How Credit Scores Are Calculated — FICO, CIBIL, and What Actually Affects Your Score

By Tapabrata Biswas · Last updated May 11, 2026 · 9 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

A FICO score of 720 versus 680 can change a 30-year US mortgage rate by roughly 0.4 percentage points, which on a $300,000 loan works out to about $25,000 in extra interest paid over the life of the loan (Consumer Financial Protection Bureau and Freddie Mac PMMS data, 2024). A CIBIL score of 760 versus 690 in India can change a home loan rate by 0.5–1.0 percentage points, which on a ₹50 lakh 20-year loan adds ₹4–8 lakh to the total interest. The score is not abstract. It is a price tag that every credit decision attaches to your future cash flow.

Both scores are calculated by formulas that have been publicly described in broad terms but never released as exact source code. FICO publishes the five factor categories and their weights; TransUnion CIBIL describes its four factors and gives approximate ranges. What follows is the documented breakdown for both, what each factor actually measures, and what the practical levers are for moving your score up.

How a credit score is built

A credit score is a three-digit number that summarises the information on your credit report. The score is a statistical estimate of the probability that you will pay back a new loan or credit line on time.

In the US, the dominant model is FICO 8, produced by the Fair Isaac Corporation. The score range is 300–850. The competing VantageScore model is also used by some lenders and by free-score services like Credit Karma. Both pull data from the three US credit bureaus: Experian, Equifax, and TransUnion.

In India, the dominant model is the TransUnion CIBIL score, with a range of 300–900. Three other bureaus operate in India under RBI regulation: Experian, Equifax, and CRIF High Mark. Most lenders pull from CIBIL but check at least one other bureau before approving large loans.

The factor categories are similar across bureaus and across countries, though the weights and the exact ranges differ.

The five FICO factors and their weights

FICO publishes the following weights for its FICO 8 model (the version used in roughly 90% of US lending decisions):

| Factor | Weight | What it measures |

|---|---|---|

| Payment history | 35% | Whether you pay on time; counts late payments, defaults, collections, bankruptcies |

| Amounts owed | 30% | Credit utilization ratio — total balance divided by total available credit |

| Length of credit history | 15% | Age of oldest account, age of newest account, average age of all accounts |

| Credit mix | 10% | Variety of credit types (revolving credit cards, installment loans, mortgage) |

| New credit | 10% | Recent hard inquiries and recently-opened accounts |

The 65% combined weight of payment history and amounts owed is the single most important fact about credit scores. Everything else — credit mix, length of history, new inquiries — moves the needle by single-digit percentage shares of the score. Pay on time and keep utilization low; the other factors take care of themselves over time.

The four CIBIL factors

TransUnion CIBIL publishes four factor categories with approximate weights, drawn from their own consumer education materials and RBI-mandated disclosures:

| Factor | Approximate weight | What it measures |

|---|---|---|

| Payment history | ~30% | On-time payment record across all loans and credit cards |

| Credit exposure (utilization) | ~25% | Outstanding balances relative to total credit limits |

| Credit type and tenure | ~25% | Mix of secured and unsecured credit; length of credit history |

| New credit and inquiries | ~20% | Recent loan applications and newly-opened accounts |

CIBIL's factor list collapses what FICO calls "credit mix" and "length of credit history" into a single category. The factor names and weights are similar enough that the practical advice for raising a score is identical in both countries: pay on time, keep utilization below 30%, don't apply for new credit you don't need.

Payment history — 35% FICO, ~30% CIBIL

This is the largest single factor in both models. Every credit card and loan reports your payment status to the bureaus each month. Payments 30, 60, 90, or 120 days late and charge-offs all carry escalating negative weight.

A single 30-day-late payment on a previously clean record can drop a FICO score by 60–110 points, depending on starting score, according to FICO's own modelling. Higher starting scores fall further because the model assumes a higher score has more to lose.

Late-payment marks stay on a US credit report for seven years from the date of the original delinquency. In India, late payments stay on a CIBIL report for the duration of the loan plus seven years after closure for serious defaults.

The practical rule: every payment, every month, on every account, paid by the due date. Auto-pay the minimum on every credit card so a forgotten manual payment never produces a 30-day-late mark. See what is a credit report for the underlying data structure that payment history sits in.

