How Does Debt Consolidation Work — The Step-by-Step Process and the Numbers Behind It

By Tapabrata Biswas · Last updated May 11, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

A borrower with four credit cards totalling ₹3,20,000 at a weighted-average APR of 39% pays roughly ₹10,400 per month in interest alone if balances stay flat. Replace those four cards with one personal loan at 13% APR over four years, and the EMI is around ₹8,580 — less than the prior monthly interest, while the principal also retires. That is the mechanical reason debt consolidation works when it works. The process behind it has six concrete steps, and missing any of them is what causes consolidations to fail.

This piece walks through the actual procedural mechanics of debt consolidation: applying, qualifying, funding, paying off the old debts, settling into the single monthly payment, and tracking the credit-score impact through the months that follow. For the conceptual question of whether to consolidate, see our companion piece on what is a debt consolidation loan.

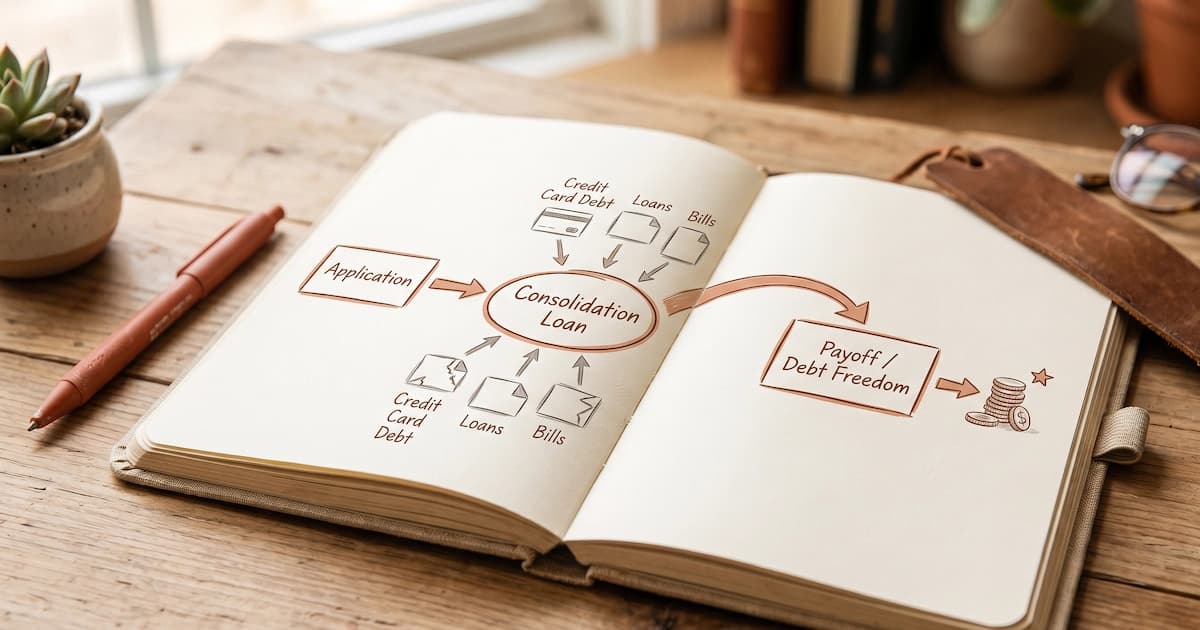

How debt consolidation works — the six-step process

Every debt consolidation, regardless of loan type or country, follows essentially the same six steps. The lender, the rate, and the paperwork differ. The sequence does not.

Step 1: Total existing debts and weighted-average APR

Before applying for a consolidation loan, the borrower lists every debt to be consolidated, the current balance, the APR, and the monthly minimum. The weighted-average APR — calculated as the sum of (each balance × its APR) divided by total balance — sets the threshold the new loan rate must beat.

Example: three cards at ₹80,000 (38%), ₹70,000 (36%), ₹90,000 (42%) total ₹2,40,000. Weighted average is roughly 38.7%. Any consolidation loan above that rate makes things worse, not better.

Step 2: Choose loan type and shop quotes from 3+ lenders

The three main forms — personal loan, balance transfer card, secured loan against an asset — each have different rate ranges, as covered in the companion post. Most borrowers will land on a personal loan in India or a personal loan / balance transfer card in the US.

Pre-qualification is a critical step. Most US lenders (LendingClub, SoFi, Discover, Marcus) and many Indian lenders (HDFC, ICICI, Bajaj Finserv) offer a soft-pull pre-qualification that returns an estimated rate without affecting the credit score. Three or more pre-qualifications give a real spread of offers to compare. Settling on the first quote almost always costs money.

Step 3: Submit the formal application — the hard inquiry

Once the best pre-qualified offer is selected, the formal application is submitted with full documentation: PAN, salary slips, bank statements (India) or pay stubs, W-2s, tax returns (US). This step triggers a hard inquiry on the credit report, which drops the credit score by roughly 5 to 10 points and remains visible to other lenders for 12 to 24 months per FICO and CIBIL scoring documentation, 2024.

