Student Loan Grace Period Explained — How the Six-Month Window Works (and What India's Moratorium Looks Like)

By Tapabrata Biswas · Last updated May 11, 2026 · 8 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

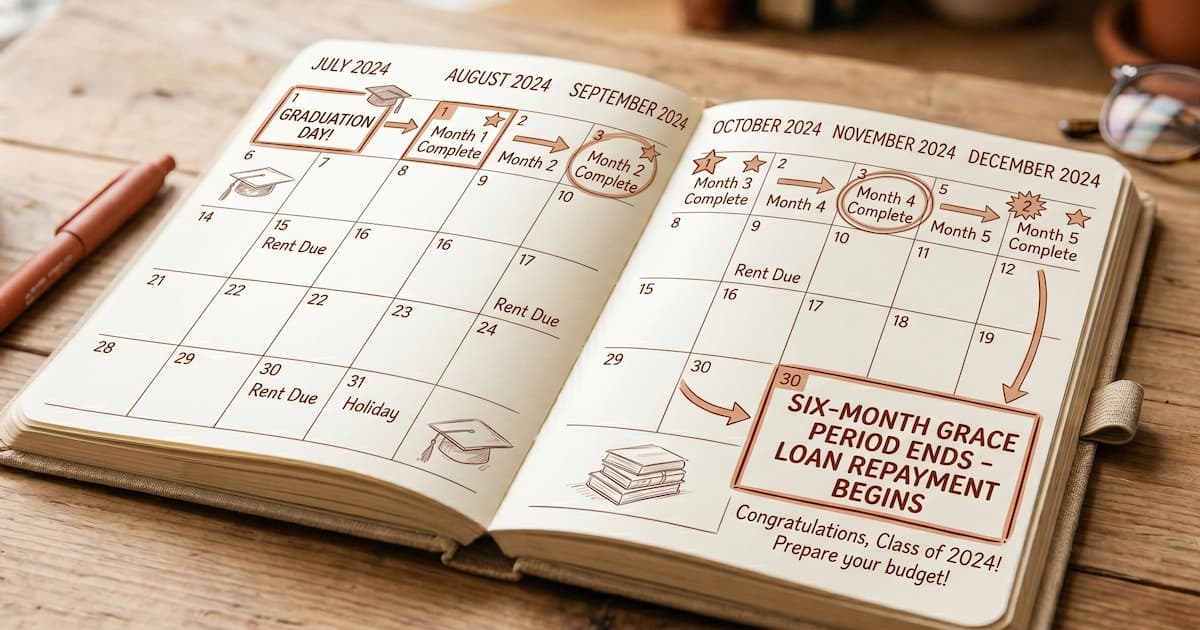

A US federal student loan borrower who graduates in May has until November before the first payment is due — six months, fixed by statute. An Indian engineering student who finishes a four-year B.Tech in 2026 with a ₹10 lakh education loan at 10.5% can defer EMIs until roughly mid-2027, but the bank will have added approximately ₹2.5 lakh in accrued interest to the principal by the time the first EMI is calculated. Same concept, very different financial outcomes.

The student loan grace period (US) and the education loan moratorium (India) are the windows when borrowers are not required to make scheduled payments. What happens to interest during that window decides how much the loan actually costs. This post covers the federal US rules, the IBA model scheme rules in India, and the strategic question every borrower should answer before the grace period ends.

What is a student loan grace period

A grace period is the time between leaving school and the first required loan payment. In the US it is a defined federal benefit: six months on the most common loan types, set by 34 CFR 685.207 governing the William D. Ford Direct Loan Program. The clock starts the day after enrolment drops below half-time — graduation, withdrawal, or part-time status all trigger it.

The Indian equivalent is the moratorium period. Under the IBA Model Education Loan Scheme, banks grant a moratorium covering the course duration plus an additional 6–12 months for the borrower to find employment. SBI's Education Loan Scheme, the largest Indian lender by volume, sets the additional period at 12 months for most cases. The structure looks similar — no scheduled payments — but the interest treatment is the load-bearing difference.

