8 Best Apps to Track Net Worth (2026): Free & Paid

By Tapabrata Biswas · Updated July 5, 2026 · 14 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

When Intuit shut Mint down in March 2024, it moved millions of users to Credit Karma, which shows your accounts but never rebuilt Mint's clean net-worth-over-time view. That is why so many people are now searching for a net worth tracker: they want the one number Mint used to give them, total assets minus total liabilities, tracked month over month. This guide covers the eight apps actually worth using for that in 2026, free and paid, plus how bank-linking safety works and a no-app spreadsheet option.

One thing to know before you pick: the largest single asset for most households, the home, is the one thing these apps see worst. The Federal Reserve's 2022 survey put the primary residence at about 27% of average US household assets, and almost every consumer app either misses it or estimates it. Where that matters, and how to handle it, is covered below.

What a net worth tracker app does

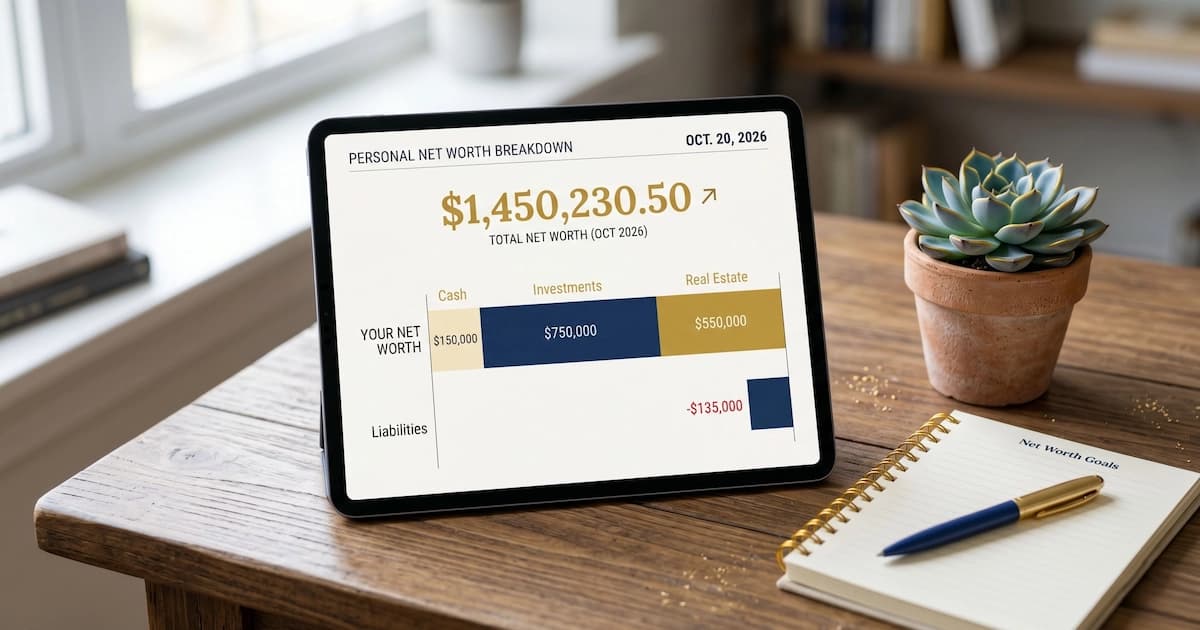

A net worth tracker app computes one number, total assets minus total liabilities, by linking your financial accounts and refreshing the total as balances change. Assets are cash, savings, investments, retirement accounts, real estate, and vehicles; liabilities are credit-card balances, student loans, mortgages, and other debt. The app sums the first group, subtracts the second, and plots the result over time.

That last part is the point. Net worth is a balance sheet, so what matters is the trend across months and years; the daily wiggle is just noise. A student often has a slightly negative net worth and does not need to track it closely; someone in their thirties with a mortgage, a 401(k), and a brokerage benefits from seeing the pieces move in different directions; someone near retirement needs the full picture across every account. For the underlying idea, see our what is net worth explainer.