Multiple hard inquiries from the same loan type within a 14 to 45 day window are scored as a single inquiry by both FICO and CIBIL — but only when they're for the same product type. Mixing personal loan and credit card applications does not get the rate-shopping discount.

Step 4: Underwriting and approval — the credit thresholds

Underwriting takes 1 to 5 business days at most lenders. The lender verifies income, debt-to-income ratio, and credit history. Approval thresholds in 2024:

| Market | Minimum credit score for approval | Score for best rates | Typical DTI cap |

|---|---|---|---|

| India (personal loan) | CIBIL 700+ | CIBIL 750+ | 50% of monthly income |

| India (gold loan) | No score requirement | N/A — based on gold value | N/A |

| US (personal loan) | FICO 660+ | FICO 720+ | 40–45% of monthly income |

| US (balance transfer card) | FICO 670+ | FICO 720+ | Issuer-dependent |

| US (home equity loan) | FICO 660+ | FICO 740+ | 43% (CFPB QM rule) |

Sources: CFPB consumer credit reports, 2024 and TransUnion CIBIL scoring guide, 2024.

Borrowers below these score thresholds can still consolidate through secured loans (gold in India, home equity in the US) or through US credit unions, where membership underwriting is slightly more flexible than commercial bank standards. For the full breakdown of what each FICO and CIBIL band actually unlocks in loan pricing, see what is a good credit score.

Step 5: Loan funds and old debts are paid off

Once approved, the loan funds in 1 to 5 business days. Two disbursement models exist:

- Direct-to-creditor. The consolidation lender pays old creditors directly. The borrower never sees the money. Offered by US lenders like Discover and Payoff and increasingly common in India. Removes the temptation to spend the funds elsewhere.

- Borrower-disbursed. Funds arrive in the borrower's bank account, and the borrower pays off the old debts manually. A 2023 LendingTree study found that 12% of borrowers who received funds directly used some portion for non-debt expenses.

Within 5 business days of funding, the old credit card balances should read zero. Screenshot the zero balances for records.

Step 6: Single monthly payment begins

The consolidation loan's first EMI is due 30 to 45 days after funding. From this point forward, the borrower has one monthly payment to track instead of several. Setting up auto-debit from the primary bank account eliminates the missed-payment risk that would re-damage the credit report.

A worked example — four credit cards into one personal loan

Consider a US borrower in late 2024 with four credit cards:

| Card | Balance | APR | Min. payment | Monthly interest only |

|---|---|---|---|---|

| Visa | $5,200 | 24% | $130 | $104 |

| Mastercard | $3,800 | 22% | $95 | $70 |

| Store card | $2,100 | 28% | $63 | $49 |

| Amex | $4,500 | 21% | $112 | $79 |

| Total | $15,600 | 23.4% weighted | $400 | $302 |

Paying only minimums with flat balances, $302 of every $400 monthly payment is interest. Only $98 reduces principal. At that rate, the debt takes more than 30 years to clear and accrues more than $25,000 in additional interest, per CFPB minimum-payment disclosure rules under the CARD Act.

Consolidation option: 5-year personal loan at 13% APR with 4% origination fee

The borrower needs $15,600 net. With a 4% origination fee, the loan amount is $16,250 ($15,600 / 0.96).

EMI on $16,250 at 13% APR over 60 months: $370/month. Total payments: $22,200. Total interest: $5,950 over 5 years.

Comparison

| Path | Monthly payment | Time to payoff | Total interest |

|---|---|---|---|

| Continue minimums on cards | $400 | 30+ years | $25,000+ |

| Consolidation loan | $370 | 5 years | $5,950 |

| Difference | −$30/mo | −25 years | −$19,000+ |

The consolidation reduces monthly payment by $30, saves close to $19,000 in interest, and clears the debt 25+ years faster. The net benefit is large — but only because the new rate (13% effective, including origination) is well below the 23.4% weighted average being replaced. For the credit-score side, see our explainer on what is credit utilisation.

How the credit score moves over 12 months

The credit-score effect of consolidation has a predictable shape across both FICO and CIBIL models:

| Month after consolidation | Effect | Typical score change |

|---|---|---|

| 0 (application) | Hard inquiry recorded | −5 to −10 points |

| 1 | Old card balances drop to zero, utilisation crashes | +20 to +40 points |

| 2–3 | New loan reports as account, average account age dips slightly | −2 to −5 points |

| 4–6 | On-time payment history on new loan begins building | +5 to +10 points |

| 7–12 | Steady improvement if cards stay at zero balance | +10 to +20 points |

Net effect at 12 months for a borrower who keeps the old cards at zero: +30 to +60 points. Net effect for a borrower who runs the old cards back up: −20 to −50 points below starting position, because total debt has now grown.

Fees and pitfalls to watch for

Three fee categories meaningfully affect whether the consolidation pencils out.