US federal grace period rules by loan type

The grace period and interest treatment vary by loan. The 2024–25 federal interest rates, set annually by Treasury auction and published by Federal Student Aid, are baked into the examples below.

| Loan type | Grace period | Interest during grace | Capitalisation when repayment starts |

|---|---|---|---|

| Direct Subsidised (undergraduate) | 6 months | None — government pays | None |

| Direct Unsubsidised (undergraduate) | 6 months | Accrues at 6.53% | Yes, if unpaid |

| Direct Unsubsidised (graduate) | 6 months | Accrues at 8.08% | Yes, if unpaid |

| Direct PLUS (graduate) | Auto 6-month deferment | Accrues at 9.08% | Yes, if unpaid |

| Direct PLUS (parent) | Deferment by request | Accrues at 9.08% | Yes, if unpaid |

| Perkins (legacy) | 9 months | None — government pays | None |

| Most private loans | Varies (typically 6 months) | Accrues at lender's rate | Per loan agreement |

Direct Subsidised loans are the only consumer credit product in the US where the federal government actively pays interest on the borrower's behalf during specific periods. To qualify, the student must demonstrate financial need on the FAFSA and be enrolled in an undergraduate programme. For everyone else, the loan balance grows during the grace period whether or not the borrower realises it.

What capitalisation actually does to the balance

Capitalisation is when accrued unpaid interest gets folded into the principal at a defined trigger event — the end of the grace period being one of them. After capitalisation, future interest is calculated on the new, larger principal.

A worked example in US dollars. A student graduates with a $30,000 Direct Unsubsidised loan at 6.53% APR. Daily simple interest accrues during the six-month grace period:

- Daily rate: 6.53% ÷ 365 = 0.0179%

- Daily interest on $30,000: about $5.37

- Six months (183 days): roughly $982 in accrued interest

- New principal at start of repayment: $30,982

On a standard 10-year repayment plan, that $982 of capitalised interest costs an extra $336 in interest over the life of the loan — roughly $1,318 of additional cost from the grace period alone if no in-grace payments were made.

Now in Indian rupees. A ₹10 lakh education loan at 10.5% during a four-year B.Tech plus one-year moratorium (60 months total of accruing interest):

- Monthly interest on ₹10,00,000 at 10.5%: roughly ₹8,750

- Approximate accrued interest over 60 months (simple, before capitalisation each year): roughly ₹2,50,000–2,75,000 depending on how the bank compounds during the moratorium

By the time the borrower's first EMI is calculated, the principal is closer to ₹12.5 lakh, and the EMI is set against that larger balance. This is the single largest hidden cost in Indian education lending and the reason the interest rate on the loan understates the true cost of borrowing.

How CSIS subsidises moratorium interest in India

The Central Sector Interest Subsidy Scheme (CSIS) is the Indian government's narrowest answer to the US Direct Subsidised loan benefit. Under the Department of Higher Education's CSIS guidelines, the central government pays 100% of the interest accruing during the moratorium period for students whose annual family income is up to ₹4.5 lakh, on loans up to ₹7.5 lakh, taken for approved courses at recognised institutions.

The scheme covers a thin slice of the borrowing population. Most middle-income families — annual income above ₹4.5 lakh — receive no moratorium interest subsidy at all and bear the full capitalisation cost. State-level schemes (Tamil Nadu's Education Loan Scheme for SC/ST students, Karnataka's Vidyasiri scheme) add coverage at the state level, but the eligibility rules vary widely.

Strategic uses of the grace period

The grace period is not just a payment holiday. It serves a few specific purposes that change how a borrower should approach it.

Time to set up income. The six-month US window matches the typical job-search-to-first-paycheck timeline. The Indian moratorium plus-12-months extension assumes the same employment ramp. Borrowers who land salaried roles within the first three months can use the remaining months to build a small emergency buffer before EMIs hit — covered in our guide on saving as a student or new graduate.

Window to choose a repayment plan. US borrowers can use the six months to compare standard 10-year repayment against an income-driven plan. The choice locks in the monthly payment for at least the next year, so it is worth getting right.

Window to make interest-only payments and avoid capitalisation. This is the single highest-leverage move on unsubsidised US loans and any Indian education loan. Paying just the accruing interest each month during grace or moratorium prevents capitalisation. On the $30,000 example above, paying $164/month in interest during grace ($5.37 × 30) costs $984 over six months — but eliminates the $336 of additional interest the capitalised balance would have generated, and keeps the repayment principal at $30,000 flat.

Time to decide on consolidation. US Direct Consolidation Loans can be initiated during the grace period, but doing so ends the grace period early — the new consolidation loan enters repayment immediately. Most borrowers benefit from waiting until month five or six to consolidate.

Common mistakes during the grace period

A few patterns show up in borrower-complaint data filed with the Consumer Financial Protection Bureau:

- Ignoring servicer communications. US loan servicers (MOHELA, Nelnet, Aidvantage) send the first repayment notification roughly 60 days before payments are due. Borrowers who miss the notification often find their loan in delinquency before they realise repayment has started.