The 8 best net worth tracker apps for 2026

The shortlist at a glance, with the free-versus-paid split and how each handles homes and crypto (the assets that separate the good apps from the rest):

| App | Best for | Price | Free plan | Homes & crypto |

|---|---|---|---|---|

| Empower (formerly Personal Capital) | Best free, US | Free | Yes | Home manual, crypto manual or linked |

| Monarch Money | Best Mint replacement | ~$100/yr | Trial only | Home via Zillow, crypto linked |

| Kubera | Best for real estate + crypto + alt-assets | ~$249/yr | Trial | Home auto (Zillow), crypto linked, alt-assets |

| Copilot Money | Best design, iOS only | ~$95/yr | Trial | Home manual, crypto linked |

| Quicken Simplifi | Best low-cost all-in-one | ~$48/yr | No | Home manual, crypto manual |

| PocketSmith | Best for forecasting | Free / paid tiers | Yes | Home manual, projections |

| Tiller | Best spreadsheet | ~$79/yr | Trial | Fully manual, customisable |

| INDmoney | Best for India | Free | Yes | Home manual, aggregates MF, stocks, EPF, US stocks |

Prices are annual and current as of mid-2026; app pricing drifts, so confirm on the app's site.

Best free net worth trackers

Empower has the deepest free net-worth tier in the US, which is why it is the most common Mint replacement. It links bank accounts, credit cards, brokerage, 401(k), IRA, mortgage, and student-loan accounts through Plaid, produces a unified net-worth view that updates daily, and throws in a genuinely useful investment-fee analyzer that flags expensive funds in your retirement accounts. It stays free because Empower's real business is wealth-management advisory; cross a rough $100,000 in linked assets and you may get advisor calls, which you can decline while keeping the free tools.

Empower's blind spot is illiquid assets. Real estate goes in as a manual line that does not auto-update, vehicles need manual entry, and private business equity is invisible. For someone with mostly liquid wealth (bank, brokerage, retirement), Empower covers the whole picture; for someone with a lot of home equity, it undercounts by exactly that amount until you enter it.

Two more free routes are worth knowing. PocketSmith has a free tier and stands out for cash-flow forecasting, projecting your balances and net worth forward, which none of the others do as well. And if you already bank with Fidelity, its Full View aggregates outside accounts into a net-worth view at no cost.

Best paid net worth trackers

Monarch Money is the paid app most people move to after Mint, because former Mint team members built it as a direct replacement. At about $100 a year it bundles net-worth tracking with budgeting and bill tracking, pulls US home values from Zillow, links crypto, and, uniquely at this price, lets both partners share one household account. If you want net worth alongside an actual budget, Monarch is the pick.

Kubera is the choice when your wealth is complex or illiquid. At about $249 a year it is the most expensive here, but it auto-updates US real estate via Zillow, links crypto through exchanges, and handles alternative assets (art, collectibles, private equity, domains, a car by VIN) that the others ignore, across banks in many countries. It is the only major app built around net worth first, and it covers markets, including India, where Empower and Monarch do not sync banks.

Copilot Money is iOS-only with the best-looking interface in the category. Its net-worth tracking is solid without being class-leading, but for someone already inside the Apple ecosystem paying about $95 a year, the included view is more than enough. Quicken Simplifi, at roughly $48 a year, is the low-cost all-rounder, a light net-worth view sitting on top of strong budgeting.

Is it safe to link your bank accounts?

Linking a bank account to a reputable net worth app is generally safe because the connection is read-only and runs through a regulated aggregator with read-only access, so the app never stores your bank password. This is the question that stops most people, so it is worth spelling out.

These apps connect through account aggregators, mainly Plaid, MX, or Yodlee. In a typical flow you enter your bank login on the aggregator's own screen, the aggregator returns a read-only token, and the app can then see balances and transactions but cannot move money. The data is encrypted in transit and at rest. The real risks are the ordinary ones: a breach at the app or the aggregator, and phishing that tricks you into entering credentials somewhere fake.

The sensible precautions are the usual ones. Use a strong, unique password and turn on two-factor authentication for the app and the linked bank. Stick to established apps with a track record. And if you are genuinely not comfortable linking accounts at all, the spreadsheet route below sidesteps the whole question.