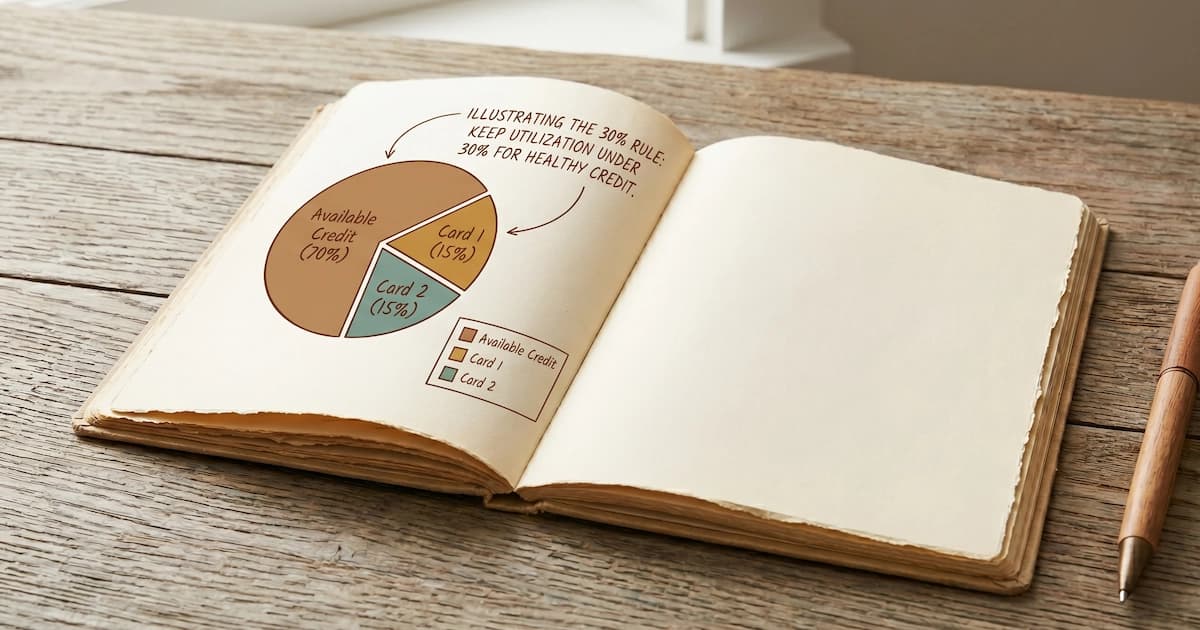

Amounts owed — 30% FICO, ~25% CIBIL

This factor is dominated by credit utilization: the ratio of your current credit card balances to your total credit limits. A person with $2,000 in balances across cards with $10,000 in total limits has 20% utilization.

FICO scores best at utilization below 10%; the score curve drops noticeably above 30% and falls steeply above 50%. CIBIL guidance suggests keeping utilization below 30% for the same reason. Utilization is calculated per-card and across all cards combined; both numbers matter, but the aggregate ratio matters more.

The factor name is "amounts owed," not "amounts borrowed" — the model is measuring how much of your available credit you are currently using, not how much credit you have access to. A higher credit limit on the same balance lowers utilization without changing the underlying debt. This is the mechanism behind the common advice to request credit limit increases on existing cards rather than open new ones — limit increases lower utilization without adding hard inquiries.

For the full mechanics of how this ratio is calculated and what moves it, see our piece on credit utilization.

Length of history, mix, and new credit

The remaining 35% of the FICO score (and the parallel CIBIL components) cover three smaller factors.

Length of credit history (15% FICO) measures the age of your oldest account, your newest account, and the average across all accounts. Older histories score better because more data exists to estimate future behaviour. The practical implication: closing your oldest credit card hurts the score even if the card is unused. Keep the oldest card open with a small recurring charge auto-paid each month.

Credit mix (10% FICO) measures the variety of credit types — revolving (credit cards) and installment (auto, personal, mortgage). A report showing both types scores slightly higher than one type alone. The factor is small enough that it is rarely worth opening new accounts to optimise.

New credit (10% FICO, part of CIBIL's ~20% inquiries factor) measures recent hard inquiries and recently-opened accounts. A single hard inquiry drops a FICO score by 5 points or fewer; the impact fades within 12 months. Multiple inquiries within 14–45 days for the same loan type — mortgage, auto, student — are usually treated as one inquiry on the assumption that you are rate-shopping. Credit card inquiries are not bundled this way.

Worked example: how to move a 680 to a 740

Consider a US borrower at 680 FICO with three credit cards totalling $8,000 in balances against $20,000 in total limits (40% utilization), one 30-day-late payment from 18 months ago, two recent hard inquiries, and a five-year history.

Four levers move this score from 680 to 720–740 over 12 months:

- Pay $4,500 of the credit card balances down. New utilization: 17.5%. Typically adds 30–50 points within 1–2 reporting cycles.