Origination fees. US personal loans charge 1–8% upfront, deducted from disbursed proceeds. On a $20,000 loan with a 6% origination fee, the borrower receives $18,800 but repays $20,000. Indian personal loans charge 0–3% as a "processing fee," lower than the US norm.

Prepayment penalties. Some lenders charge 1–4% of the outstanding balance if the loan is paid off early. RBI banned prepayment penalties on floating-rate personal loans for individual borrowers as of 2014, but fixed-rate loans can still carry them.

Balance transfer fees. US balance transfer cards charge 3–5% upfront. On a $10,000 transfer at 4%, that is $400 added to the balance. Math still favours transfer when intro APR is 0% for 18 months versus 22% on the source card, but the fee belongs in the comparison.

A prepayment penalty plus origination fee combination can erase a consolidation's rate-savings entirely. Both should be disclosed in the loan agreement before signing.

What experts say

The CFPB's debt consolidation FAQ, 2024 recommends comparing the total cost of credit — principal plus all interest plus all fees — across at least three offers before accepting any consolidation loan. Headline-APR comparison alone misses origination and balance-transfer fees that materially affect true cost.

The RBI Master Direction on Interest Rate on Advances, 2016 requires Indian banks to disclose the all-inclusive APR (including processing fees) at loan application. Borrowers should request this in writing rather than relying on the marketing-quoted headline rate.

The Federal Reserve's Report on the Economic Well-Being of US Households, May 2024 found 17% of US adults carrying card balances they pay off at less than the full amount each month — roughly 45 million households for whom even modest rate reductions through consolidation produce meaningful annual savings.

To compare the EMI and total interest a candidate consolidation loan would produce at three different tenures, our loan calculator handles the side-by-side math directly — useful before signing on a specific tenure.

Frequently asked questions

How long does the debt consolidation process take from start to finish?

The application-to-funding cycle for a personal loan takes 1 to 7 days at most Indian and US banks, with online lenders often funding in 24 to 48 hours. Once funds arrive, paying off the old debts takes another 1 to 5 business days depending on whether the lender disburses directly to creditors or to the borrower's account. Total elapsed time from application to all old debts paid off is normally 5 to 14 days.

What credit score do I need to qualify for a debt consolidation loan?

Most Indian banks require a CIBIL score of 700+ for unsecured personal loan approval, with the best rates reserved for 750+. US lenders generally require a FICO score of 660+ for personal loan approval, with the lowest APRs offered to borrowers above 720. Borrowers below these thresholds can still qualify through credit unions, NBFCs, or secured loan products like gold loans (India) or home equity loans (US), where the asset reduces the lender's risk.

Will my credit score drop after debt consolidation?

The hard inquiry from the loan application drops the score by roughly 5 to 10 points and stays on the report for 12 to 24 months. Once the old credit cards are paid off, utilisation drops sharply, which lifts the score within one to two billing cycles. The net effect after 90 days is generally neutral to positive — a 20 to 40 point gain is common when consolidation moves utilisation from above 60% to below 30%.

What fees should I watch for in a debt consolidation loan?

Three fee categories matter: origination fees (1 to 8 percent of loan amount in the US, 0 to 3 percent in India), prepayment penalties on the new loan if you plan to repay early, and balance transfer fees (3 to 5 percent of transferred amount on US balance transfer cards). A 5 percent origination fee on a $13,000 loan is $650 added to the principal — meaningful enough to affect whether the consolidation pencils out.

In summary

Debt consolidation is a six-step process: total the debts, shop multiple lenders, submit one formal application, qualify based on score and DTI, fund and pay off the old debts within two weeks, and start a single monthly payment. The credit-score impact is a brief hard-inquiry dip followed by a larger gain from utilisation collapsing once old cards hit zero. The arithmetic works when the new rate beats the weighted-average old rate by enough to absorb origination and balance-transfer fees. The $19,000 interest savings on a $15,600 starting balance shown above is typical for a high-APR-card borrower who qualifies for a mid-tier personal loan rate. The strategic question of whether to consolidate at all is covered in the companion piece on what is a debt consolidation loan.

Sources

- Consumer Financial Protection Bureau — Debt consolidation FAQ, 2024

- Reserve Bank of India — Master Direction on Interest Rate on Advances, 2016 (updated 2024)

- Federal Reserve — Report on the Economic Well-Being of US Households, May 2024

- TransUnion CIBIL — Credit score guide, 2024

- FICO — What's in your credit score, 2024

You might also like

What is a debt consolidation loan, the three main forms it takes in India and the US, and the conditions under which it actually saves money instead of just rearranging it.

9 min read

Yes, TransUnion CIBIL's guidance recommends keeping credit utilization under 30%. What 'official' really means, the ideal ratio, and how to lower it fast.

8 min read

How does credit card interest work? A plain-English breakdown of daily compounding, the average daily balance method, grace periods, and the minimum payment trap, with India and US numbers.

9 min read