- Assuming subsidised treatment on unsubsidised loans. The two loan types have nearly identical names and identical online portals. Many borrowers do not distinguish them until the first statement arrives showing a higher principal than they remember disbursing.

- Letting the grace period reset incorrectly. A second period of in-school enrolment (returning for a master's, for example) can pause repayment but does not always grant a second six-month grace period. Many borrowers get only an in-school deferment, then resume repayment immediately when they leave the second time.

- In India, missing the CSIS application window. CSIS subsidy must be claimed through the bank during the moratorium. Missing the documentation window means losing the subsidy permanently for that academic year.

What experts say

Federal Student Aid (the US Department of Education office that administers federal loans) explicitly recommends making interest-only payments during the grace period on unsubsidised loans to prevent capitalisation. Their public messaging frames it as the single most cost-effective borrower action available pre-repayment.

The Reserve Bank of India's Master Circular on Education Loans directs banks to extend moratorium and to consider servicing of interest during the moratorium as a borrower option, not a default. RBI permits banks to give a 1% interest rate concession to borrowers who service interest during the moratorium — a benefit very few borrowers claim because banks rarely advertise it.

The Consumer Financial Protection Bureau's student loan complaint database shows post-grace surprise — borrowers reporting their balance is higher than the original loan amount — as one of the top three complaint categories year after year. The pattern reflects how poorly capitalisation is communicated by servicers. For broader context on how interest accumulates over time, our explainer on compound interest covers the same mechanic that drives capitalisation.

Frequently asked questions

How long is the federal student loan grace period in the US? Six months for Direct Subsidised and Direct Unsubsidised loans, beginning the day after you drop below half-time enrolment. PLUS loans for graduate students get an automatic six-month deferment that functions like a grace period, while parent PLUS borrowers can request the same deferment but it is not automatic. Perkins loans (now discontinued for new borrowers but still on existing accounts) carry a nine-month grace period.

Does interest accrue during the grace period? It depends on the loan type. Direct Subsidised loans accrue no interest during the grace period — the US Department of Education pays it. Direct Unsubsidised loans, PLUS loans, and most private loans accrue interest the entire time, and any unpaid interest capitalises (gets added to principal) when repayment begins. On a $30,000 unsubsidised loan at 6.53%, six months of grace adds roughly $980 to the balance before the first payment is due.

Is the Indian education loan moratorium the same as a US grace period? Functionally similar but structurally different. Under the IBA Model Education Loan Scheme, Indian banks grant a moratorium of course duration plus 6–12 months. Interest accrues during the entire moratorium and is added to principal when EMIs begin. The CSIS scheme covers 100% of moratorium interest for students from families earning under ₹4.5 lakh annually on loans up to ₹7.5 lakh, but most middle-income borrowers pay the accumulated interest themselves.

Can I make payments during the grace period? Yes, and on unsubsidised or Indian moratorium loans it makes a real difference. Paying just the accruing interest each month during the grace or moratorium period stops capitalisation, so your repayment EMI is calculated on the original principal rather than principal plus accrued interest. On a ₹10 lakh Indian education loan at 10.5% with a four-year course plus one-year moratorium, paying interest during the moratorium can save roughly ₹3 lakh over the life of the loan.

In summary

The grace period is a window, not a benefit, and what fills the window is interest. US Direct Subsidised borrowers get a true free pass for six months. Everyone else — unsubsidised US borrowers, PLUS borrowers, almost all private US borrowers, and almost all Indian education loan borrowers outside CSIS — pays for the deferral in capitalised interest. The borrower who treats the grace period as the start of repayment, even at interest-only, ends up with a measurably smaller loan than the borrower who waits.

Sources

- Federal Student Aid — Interest Rates and Fees for Federal Student Loans — 2024–25 federal loan interest rates set by Treasury auction

- Indian Banks' Association — Model Education Loan Scheme — moratorium structure and standard terms across Indian banks

- Department of Higher Education — Central Sector Interest Subsidy Scheme (CSIS) — moratorium interest subsidy for economically weaker students

- Reserve Bank of India — Master Circular on Loans and Advances — directions on education loan structure and concessions

- Consumer Financial Protection Bureau — Student Loan Complaint Bulletin — patterns in post-grace borrower complaints

You might also like

Best ways to save money as a student — the categories where the gains are biggest (housing, food, textbooks, transport), the social pressure that defeats most plans, and the habits that pay off long after graduation.

9 min read

What is an interest rate? A plain-English explanation of how interest works, how it is calculated, and why the same number behaves differently in different contexts.

8 min read

What is compound interest? A plain-English explanation of how interest builds on itself, why time matters more than rate, and how it works on both savings and debt.

8 min read