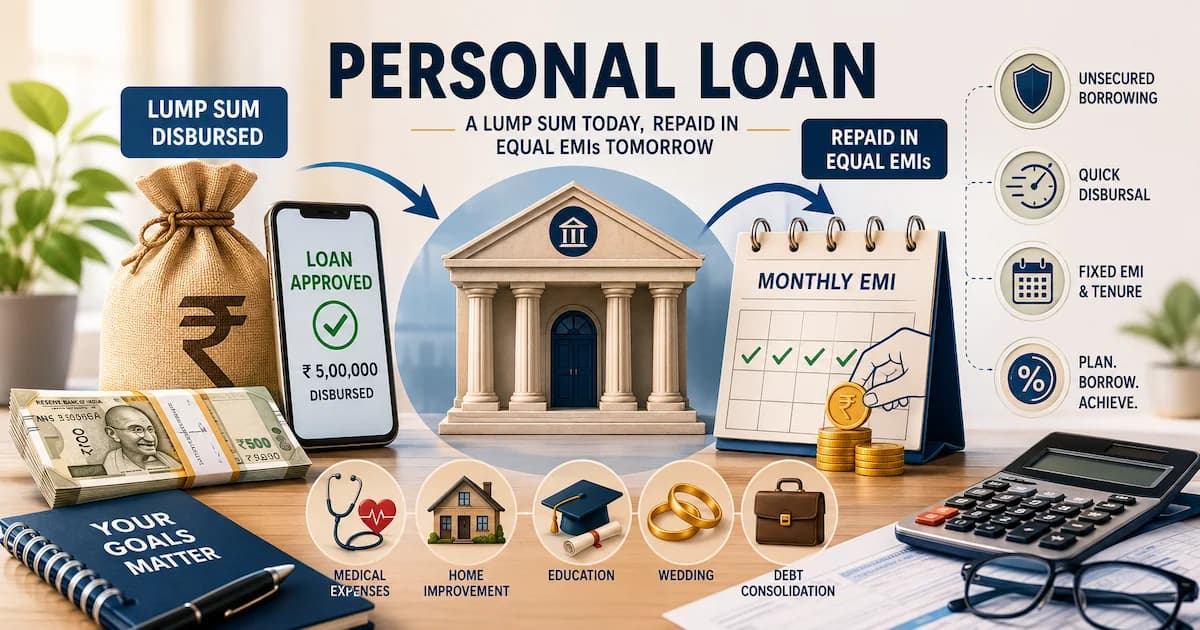

What is a personal loan?

A personal loan is an unsecured installment loan that a bank or NBFC pays out as a single lump sum, repaid in fixed monthly instalments over an agreed term. The term usually runs one to five years, and interest applies to the balance still outstanding.

Three features define it, and the third drives the other two.

| Feature | What it means |

|---|---|

| Lump sum | The full amount arrives once and cannot be drawn on again |

| Installment | The EMI and the closing date are fixed when you sign |

| Unsecured | No asset backs it, so the lender relies on income and credit record |

Being unsecured is why a personal loan costs more than a home loan or a gold loan, where the lender can fall back on the asset. It is also why eligibility rests on your income, your existing obligations and your credit record.

What does a personal loan cost?

The headline rate understates the cost, because compulsory fees sit outside it. The most common is a processing fee deducted from the disbursal, which means you repay interest on the full sanctioned amount while receiving less than it.

Take a loan of ₹5,00,000 at 12% over three years.

| Item | Amount |

|---|---|

| Sanctioned | ₹5,00,000 |

| Monthly EMI | ₹16,607 |

| Total repaid over 36 months | ₹5,97,858 |

| Interest paid | ₹97,858 |

| Processing fee at 2%, deducted upfront | ₹10,000 |

| Actually credited to your account | ₹4,90,000 |

The interest alone comes to close to a fifth of the principal. The fee then widens the gap between what you repay on and what you received, and a loan advertised at a lower rate with a larger fee can end up the costlier of two offers.

The number that folds both parts together is the APR. Indian lenders must disclose it on a Key Facts Statement for retail and MSME loans sanctioned from 1 October 2024, along with a computation sheet and an amortisation schedule, under an RBI circular of 15 April 2024. That document acts as a cap as well as a disclosure, since a fee it does not mention cannot be charged later without your explicit consent. What APR includes, and the specific fees regulation leaves out of it, is covered in our APR explainer.