The DIY option: a net worth tracker in Google Sheets

You do not need an app at all; a free Google Sheet tracks net worth manually with three simple parts. For people who would rather not link accounts, or who want full control, a spreadsheet is the oldest and most private method.

The layout that works:

- An Assets tab. Rows for cash and savings, investments and brokerage, retirement accounts, your home, vehicles, and anything else of value. One column per account, one total at the bottom.

- A Liabilities tab. Rows for the mortgage, loans, and credit-card balances, with a total.

- A monthly snapshot row. Once a month, record total assets, total liabilities, and the difference (net worth). Over a year those rows become a trend line, which is the whole point.

Tools like Tiller can auto-sync bank data into a Google Sheet for about $79 a year, and free templates are widely available. If you want a ready formula-driven sheet to start from, the same build approach we use for a budget in Google Sheets works for a net-worth sheet: swap the income and expense sections for Assets and Liabilities tabs and keep the monthly snapshot row.

How these apps handle real estate and crypto

The home is where consumer apps diverge most, and it matters because it is the biggest asset most households own. The four approaches:

| Approach | Apps | Accuracy |

|---|---|---|

| Zillow auto-estimate | Kubera, Monarch (US only) | Approximate, refreshed automatically |

| Manual entry with reminder | Empower, Copilot | Accurate when entered, stale after |

| Manual entry, no reminder | INDmoney, Kuvera | Only as current as you keep it |

| Not supported | Investment-only trackers | Home is invisible |

Even Zillow estimates drift 10% to 20% from what a home would actually sell for, so a household with meaningful home equity should treat the app's number as directional and refresh the home value manually every quarter. In India there is no automated home valuation at all (no local Zillow), so Indian users set property values by hand using circle rates or comparable listings on MagicBricks or 99acres.

Crypto is handled better across the board. Empower, Monarch, Copilot, Kubera, and INDmoney all support either exchange linking (Coinbase, Binance) or manual entry, and exchange-linked holdings update in real time, which can make daily net-worth swings dramatic if crypto is a big share of the total.

How to actually track your net worth

Tracking net worth is a five-step routine, not a daily habit. Pick one tool (a free app like Empower, or a spreadsheet). Link your accounts, or enter their balances. Add the manual assets the app cannot see, chiefly your home and vehicles. Set an update cadence; monthly is plenty, because the number moves slowly and only the long trend carries meaning. Then look at the direction of travel: the useful question is whether the line is rising year over year, and which pieces are driving it. An app that produces a clean year-over-year line graph is doing the most valuable thing in this category.

In India: INDmoney and Kuvera

In India, INDmoney is the closest thing to Empower, aggregating stocks, US stocks, mutual funds, EPF, NPS, fixed deposits, and bank balances into one free net-worth number. Kuvera adds a free family view across a household but is more mutual-fund and goal focused than a full asset aggregator. Real estate is manual, as noted, because India has no automated home valuation.

One scoping note: most Indians who want app-based tracking are really after a portfolio tracker (per-holding stock and mutual-fund performance) more than a single net-worth figure. If that is you, our best investment tracking apps guide covers the India options (INDmoney, Kuvera, and the portfolio-focused tools) in depth, framed around holdings and returns, not one aggregate number.

Frequently asked questions

What is the best free net worth tracker app? For US users, Empower (formerly Personal Capital) is the strongest free option. It links bank, credit, brokerage, 401(k), and IRA accounts through Plaid and produces a complete net-worth view that updates daily, plus a free investment-fee analyzer. It stays free because Empower's business is wealth-management advisory; if your linked assets pass roughly $100,000 you may get a sales call, which is easy to decline. For Indian users, INDmoney is the most comprehensive free option. The trade-off with any free app is that illiquid assets like real estate and vehicles need manual entry.

What replaced Mint for tracking net worth? Intuit shut Mint down in March 2024 and pushed users to Credit Karma, which tracks accounts but does not give a proper net-worth view over time. For free net-worth tracking the common replacement is Empower. For a paid all-in-one that also budgets, the common pick is Monarch Money, which was built partly by former Mint team members and is designed as a direct Mint replacement. Rocket Money and Quicken Simplifi are also frequently recommended for displaced Mint users.