- Continue every payment on time. The 18-month-old late mark loses high-impact weight after 24 months.

- Open no new accounts for 12 months. The two hard inquiries lose effect by month 12.

- Request limit increases on existing cards. A $5,000 increase brings utilization to 14% with no balance change.

The two largest factors — payment history and amounts owed — do the work that the smaller factors cannot.

Common mistakes when trying to raise a score

Closing old credit cards is the most common self-inflicted score drop. The closed card removes from average-age-of-accounts and from total available credit, which raises utilization on the remaining balances. Keep old unused cards open with a small recurring charge.

Paying off and immediately closing an installment loan is the second. The closed loan stops contributing to credit mix and to active payment history.

Disputing accurate items on the report is the third — only inaccurate items should be disputed. Applying for store cards at checkout is the fourth. The 5% register discount is rarely worth the hard inquiry, the average-age hit, and the high APR if you carry a balance.

What experts say

The Consumer Financial Protection Bureau's guide to credit scores covers FICO mechanics and consumer rights under the Fair Credit Reporting Act. myFICO's official factor breakdown is the canonical source for the 35/30/15/10/10 weights cited above.

TransUnion CIBIL's score education page covers the four-factor framework and the 300–900 range used in India. The Reserve Bank of India's credit information regulations govern how Indian credit bureaus collect and report data.

For the underlying credit report data that any score is calculated from, see our piece on what is a credit report. For the credit utilization ratio that drives 30% of the FICO score, see our deeper piece on credit utilization. For the score-band definitions that determine which tier of loan rates each score qualifies for, see what is a good credit score.

Frequently asked questions

What are the five factors that determine a FICO credit score? Payment history (35%), Amounts owed or credit utilization (30%), Length of credit history (15%), Credit mix (10%), and New credit or hard inquiries (10%). Together these cover 100% of the FICO 8 model used by most US lenders. The two largest factors — payment history and amounts owed — together account for 65% of the score, which is why on-time payments and a low utilization ratio matter far more than any other lever.

How is the CIBIL score calculated in India? TransUnion CIBIL uses four broad factors: payment history (roughly 30%), credit utilization (roughly 25%), length and mix of credit (roughly 25%), and new credit and inquiries (roughly 20%). CIBIL has not published exact weights the way FICO has, but their guidance and documentation align with these approximate ranges. The score range is 300–900, and 750 or above is considered good by most Indian lenders.

How long does it take to build a credit score from zero? Both FICO and CIBIL require at least one credit account that has been open and reported for at least six months before they can generate a score. From there, a thin file (one or two accounts) typically reaches the good range in 12–24 months of on-time payments and low utilization. A thick file with multiple account types and several years of history is what produces scores in the very-good or excellent range.

Does checking my own credit score lower it? No. Checking your own score through CIBIL, Experian, Equifax, or services like Credit Karma is a soft inquiry that has no effect on your score. Only hard inquiries — when a lender pulls your report to evaluate a loan or credit card application — affect the score, and even then the impact is small (typically 5 points or less per inquiry) and fades within 12 months.

In summary

FICO weights are 35/30/15/10/10 across payment history, amounts owed, length of history, credit mix, and new credit. CIBIL weights are approximately 30/25/25/20 across the same broad categories. In both systems the two largest factors — payment history and credit utilization — together account for roughly two-thirds of the score, and acting on those two levers produces the largest movement.

The practical playbook is short: pay every bill on time, keep credit card utilization below 30% (and ideally below 10%), don't close oldest cards, and don't apply for credit you don't need. Score gains of 30–60 points over 6–12 months are realistic when those four habits are applied to a starting score in the fair range.

Sources

- myFICO, What's in My FICO Scores — myfico.com/credit-education/whats-in-your-credit-score

- Consumer Financial Protection Bureau, Understanding Your FICO Score — consumerfinance.gov/about-us/blog/understanding-your-fico-score-credit-scoring-101

- TransUnion CIBIL, Credit Score — cibil.com/credit-score

- Reserve Bank of India, Credit Information Companies Regulation — rbi.org.in/Scripts/NotificationUser.aspx?Mode=0&Id=12114

- Investopedia, Credit Score — investopedia.com/terms/c/credit_score.asp

You might also like

What is a credit report? A plain-English explanation of what's on it, where it comes from, who can see it, and how it differs from a credit score.

8 min read

Yes, TransUnion CIBIL's guidance recommends keeping credit utilization under 30%. What 'official' really means, the ideal ratio, and how to lower it fast.

8 min read

What is the difference between APR and interest rate? A plain-English explanation of why they differ, what APR includes, and which to compare when shopping for a loan.

8 min read