On the US side, the Federal Reserve's G.19 release of 8 July 2026 puts the rate on 24-month personal loans at commercial banks at 11.86% for May 2026.

Can you pre-pay a personal loan without a charge?

Under the Reserve Bank of India (Pre-payment Charges on Loans) Directions, 2025, a regulated entity shall not levy pre-payment charges on floating rate loans to individuals for purposes other than business. The Directions carry reference RBI/2025-26/64, are dated 2 July 2025, and apply to all loans and advances sanctioned or renewed on or after 1 January 2026.

The qualifier does the work here, so the scope is worth reading closely.

| Loan | Covered by the bar? |

|---|---|

| Floating rate, individual, non-business purpose | Yes, paragraph 5(i) |

| Fixed rate, individual, non-business purpose | Not by paragraph 5(i) |

| Dual or special rate | Depends on whether it is floating when you pre-pay, paragraph 5(iv) |

| Individual for business purposes, or MSE, from a larger bank or upper-layer NBFC | Yes, paragraph 5(ii)(a) |

| Individual for business purposes, or MSE, from a smaller entity | Yes, up to a sanctioned limit of ₹50 lakh, paragraph 5(ii)(b) |

Personal loans are commonly written at fixed rates, which is why the sanction letter matters more here than the headline. Fixed or floating is the field to look for.

Where the bar does apply, it is unusually complete. Paragraph 5(iii) states that it holds irrespective of the source of the funds used for pre-payment, on part or full pre-payment, on loans with or without co-obligants, and without any minimum lock-in period. Each of those closes a specific workaround. A lender cannot demand that the money come from your own savings and no one else's, cannot restrict the relief to full closure, and cannot make you wait twelve EMIs first.

Two limits are worth holding alongside it. The Directions bite on loans sanctioned or renewed from 1 January 2026, so an older loan runs on its existing agreement. And they govern the pre-payment charge itself, not interest already accrued.

How does a personal loan compare with a credit card?

A personal loan amortises on a fixed schedule while a card balance revolves with no end date, and on published averages the card costs roughly nine percentage points more.

| 24-month personal loan | Credit card, all accounts | |

|---|---|---|

| Rate, May 2026 | 11.86% | 20.94% |

| Repayment | Fixed EMI, fixed closing date | Revolving, no end date |

| Amount | Fixed at sanction | Drawn repeatedly up to a limit |

| Source | Federal Reserve G.19, 8 July 2026 | Federal Reserve G.19, 8 July 2026 |

Both figures come from the same table in the same release for the same month, so the comparison is like for like. On accounts assessed interest, meaning cards actually carrying a balance, the same release records 22.15%.

The structural difference matters as much as the rate gap. A personal loan has a date on which it ends. A revolving balance does not, which is the mechanism explained in how credit card interest works, and the reason credit utilisation behaves differently on a card than on an installment loan.

What this post deliberately does not cover

This explains what a personal loan is, how its cost is assembled and what the pre-payment Directions say. It does not recommend taking or avoiding a loan, does not rank lenders, and does not assess whether borrowing suits your circumstances.

Several adjacent subjects sit elsewhere on purpose. How APR is defined and what regulation excludes from it is in the APR explainer. How a rate is set and when a floating rate resets is in what an interest rate is. Using a personal loan to replace other borrowing is debt consolidation, which has its own arithmetic.

Two limits on the figures. The G.19 numbers are for US commercial banks in May 2026 and get revised in later releases, so re-check them at the source. And the Directions are summarised here, not reproduced; the notification governs, and paragraph numbers are given so the wording can be read directly.

Whether a particular loan is affordable depends on income, existing obligations and circumstances no article can see. A qualified financial adviser is the right place for that question, and the loan agreement is the document that governs the terms.

Frequently asked questions

Can a lender still charge me a foreclosure fee on a personal loan? Possibly, and it turns on whether your loan is fixed or floating. RBI's Pre-payment Charges on Loans Directions, 2025 apply to loans sanctioned or renewed on or after 1 January 2026, and paragraph 5(i) says a regulated entity shall not levy pre-payment charges on floating rate loans to individuals for purposes other than business. Personal loans are commonly written at fixed rates, and a fixed-rate personal loan is not covered by that paragraph. For a dual or special rate loan, paragraph 5(iv) says the answer depends on whether the loan is on a floating rate at the moment you pre-pay. The sanction letter is where you check which one you hold.