Is it safe to link your bank account to a net worth app? For reputable apps, yes, within the usual limits. They connect through aggregators like Plaid, MX, or Yodlee using read-only access, so the app can see balances and transactions but cannot move money, and in most flows your bank login is entered on the aggregator's own screen, so the app never stores it. The data is encrypted. The residual risks are the same as any account: a data breach at the app or aggregator, and phishing. Using a strong unique password and two-factor authentication, and choosing established apps, keeps the risk low. If you are not comfortable linking, a manual Google Sheet avoids it entirely.

What is the best app for tracking net worth with real estate and crypto? Kubera is the app most built for this. It auto-updates US home values via Zillow, links crypto through exchanges like Coinbase and Binance, and lets you add alternative assets (art, collectibles, private equity, domains, even a car by VIN) manually, across banks in many countries. It costs about $249 a year, the priciest on this list, but it is the only major app built specifically for net worth, where the others treat it as a budgeting add-on. Monarch also does US real estate via Zillow and linked crypto at a lower price.

Is Empower (Personal Capital) really free? Yes, the tracking tools are genuinely free: the net-worth dashboard, account aggregation, retirement planner, and fee analyzer cost nothing. Empower makes money from its paid wealth-management advisory service, which is optional. The main friction is that larger linked balances trigger occasional calls from Empower advisors offering that paid service. You can decline and keep using the free tools indefinitely. Personal Capital was renamed Empower after Empower Retirement acquired it, so the older name still turns up in searches.

Can I track net worth without linking bank accounts? Yes. A free spreadsheet does the whole job manually. Make an Assets tab (cash, investments, retirement, home, vehicles, other), a Liabilities tab (mortgage, loans, credit cards), and a row you fill in once a month so you can see the trend over time; net worth is simply total assets minus total liabilities. Tiller offers auto-syncing spreadsheets, and there are many free templates. Manual entry is more work than a linked app but keeps every credential in your own hands.

Which net worth tracking apps work in India? INDmoney is the closest Indian equivalent to Empower: it aggregates Indian stocks, US stocks, mutual funds, ETFs, EPF, NPS, fixed deposits, and bank balances into one net-worth figure, and it is free. Kuvera has a free family view but is more mutual-fund and goal focused. Indian real estate has no auto-valuation (there is no local Zillow), so home values are entered manually. For deeper per-holding portfolio tracking, beyond a single net-worth number, see our best investment tracking apps guide, which covers the India options in depth.

In summary

The best net worth tracker app for 2026 comes down to country, asset mix, and budget. US users with mostly liquid wealth get the most from free Empower, the standard Mint replacement. If you want net worth alongside a real budget, Monarch (about $100 a year) is the paid all-rounder; if your wealth includes real estate, crypto, or alternative assets, Kubera (about $249 a year) is the most complete; if you live in the Apple world, Copilot. If you would rather not link accounts, a Google Sheet with Assets, Liabilities, and a monthly snapshot does the job by hand. In India, INDmoney is the free go-to. Whatever you choose, the value is in the trend: track the number monthly, watch it year over year, and treat the home-value figure as an estimate to refresh each quarter. For per-holding investment performance beyond the single net-worth number, see best investment tracking apps.

Sources

- Federal Reserve, Survey of Consumer Finances 2022, federalreserve.gov

- Reserve Bank of India, Report of the Household Finance Committee (2017), rbi.org.in

- Empower, Personal Dashboard and Wealth platform overview, empower.com

- Kubera, About Kubera, kubera.com

- INDmoney, Net Worth Tracker, indmoney.com

You might also like

What is net worth? A plain-English explanation of the most foundational personal finance number, plus how to calculate yours in five minutes.

8 min read

Researched comparison of the best investment tracking apps for 2026, Sharesight, Empower, Morningstar, Kuvera, Groww, INDmoney plus CoinTracker and Koinly for crypto. India and US markets.

9 min read

Best expense tracker apps for 2026: US (Rocket Money, Monarch, Empower) and India (Moneyview, axio, ET Money), free and paid, plus the SMS-tracking reality.

14 min read