What is a personal loan in simple terms? A personal loan is an unsecured installment loan that a bank or NBFC pays out as one lump sum, which you repay in fixed monthly instalments over an agreed term, usually one to five years. Three things define it. The money arrives all at once, in a single payout you cannot draw on again. The instalment and the end date are fixed when you sign. And it is unsecured, so no asset backs it, which is the reason it costs more than a home loan or a gold loan and the reason your income and credit record carry the decision.

How much does a personal loan actually cost? More than the headline rate, because compulsory fees sit outside it. A processing fee deducted from the disbursal means you receive less than the sanctioned amount while paying interest on the full sum. On a five lakh rupee loan at 12% over three years, the EMI works out to about 16,607 rupees and the total interest to about 97,858 rupees, and a 2% processing fee deducted upfront means only 4,90,000 rupees reaches your account. The single number that captures both parts is the APR, which Indian lenders must disclose on the Key Facts Statement for retail loans.

Is a personal loan cheaper than a credit card? On the published averages, substantially. The Federal Reserve's G.19 release of 8 July 2026 puts the rate on 24-month personal loans at US commercial banks at 11.86% for May 2026, against 20.94% across all credit card accounts and 22.15% on accounts assessed interest, all from the same table and the same month. The structures differ as much as the rates. A personal loan has a fixed instalment and a fixed end date, while a card balance revolves with no end date, so the comparison is between a debt that amortises on a schedule and one that need not.

What credit score do lenders look for? Lenders reserve their finest rates for stronger scores, and the working thresholds differ by country because the scoring systems do. In India, CIBIL scores run from 300 to 900 and lenders commonly treat the upper 700s as strong. In the US, FICO scores run from 300 to 850. In both markets the score is one input among several, since lenders also weigh income, existing obligations and employment, and each sets its own criteria. A score below a lender's preferred band often means a higher rate or a smaller sanction, with outright refusal the less common outcome.

What is the Key Facts Statement and why does it matter here? It is a standardised summary Indian lenders must give retail and MSME borrowers, carrying an all-in APR plus a computation sheet and an amortisation schedule, under an RBI circular of 15 April 2024 that took effect for loans sanctioned from 1 October 2024. It matters for a personal loan because it puts the interest rate and the compulsory fees into one comparable figure. It also caps what can be charged, since a fee not mentioned in the statement cannot be billed later without the borrower's explicit consent.

Sources

-

Reserve Bank of India, Reserve Bank of India (Pre-payment Charges on Loans) Directions, 2025, RBI/2025-26/64, 2 July 2025 (applicability to loans sanctioned or renewed on or after 1 January 2026; paragraph 5(i) on floating rate loans to individuals for non-business purposes; 5(ii)(a) and 5(ii)(b) including the ₹50 lakh limit; 5(iii) on source of funds, co-obligants and lock-in; 5(iv) on dual and special rate loans) rbi.org.in

-

Reserve Bank of India, Key Facts Statement for Loans and Advances, 15 April 2024 (the all-in APR, the computation sheet and amortisation schedule, applicability to retail and MSME loans sanctioned from 1 October 2024, and the rule that a fee absent from the KFS cannot be charged without explicit consent) rbi.org.in

-

Board of Governors of the Federal Reserve System, G.19 Consumer Credit, release of 8 July 2026, Terms of Credit at Commercial Banks (24-month personal loan rate 11.86%, credit card plans all accounts 20.94%, accounts assessed interest 22.15%, all for May 2026) federalreserve.gov

You might also like

Credit card interest is charged daily on your average daily balance once you carry a balance. The real math, grace periods, and the minimum trap, in ₹ and $.

13 min read

What is a debt consolidation loan, the three main forms it takes in India and the US, and the conditions under which it actually saves money instead of just rearranging it.

9 min read

TransUnion CIBIL calls 30% a healthy ratio but sets no official cut-off, and FICO publishes none either. What the data shows, and why top scores sit under 10%.

13 min read